What are the key factors currently influencing housing markets in the UK?

What You Need To Be Aware Of In UK Housing Market 2024 and Foreseeable Future: Institutional Buying and Its Impact on You

The UK housing market has been a topic of constant discussion for years, and 2024 is no different. While the pandemic initially caused a temporary halt, the market rebounded with a vengeance. However, recent trends suggest a potential cooling period, with some predicting price drops. However, could UK house prices be propped up by institutional buyers?

However could UK housing market prices be sustained by institutional buyers?

CheeringupInfo Lifestyle Improvement Club

One significant factor influencing the market’s future is the growing presence of large institutions like Lloyds Bank and major investment funds. These entities are actively buying thousands of single-family homes, prompting questions about the long-term implications for consumers and families.

Sign up for our free newsletter to receive valuable insights on navigating the housing market, financial planning, healthy living tips, and relationship advice. Together, let’s build a brighter future for ourselves and our families.

This article explores the reasons behind institutional buying, its potential impact on the UK housing market, both positive and negative, and what you, as a consumer, need to be aware of to navigate this evolving landscape.

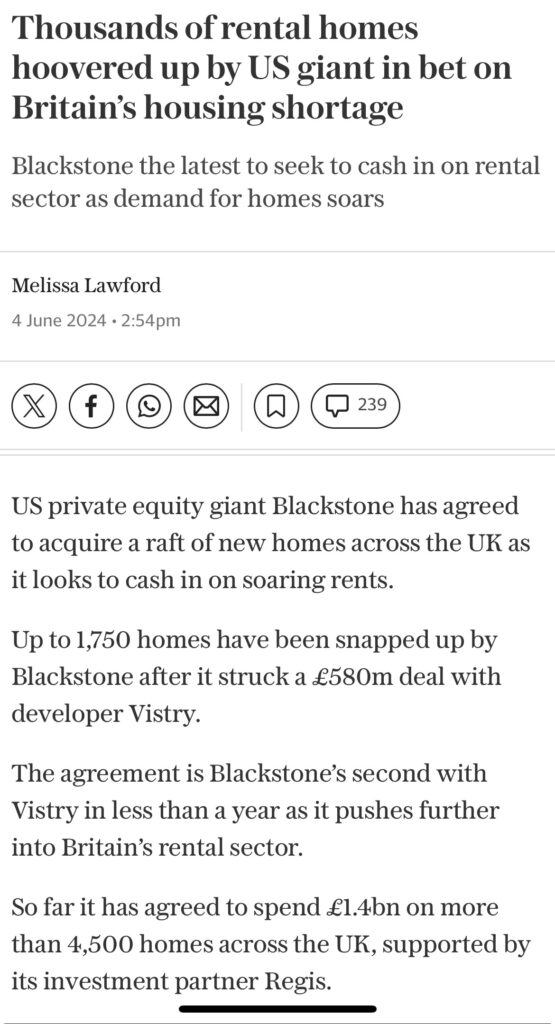

Blackstone the latest to seek to cash in on rental sector as demand for homes soars cheeringup.info #HousingMarketUK #HomesUK #HousingCrisis

Why Are Institutions Buying Houses?

Several factors motivate large institutions to enter the single-family home market:

Stable Returns: Property historically offers consistent returns, acting as a hedge against inflation. Property investment becomes an attractive option for institutions seeking long-term, stable income streams.

Diversification: Institutions hold a diversified portfolio of assets to minimise risk. Including residential property provides diversification and reduces dependence on traditional investment vehicles like stocks and bonds, or even commercial property investments that are currently tanking.

Scarcity and Demand: The UK housing market faces a chronic shortage of available properties, particularly affordable ones. This scarcity fuels demand, making residential property a potentially lucrative investment.

9 Reasons Why Institutional Buying Matters (For Good and Bad)

The rise of institutional buying in the UK housing market carries significant weight for consumers and families. Here are nine key reasons why:

Potential Benefits:

Increased Supply: Institutions may unlock additional housing stock by renovating older properties or acquiring underutilised land for development, potentially increasing overall supply in the long run.

Professional Management: Large institutions often have professional property management teams, potentially leading to better maintenance and more responsive landlords for tenants.

Stabilised Prices: Increased institutional ownership could dampen price volatility, leading to a more stable market in the long term.

Potential Drawbacks:

Reduced Affordability: Large-scale buying by cash-rich institutions could further drive up prices, particularly for first-time buyers, potentially pushing them out of the market.

Reduced Choice: With institutions snapping up available properties, individual buyers may face a smaller pool of homes to choose from, limiting their options.

Community Impact: A high concentration of institutionally-owned properties might affect the character and dynamic of neighbourhood, potentially leading to a homogenisation of communities.

Uncertainty for Tenants: The long-term impact on tenant rights and protections remains unclear. Institutional ownership might lead to changes in tenancy agreements or increased focus on short-term rentals.

Financial System Risk: If the housing market suffers a significant downturn, institutions holding large numbers of properties could face financial difficulties, potentially impacting the broader financial system.

Reduced Social Mobility: Difficulty accessing affordable homeownership could hinder social mobility, making it harder for young families to build wealth and move up the economic ladder.

Actions You Can Take to Protect Yourself

The rise of institutional buying creates a complex landscape for UK consumers. Here are some actions you can take to protect yourself:

Be Prepared to Move Quickly: If you’re a buyer, be ready to act fast and make competitive offers, as institutions might be prepared to offer above asking price.

Consider Alternatives: Explore alternative housing options like shared ownership schemes or government-backed initiatives to increase affordability.

Do Your Research: Thoroughly research any property you’re considering, particularly regarding ownership and potential future plans.

Seek Professional Advice: Consulting a mortgage broker or financial adviser can help navigate the evolving market and develop a sound buying strategy.

The housing market, while crucial, is just one aspect of a fulfilling life. Cheeringup.info, a Lifestyle Improvement Club, offers resources and support for individuals and families to thrive in various areas. From financial planning to healthy living and relationship advice, Cheeringup.info empowers you to build a well-rounded life beyond the housing market.

Conclusion

The rise of institutional buying in the UK housing market presents both opportunities and challenges for consumers. While it has the potential to increase supply, stabilise prices, and improve professional management, it also carries risks like reduced affordability, limited choice, and potential community impacts. By staying informed, taking proactive steps, and seeking professional advice, UK consumers can navigate this evolving landscape and make informed decisions about their housing needs. Remember, a fulfilling life extends beyond the walls of your home. Explore resources offered by Cheeringup.info to empower yourself in all aspects of life.

Signup for free lifestyle improvement tips and reviews

Sign up for our free newsletter to receive valuable insights on navigating the housing market, financial planning, healthy living tips, and relationship advice. Together, let’s build a brighter future for ourselves and our families.

Simple words linked to your business selling process

Accelerate your business growth in the UK with Cheeringup.info’s Textlink Advertising service! In a digital world, visibility is crucial, and our text link ads offer an effective way to enhance your online presence. By placing your link on Cheeringup.info, you can reach a targeted audience looking for valuable resources and services like yours.

Our platform ensures that your business stands out, driving traffic directly to your website and boosting your brand recognition. With our user-friendly advertising options, you can quickly and easily promote your services, products, or events to potential clients.

Don’t miss this opportunity to leverage our established platform to expand your reach. Sign up for a text link ad on Cheeringup.info today and watch your business thrive faster than ever!

The Cost-Effectiveness of Textlink Adverts on Websites and Social Media Accounts for Businesses in the UK

In today’s digital age, businesses are constantly seeking effective and budget-friendly ways to drive traffic, enhance visibility, and increase sales. Among the plethora of digital marketing strategies, textlink adverts on websites and social media accounts stand out as a particularly cost-effective solution. This article delves into why textlink adverts are an efficient choice for businesses in the UK, discusses the essentials of using text links to drive new business, and offers six top tips to maximize their effectiveness.

The Benefits of Textlink Adverts

Cost-Effectiveness:

Lower Costs: Compared to banner ads or video ads, textlink adverts are significantly cheaper to create and implement. They require minimal design work and can be easily integrated into existing content.

Pay-Per-Click (PPC) Models: Many textlink adverts operate on a PPC basis, ensuring that businesses only pay when a user actually clicks on the link. This model can be more cost-effective than paying for impressions alone.

Improved Click-Through Rates (CTR):

Contextual Relevance: Text links embedded within relevant content are more likely to be clicked because they are contextually related to the reader’s interests.

Less Intrusive: Unlike flashy banner ads that can be intrusive, text links blend seamlessly into content, making them less likely to be ignored or blocked by ad blockers.

SEO Benefits:

Boosting Rankings: High-quality text links from reputable websites can improve a business’s search engine rankings. Search engines consider these backlinks as endorsements, which can enhance a site’s authority and visibility.

Anchor Text Optimisation: Text links with relevant keywords help search engines understand the context and relevance of the linked content, potentially improving the rankings for those keywords.

Enhanced Engagement:

Targeted Traffic: Since text links are usually embedded in related content, they attract a more targeted audience who are already interested in the topic, leading to higher engagement rates.

Deeper Content Integration: By placing text links within articles, blog posts, or social media updates, businesses can provide additional value and context, encouraging users to explore further.

Flexibility and Scalability:

Easy Implementation: Adding or modifying text links is straightforward and does not require complex coding or design changes.

Scalable Campaigns: Businesses can easily scale their textlink campaigns by increasing the number of links or extending them across multiple platforms without significant additional costs.

Essentials of Text Links for Driving New Business

Relevance:

Ensure that the text link is relevant to the content in which it is placed. This relevance increases the likelihood of clicks and provides a better user experience.

Anchor Text:

Use descriptive and keyword-rich anchor text that clearly indicates what the user will find when they click the link. This not only helps with SEO but also sets the right expectations for the user.

Quality Over Quantity:

Focus on obtaining links from high-authority sites rather than numerous low-quality sites. High-quality backlinks are more beneficial for SEO and are likely to drive more meaningful traffic.

Clear Call-to-Action (CTA):

Ensure that the text link includes a compelling call-to-action that encourages users to click. Phrases like “Learn more,” “Get started,” or “Discover how” can be very effective.

Tracking and Analytics:

Use tracking tools to monitor the performance of your text links. Analysing data such as click-through rates and conversion rates can help you understand the effectiveness of your links and make necessary adjustments.

User Experience:

Text links should enhance the user experience, not detract from it. Avoid overloading your content with links and ensure that they are placed naturally within the text.

Top Tips for Highly Effective Text Links

Strategic Placement:

Place text links in strategic locations where they are most likely to be seen and clicked. Typically, links within the first few paragraphs of an article, near engaging visuals, or within list items tend to perform better.

Consider using multiple links throughout longer pieces of content to capture attention at different points.

Utilise Social Proof:

Leverage user-generated content, testimonials, and reviews by linking to these types of content within your text links. Social proof can increase trust and credibility, making users more likely to click and convert.

Encourage customers to share their experiences and link to these stories in your content.

Link to Valuable Resources:

Ensure that your text links point to valuable and relevant resources. This could include detailed blog posts, product pages, whitepapers, or case studies that provide additional value to the user.

High-value content can significantly improve engagement and conversion rates.

Mobile Optimisation:

With an increasing number of users accessing content on mobile devices, it’s crucial to ensure that text links are easily clickable on smaller screens. This includes using larger font sizes and ensuring adequate spacing around links.

Test your links on various devices to ensure they work seamlessly across all platforms.

A/B Testing:

Experiment with different anchor texts, link placements, and CTAs to see what resonates most with your audience. A/B testing allows you to optimise your text links based on data-driven insights.

Regularly update and test your text links to maintain their effectiveness.

Build Relationships for Backlinks:

Establish relationships with industry influencers, bloggers, and reputable websites to gain high-quality backlinks. Guest posting, collaborations, and joint ventures can be effective ways to secure these valuable links.

Focus on building long-term relationships that can provide ongoing backlink opportunities.

Conclusion

Textlink adverts on websites and social media accounts offer a cost-effective and powerful way for businesses in the UK to drive traffic, enhance visibility, and increase sales. By understanding the essentials of text link advertising and implementing the top tips provided, businesses can maximise the effectiveness of their campaigns and achieve substantial growth. Textlink adverts, with their ability to integrate seamlessly into content, provide a non-intrusive yet highly engaging method to attract and convert potential customers, making them an indispensable tool in the digital marketing arsenal.

Why Image Logo Advertising for Lifestyle Products and Services is Cost-Effective in the UK

Image logo advertising is a potent tool for promoting lifestyle products and services in the UK. It combines visual appeal with brand recognition to create a memorable impact on consumers. This approach not only enhances brand visibility but also fosters a deeper connection with the target audience, ultimately proving to be cost-effective. Here’s why image logo advertising is beneficial and how to maximise its impact:

The Power of Visual Branding

Visual branding, particularly through image logos, is crucial in lifestyle marketing. It helps in establishing an immediate connection with the audience. According to studies, humans process images 60,000 times faster than text, and nearly 90% of information transmitted to the brain is visual. This makes image logo advertising an effective way to capture attention quickly and convey brand messages succinctly.

Enhanced Brand Recognition: Consistent use of a well-designed logo helps in creating a strong visual identity for your brand. It makes your brand easily recognisable, which is essential in a crowded market.

Emotional Connection: Images evoke emotions. By using images that reflect the lifestyle your brand promotes, you can create an emotional bond with your audience. For instance, using images of happy, active individuals for a fitness brand can inspire and motivate potential customers.

Storytelling: Lifestyle brands thrive on storytelling. Images can tell a story at a glance, portraying the lifestyle your product supports. This storytelling aspect is vital in creating a narrative that resonates with your audience.

Cost-Effectiveness: Compared to text-heavy ads, image logo advertising can be more cost-effective. It reduces the need for extensive copy and can be used across various platforms with minimal modifications, ensuring a consistent brand message.

Maximising the Impact of Image Logo Advertising

To ensure that your image logo advertising is as effective as possible, consider the following strategies:

Know Your Audience: Understanding your target audience is crucial. Identify their preferences, values, and lifestyles. Tailor your images to reflect these aspects to make your ads more relatable and appealing.

Quality Over Quantity: Invest in high-quality images. Professional photography and design can make a significant difference in how your brand is perceived. High-quality visuals convey professionalism and build trust.

Consistency is Key: Maintain consistency in your visual branding. Use the same colour schemes, fonts, and style across all platforms. This helps in reinforcing your brand identity and making it more recognisable.

Utilise Social Media: Social media platforms are ideal for image logo advertising. Platforms like Instagram, Pinterest, and Facebook are highly visual and can help you reach a larger audience. Use these platforms to showcase your products in a lifestyle context.

Engage with User-Generated Content: Encourage your customers to share their own photos using your products. This not only provides authentic content but also builds a community around your brand. User-generated content can be a powerful testimonial and add credibility.

Leverage Influencers: Collaborate with influencers who align with your brand’s lifestyle. Influencers can amplify your reach and add a layer of trust and authenticity to your advertising efforts.

Adapt to Trends: Stay updated with the latest trends in visual marketing. Adapt your strategies to include new styles and formats that appeal to your audience.

Best Types of Images for UK Consumers

To resonate with UK consumers, consider the following types of images:

Authentic and Relatable: Use images that feel genuine and relatable. Avoid overly staged or edited photos. Authenticity can help in building trust and connection.

Cultural Relevance: Ensure your images reflect the cultural context of your target audience. This includes diversity and inclusion, which are highly valued in the UK.

Seasonal and Local: Use seasonal themes and local landmarks to make your images more relatable to UK consumers. This could include autumn leaves, local festivals, or iconic locations.

Lifestyle-Oriented: Showcase your products in real-life scenarios that your audience aspires to. For example, if you’re selling outdoor gear, use images of people hiking or camping in picturesque UK landscapes.

High-Energy and Positive: Positive and high-energy images can be very appealing. They create a feel-good factor that can enhance the attractiveness of your brand.

Practical Tips for Effective Image Logo Advertising

Optimise for Mobile: Ensure your images are optimised for mobile viewing. With a significant portion of internet traffic coming from mobile devices, this is crucial for reaching your audience effectively.

SEO-Friendly: Use descriptive file names and alt text for your images. This can improve your search engine rankings and make your images more discoverable online.

Call-to-Action: Include clear call-to-actions (CTAs) in your visual ads. Whether it’s to visit your website, follow your social media, or make a purchase, a strong CTA can drive engagement and conversions.

A/B Testing: Conduct A/B testing to see which images perform best. This can provide valuable insights into what resonates most with your audience and help you refine your strategy.

Analytics: Use analytics tools to track the performance of your image logo ads. Monitor metrics like engagement, click-through rates, and conversions to measure the effectiveness of your campaigns.

Sustainability and Ethics: Highlight any sustainable and ethical practices in your visual content. UK consumers are increasingly conscious about sustainability, and showcasing your commitment can enhance your brand’s appeal.

Conclusion

Image logo advertising is a powerful and cost-effective tool for promoting lifestyle products and services in the UK. By focusing on visual storytelling, maintaining consistency, leveraging social media, and understanding your audience, you can create impactful ads that resonate with consumers. High-quality, authentic images that reflect the aspirations and lifestyles of your target audience can significantly enhance brand recognition and loyalty. With strategic implementation, image logo advertising can drive long-term success and growth for your business.

Unveiling the Enchanting Spirit of Chiang Mai: A Tapestry of Culture, Adventure, and Serenity

Nestled amidst the verdant embrace of northern Thailand, Chiang Mai beckons travelers seeking an experience unlike any other. Often lauded for its rich cultural heritage and breathtaking natural beauty, Chiang Mai offers a captivating blend of ancient temples, vibrant markets, delectable cuisine, and thrilling adventures. Whether you’re a history buff yearning to delve into the past, a nature enthusiast seeking outdoor escapades, or a curious explorer craving authentic experiences, Chiang Mai has something to enthrall you.

Best Khao Soi So Far Chiang Mai Thailand cheeringup.info #KhaoSoi #ChiangMai #Thailand #CheeringupInfo #CheeringupTV #RetirementIdeas #RetirementMagazine #RetirementTV #GuidePrice #BestPrice

A Journey Through Time: Unveiling Chiang Mai’s Cultural Tapestry

Chiang Mai boasts a legacy etched in majestic temples and captivating ruins. Within the city walls lies the heart of its cultural soul – the Old City. Here, wander through the ancient moat and explore an array of magnificent temples. Wat Phra Singh, adorned with intricate murals and housing a revered Buddha statue, offers a glimpse into Lanna Kingdom artistry. Climb the revered Doi Suthep, home to Wat Phra Doi Suthep, and be rewarded with panoramic vistas of the city sprawled beneath a veil of mist. For a unique experience, witness the daily morning alms-giving ceremony, where saffron-robed monks receive offerings from devotees – a poignant display of faith and tradition.

Beyond the Temples: Unveiling Artistic Gems

Chiang Mai’s artistic spirit transcends its temples. Explore the whimsical grounds of Wat Chiang Man, the city’s oldest temple, and marvel at its Elephant Gate, or delve into the world of contemporary art at the MAIIAM Contemporary Art Museum. Stroll through the vibrant Saturday Walking Street Market, a haven for handcrafted souvenirs and local artistry. For a unique perspective, take a Thai cooking class and learn to recreate the fragrant curries and noodle dishes that define Chiang Mai’s culinary scene.

Elephants Chiang Mai Thailand!

Nature’s Playground: Adventures Await

Chiang Mai isn’t just about temples and markets. Lush rainforests, majestic mountains, and cascading waterfalls beckon adventure seekers. Embark on a thrilling elephant trek (ensure the sanctuary prioritises ethical treatment) through the verdant jungles, or conquer the slopes of Doi Inthanon National Park, the “Roof of Thailand,” and encounter captivating wildlife. Paddle down the Mae Taeng River on a bamboo raft, soaking in the breathtaking scenery, or cool off beneath the cascading waters of Huay Mae Khaeng waterfall.

A Culinary Adventure for Your Taste Buds

No exploration is complete without indulging in the local cuisine. Chiang Mai’s culinary scene is a symphony of flavors, marrying traditional Lanna dishes with influences from neighboring Burma. Savour the fiery northern Thai curries like Kaeng Kai or Kaeng Hung Le, bursting with fragrant spices and creamy coconut milk. Don’t miss the signature Khao Soi, a flavourful curry noodle dish with crispy fried noodles, or indulge in a steaming bowl of Nam Prik Ong, a fiery chili paste dip perfect with fresh vegetables. For a unique experience, visit a local night market and embark on a culinary adventure, savouring an array of street food delicacies.

Beyond the City Limits: Exploring the Environs

Chiang Mai serves as a perfect base for exploring the surrounding wonders. Journey to the historic city of Wiang Kum Kam, the former Lanna capital, and wander through its ruins and remnants of a bygone era. Explore the Elephant Nature Park, a sanctuary dedicated to rescuing and rehabilitating elephants, or visit an orchid farm and be captivated by the vibrant colors and delicate blooms. Hike to the summit of Doi Ang Khang, and witness breathtaking vistas of cascading rice terraces and lush valleys.

Unveiling the Hill Tribes

For a deeper cultural immersion, venture into the nearby hill tribe villages. The Akha, Karen, and Hmong people, with their unique traditions and colorful garments, inhabit these mountains. Witness their skilled craftsmanship, from intricate textiles to handcrafted jewellery. Be sure to interact with them respectfully, avoiding any form of exploitation, and supporting their communities through ethical tourism practices.

Nightlife with a Local Twist

After a day of exploration, unwind at Chiang Mai’s vibrant night markets. Immerse yourself in the bustling atmosphere as you browse through an array of local handicrafts, souvenirs, and delectable street food. Sample the region’s exotic fruits, indulge in freshly prepared satay skewers, and treat yourself to a refreshing mango sticky rice. For a unique experience, catch a live Muay Thai boxing match, a traditional Thai martial art characterised by its dynamic kicks and powerful strikes.

Tips for Maximising Your Chiang Mai Experience

Plan your trip: Decide on the time of year you want to visit. The cool season (November to February) offers pleasant weather, while the Songkran Festival (Thai New Year) in April is a vibrant cultural experience, but be prepared for crowds.

Embrace the slow pace: Chiang Mai offers a more relaxed atmosphere compared to the bustling streets of Bangkok. Slow down, savour the moment, and appreciate the city’s laid-back charm.

Respect the culture: When visiting temples, dress modestly and be mindful of local customs. Be courteous to the locals and avoid disrespectful behaviour.

Bargain with a smile: While not everything is negotiable, haggling is expected at the night markets. Do so politely and enjoy the interactive experience.

Support ethical tourism: Opt for tours that prioritise the well-being of animals and local communities. Avoid activities that exploit elephants or other wildlife.

Learn a few Thai phrases: Basic greetings like “Sa-wat dee krap” (hello for men) and “Sa-wat dee ka” (hello for women) go a long way in showing respect and appreciation.

Pack appropriately: Depending on the season, pack light breathable clothes for hot weather or a light jacket for cooler nights. Comfortable shoes are a must for exploring temples and navigating uneven terrain.

Explore beyond the main attractions: Don’t be afraid to venture off the beaten path and discover hidden gems. Explore local artisan workshops, take a Thai massage class to unwind after a day of exploration, or visit a local coffee plantation and learn about the region’s coffee-making process.

Embrace the unexpected: Chiang Mai is a city full of surprises. Be open to new experiences, strike up conversations with locals, and allow yourself to be swept away by the city’s unique charm.

A City that Stays with You

Chiang Mai is more than just a tourist destination; it’s an experience that lingers in your memory long after you depart. It’s a place where ancient traditions blend seamlessly with modern life, where breathtaking natural beauty inspires awe, and where delicious cuisine tantalises your taste buds. Whether you’re seeking spiritual solace, cultural immersion, or thrilling adventures, Chiang Mai offers something for everyone. So, pack your bags, embrace the spirit of adventure, and allow Chiang Mai to weave its magic on you. You might just find yourself captivated by this enchanting city in the heart of northern Thailand.

Some images and videos of Chiang Mai

Global Digital Nomad Magazine Tom yum Kung Muay Thai In Thailand cheeringup.info #MuayThai #ChiangMai #ThailandMuay Thai In Thailand cheeringup.info #MuayThai #ChiangMai #ThailandMuay Thai In Thailand cheeringup.info #MuayThai #ChiangMai #Thailand

Unveiling the Enchantment of Chiang Rai: A Haven Beyond the Usual

Nestled amidst the emerald embrace of northern Thailand, Chiang Rai beckons travellers seeking an experience unlike any other. Often overshadowed by its larger neighbour, Chiang Mai, Chiang Rai offers a unique blend of cultural charm, artistic wonders, and breathtaking natural beauty. Whether you’re a history buff, an art enthusiast, or an adventurer at heart, Chiang Rai has something to enthrall you.

A Tapestry of Culture and Tradition

Chiang Rai’s soul is steeped in centuries-old traditions. Grand temples like Wat Phra Kaew (housing the Emerald Buddha replica) and Wat Phra Singh, adorned with intricate carvings and vibrant murals, transport you to a bygone era. Immerse yourself in the serene ambiance of these sacred spaces and witness the unwavering faith of the Thai people.

A Realm of Artistic Expression

Chiang Rai is a haven for those who appreciate artistic innovation. The world-renowned White Temple, Wat Rong Khun, is a masterpiece of contemporary art. Its gleaming white facade and intricate sculptures challenge conventional temple architecture, leaving you awestruck. In stark contrast, the Black House, with its collection of dark wood structures and thought-provoking exhibits, offers a glimpse into the artistic vision of Thailand’s national artist, Thawan Duchanee.

Beyond the City Walls: Adventures Await

Chiang Rai’s magic extends far beyond its city limits. Venture into the lush countryside and discover the enchanting Golden Triangle, where the borders of Thailand, Laos, and Myanmar converge. Take a boat trip along the mighty Mekong River and witness the vibrant cultures of these Southeast Asian nations.

Embrace the Thrill of Nature

For the intrepid explorer, Chiang Rai boasts a plethora of outdoor adventures. Trek through the verdant jungles of Doi Luang National Park, the highest mountain in northern Thailand, and encounter diverse flora and fauna. Hike up to the summit of Doi Pha Tang and be rewarded with panoramic vistas of the surrounding valleys. Explore the breathtaking Mae Fah Luang Garden, a haven of colorful flowers and cascading waterfalls.

A Culinary Adventure for Your Taste Buds

No exploration is complete without indulging in the local cuisine. Chiang Rai’s culinary scene is a delightful fusion of northern Thai flavours and Burmese influences. Savour the rich curries, like Kaeng Kai or Kaeng Hung Le, bursting with fragrant spices and creamy coconut milk. Don’t miss the chance to try Khao Soi, a flavourful curry noodle dish unique to northern Thailand.

Unveiling the Hill Tribes

For a deeper cultural immersion, visit the nearby hill tribe villages. The Akha, Karen, and Lisu people have inhabited these mountains for centuries, preserving their unique traditions and ways of life. Witness their colourful clothing, intricate handicrafts, and warm hospitality. Be sure to interact with them respectfully and ethically, avoiding any form of exploitation.

Nightlife with a Local Twist

After a day of exploration, unwind at Chiang Rai’s lively night market. Immerse yourself in the vibrant atmosphere as you browse through an array of local handicrafts, souvenirs, and delectable street food. Sample the region’s exotic fruits, indulge in freshly prepared satay skewers, and treat yourself to a refreshing mango sticky rice.

Tips for an Unforgettable Chiang Rai Experience

Plan your trip: Decide on the time of year you want to visit and research festivals or events that might be happening during your stay. The cool season (November to February) offers pleasant weather, while the rainy season (July to October) showcases lush landscapes.

Embrace the slow pace: Unlike the bustling streets of Bangkok, Chiang Rai offers a more relaxed atmosphere. Slow down, savour the moment, and appreciate the city’s laid-back charm.

Respect the culture: When visiting temples, dress modestly and be mindful of local customs. Be courteous to the locals and avoid disrespectful behaviour.

Bargain with a smile: While not everything is negotiable, haggling is expected at the night markets. Do so politely and enjoy the interactive experience.

Support ethical tourism: Opt for tours that prioritise the well-being of animals and local communities. Avoid activities that exploit elephants or other wildlife.

Learn a few Thai phrases: Basic greetings like “Sa-wad dee krap” (hello for men) and “Sa-wad dee ka” (hello for women) go a long way in showing respect and appreciation.

Pack appropriately: Depending on the season, pack light breathable clothes for hot weather or a light jacket for cooler nights. Comfortable shoes are a must for exploring temples and navigating uneven terrain.

Explore beyond the main attractions: Don’t be afraid to venture off the beaten path and discover hidden gems. Explore local villages, coffee plantations, or take a cooking class to learn about regional cuisine.

Chiang Rai: A Destination that Stays with You

Chiang Rai is a destination that stays with you long after you leave. It’s a place where ancient traditions meet contemporary art, where breathtaking natural beauty collides with vibrant cultural experiences. Whether you’re seeking spiritual solace, artistic inspiration, or thrilling adventures, Chiang Rai offers something for everyone. So, pack your bags,embrace the unknown, and allow Chiang Rai to weave its magic on you.

A Few Final Words

This article has merely scratched the surface of Chiang Rai’s endless charm. With its diverse offerings and laid-back atmosphere, Chiang Rai is a city waiting to be explored. So, come and discover the magic for yourself. You might just find yourself falling in love with this hidden gem of northern Thailand.

Do you need to pay any immigration fees at border going from Thailand into Laos?

No, you won’t pay immigration fees exiting Thailand. Thailand doesn’t charge departure fees.

However, you will need to pay for a visa on arrival upon entering Laos. The cost depends on your nationality. Here’s what to expect:

Visa on Arrival: This is the most common way to enter Laos for tourists. The fee is typically paid in US Dollars (USD) and can vary between nationalities. It can range from around $30 to $50 USD.

Exceptions: Citizens of some countries, like those from Southeast Asia, may be exempt from visa fees. You can check the official Laos government website or embassy in your home country for the latest visa information.

Chiang Rai Global Digital Nomad Magazine videos images and tourist information

Chiang Rai Saturday Night Walking Street Market

Get help to protect and grow your retirement related business faster

Good bye São Paulo Brazil South America and the Americas!São Paulo To Addis AbabaAddis AbabaBangkok Airport

The Grand Palace

The Grand Palace is a sprawling complex of buildings at the heart of Bangkok, Thailand. It served as the official residence of the Kings of Siam (later Thailand) from 1782 until 1925. Today, the Grand Palace remains a symbol of the Thai monarchy and a major tourist attraction.

The Grand Palace Entrance

Why It’s Worth Visiting:

Historical Significance: The Grand Palace has been the centre of Thai royalty for centuries. It played a crucial role in the history and development of Bangkok and Thailand.

Architectural Splendor: The complex showcases a blend of traditional Thai and European architectural styles. Its intricate details, gilded facades, and exquisite craftsmanship are breathtaking.

Emerald Buddha: Within the Grand Palace grounds is Wat Phra Kaew (Temple of the Emerald Buddha), which houses the revered Emerald Buddha, a statue carved from a single block of jade.

Cultural Insight: Visiting the Grand Palace offers a deep dive into Thai culture, religion, and art. It’s a place where you can observe the traditions and reverence the Thai people have for their monarchy and religion.

Gardens and Courtyards: The Palace grounds include beautifully manicured gardens and courtyards, providing a serene environment amid the bustling city.

Tips and Secrets for Making the Most of Your Visit:

The Grand Palace Bangkok Thailand

Dress Code: Strict dress code enforcement requires visitors to wear modest clothing. Shoulders and knees must be covered. Avoid ripped jeans, leggings, or see-through clothing. Sarongs are available for rent at the entrance if needed.

Best Time to Visit: Arrive early in the morning to avoid the crowds and the midday heat. The palace opens at 8:30 AM, and being there at opening time can enhance your experience.

Plan Your Visit: Allocate at least 2-3 hours to explore the complex fully. The grounds are extensive, and there’s much to see.

Guided Tours: Consider hiring a guide or joining a guided tour. Knowledgeable guides can provide detailed explanations about the history, architecture, and significance of the various buildings and statues.

Avoid Scams: Be wary of touts outside the palace who may tell you that it’s closed for a private event and offer alternative tours. The palace is rarely closed to the public.

Photography: While photography is allowed in many parts of the Grand Palace, it is prohibited inside the Temple of the Emerald Buddha. Be respectful and follow the rules.

Stay Hydrated: Bangkok can be very hot and humid. Bring water and stay hydrated during your visit.

Visit Nearby Attractions: Combine your visit with nearby attractions like Wat Pho (Temple of the Reclining Buddha) and Wat Arun, which are a short boat ride away across the Chao Phraya River.

Entrance Fee: Be prepared to pay an entrance fee. As of my last update, it was 500 Thai Baht. Check for the latest prices and payment options.

Secret Tips:

The Grand Palace

Hidden Gems: Look for the miniature model of Angkor Wat, which is tucked away in the northeastern corner of the palace complex. It’s an often-overlooked but fascinating replica.

Museum of the Emerald Buddha Temple: This museum within the complex is less crowded and contains interesting artifacts related to the Emerald Buddha and the Grand Palace.

Quiet Spots: If you need a break from the crowds, head to the quieter gardens and courtyards within the complex. They offer a peaceful retreat and beautiful photo opportunities.

Visiting the Grand Palace is a highlight of any trip to Bangkok, providing a rich historical and cultural experience. With these tips, you can ensure a smooth and memorable visit.

The Grand Palace Bangkok Thailand The Grand Palace Bangkok Thailand The Grand Palace Bangkok Thailand The Grand Palace Bangkok Thailand

The Grand Palace Bangkok Thailand

Temple of the Emerald Buddha

Temple of the Emerald Buddha

Known as Wat Phra Kaew (Wat Phra Sri Rattana Satsadaram), is located within the Grand Palace complex in Bangkok, Thailand. This temple is one of the most important and revered Buddhist temples in Thailand, housing the highly venerated Emerald Buddha statue.

Key Highlights of Wat Phra Kaew:

Emerald Buddha: The statue itself is carved from a single block of jade (not emerald, despite the name) and is considered the palladium of Thailand. It is believed to have miraculous powers and is a symbol of the Thai state.

Royal Robes: The Emerald Buddha is adorned with seasonal costumes, which are changed three times a year by the King of Thailand during a special ceremony to mark the changing seasons (summer, rainy season, and winter).

Architectural Beauty: Wat Phra Kaew is renowned for its stunning architecture and intricate detail. The temple is adorned with gold leaf, mosaics, and murals depicting various scenes from Buddhist mythology.

Murals and Art: The inner walls of the temple complex are covered with murals depicting the Ramakien, the Thai version of the Indian epic Ramayana.

Tips for Visiting Wat Phra Kaew within the Grand Palace:

Strict Dress Code: As with the rest of the Grand Palace, Wat Phra Kaew has a strict dress code. Ensure you are dressed modestly, with shoulders and knees covered.

Respect the Rules: Photography is not allowed inside the main temple building where the Emerald Buddha is housed. Be respectful and follow all guidelines.

Best Time to Visit: Early morning visits are ideal to avoid the crowds and heat. The temple and palace complex open at 8:30 AM.

Explore the Entire Complex: Besides the Emerald Buddha, the Wat Phra Kaew complex includes several other important buildings and statues worth exploring. Take your time to walk around and appreciate the detailed artistry.

By visiting Wat Phra Kaew, you get to experience one of the most sacred sites in Thailand and witness the cultural and spiritual heritage that it embodies.

Temple of the Emerald Buddha

Wat Pho (Temple of the Reclining Buddha)

Wat Pho (Temple of the Reclining Buddha)Wat Pho (Temple of the Reclining Buddha)Wat Pho (Temple of the Reclining Buddha)Wat Pho (Temple of the Reclining Buddha)Wat Pho (Temple of the Reclining Buddha)Wat Pho (Temple of the Reclining Buddha)

Wat Arun Ratchawararam Ratchawaramahawihan

Wat Arun Ratchawararam Ratchawaramahawihan, commonly known as Wat Arun.

Commonly known as Wat Arun or the Temple of Dawn, is one of Bangkok’s most famous landmarks. This Buddhist temple is situated on the Thonburi west bank of the Chao Phraya River and is renowned for its stunning architecture and riverside location.

Why It’s Worth Visiting:

Wat Arun is famous for its central prang (tower) which is encrusted with colourful porcelain and seashells. This central spire is surrounded by four smaller towers and represents Mount Meru, the centre of the universe in Buddhist cosmology.

The temple dates back to the Ayutthaya period and has a rich history intertwined with the history of Bangkok and Thailand. It was named after Aruna, the Indian God of Dawn, and has been a significant spiritual site for centuries.

The temple offers breathtaking views, especially at sunrise and sunset. Climbing the central prang provides panoramic vistas of the Chao Phraya River and the surrounding cityscape.

Visiting Wat Arun provides insight into Thai culture and Buddhism. The intricate designs and statues, including depictions of the Buddha’s life, offer a glimpse into traditional Thai art and religious practices.

How to Make the Most of Your Visit:

Early morning or late afternoon are the best times to visit to avoid the heat and crowds. Sunset visits are particularly beautiful as the temple is illuminated.

As a place of worship, visitors should dress modestly. Wear clothes that cover your shoulders and knees.

Take time to explore the various structures within the temple complex, including the central prang, the ordination hall, and the pavilions.

Consider hiring a guide or using an audio guide to learn more about the temple’s history, significance, and architectural details.

Don’t forget your camera. The temple’s intricate details and the scenic river backdrop offer excellent photo opportunities.

Arriving or departing by boat adds to the experience, providing a picturesque view of the temple from the river.

Be mindful of local customs and rules. Keep your voice low, don’t touch religious artifacts, and be respectful of those who are there to worship.

Wat Arun is not just a visual marvel but a deep cultural and spiritual experience, making it a must-visit when in Bangkok.

Cat and Bird Attack!

Best Food Ever Bangkok Thailand

Khaosan Road Bangkok Thailand Saranrom Park Monitor Lizard cheeringup.info #MonitorLizard #SaranromPark #Bangkok #Thailand

Saranrom Park in Bangkok is known for being home to various types of lizards, but the most notable among them are the Asian water monitors (Varanus salvator). These large lizards are commonly seen in parks and canals throughout Bangkok. They can grow quite large, often reaching lengths of up to 2-3 meters. These monitors are semi-aquatic, frequently seen swimming in the park’s ponds and waterways or basking on the banks.

What are the taxes in Thailand?

In Thailand, the tax system includes various types of taxes for individuals and businesses. Here is an overview:

Individual Income Tax

Residents: Individuals who reside in Thailand for 180 days or more within a calendar year are subject to personal income tax on their worldwide income.

Non-residents: Individuals who stay less than 180 days are taxed only on income sourced within Thailand.

Tax Rates:

0% for income up to THB 150,000

5% for income from THB 150,001 to THB 300,000

10% for income from THB 300,001 to THB 500,000

15% for income from THB 500,001 to THB 750,000

20% for income from THB 750,001 to THB 1,000,000

25% for income from THB 1,000,001 to THB 2,000,000

30% for income from THB 2,000,001 to THB 5,000,000

35% for income over THB 5,000,000

Corporate Income Tax

Standard Rate: 20% on net profits.

Small and Medium Enterprises (SMEs): Reduced rates are available based on profit thresholds.

Value Added Tax (VAT)

Standard Rate: 7%

Certain goods and services are exempt, such as agricultural products, educational services, and healthcare services.

Specific Business Tax (SBT)

Applies to certain businesses like banking and real estate.

Rates vary depending on the type of business, generally ranging from 0.1% to 3%.

Withholding Tax

Applied to various payments including dividends, interest, royalties, and service fees.

Rates vary:

Dividends: 10%

Interest: 15%

Royalties: 15%

Service fees: 3% (for domestic) and 5% (for international).

Property Tax

Land and Building Tax: Implemented in 2020, it taxes land and buildings based on their usage (residential, agricultural, commercial, or unused). Rates range from 0.01% to 0.7%.

Transfer Fee: 2% of the appraised value.

Specific Business Tax (on property transfer): 3.3% if applicable.

Other Taxes

Excise Tax: Applied to specific goods such as alcohol, tobacco, and fuel.

Stamp Duty: Levied on certain legal documents and transactions.

Tax Incentives

Thailand offers various tax incentives through the Board of Investment (BOI), including tax holidays and exemptions to promote investment in targeted sectors.

These rates and regulations are subject to change, so it’s advisable to consult with a tax professional or the Revenue Department of Thailand for the most current information.

9 Powerful Techniques to Harness Your Reticular Activating System and Achieve Your Goals in the UK

In the pursuit of success and fulfillment, understanding the mechanisms of the mind is paramount. One such mechanism, the reticular activating system (RAS), plays a crucial role in shaping our experiences and outcomes in life. Situated in the brainstem, the RAS filters incoming information, directing our attention towards what we perceive as important. By learning to train and harness this system effectively, individuals can significantly enhance their ability to achieve their desired goals and aspirations. In this article, we delve into the concept of the reticular activating system and explore nine powerful techniques to train it for success, specifically tailored for individuals in the United Kingdom.

Understanding the Reticular Activating System:

The reticular activating system serves as a filter for sensory information, determining what stimuli are relevant and deserving of our attention. It acts as a gatekeeper, selectively allowing certain information to reach our conscious awareness while filtering out the rest. This function is crucial for our survival, as it helps us focus on essential tasks and stimuli in our environment.

How the RAS Influences Your Life:

The RAS influences various aspects of our lives, from our perceptions and beliefs to our actions and behaviours. By understanding how this system operates, individuals can gain greater control over their thoughts and actions, leading to more intentional and purposeful living.

Set Clear Goals: One of the most effective ways to train your RAS is by setting clear, specific goals. When you define your objectives with clarity and precision, you provide your RAS with a clear target to focus on. Whether it’s achieving a career milestone, improving your health, or enhancing your relationships, clearly defined goals activate your RAS, directing your attention and resources towards their attainment.

Visualise Your Success: Visualisation is a powerful tool for training the RAS. By vividly imagining yourself achieving your goals, you send powerful signals to your brain, reinforcing the desired outcomes and activating the RAS to seek opportunities that align with your vision. Spend time each day visualising your success in detail, engaging all your senses to make the experience as real and tangible as possible.

Practice Gratitude: Gratitude is another effective way to train your RAS for success. When you focus on the things you’re thankful for, you shift your attention towards positive experiences and opportunities, effectively reprogramming your RAS to seek out more of the same. Make it a habit to express gratitude daily, whether through journaling, meditation, or simply reflecting on the blessings in your life.

Surround Yourself with Positivity: The company you keep has a significant impact on your RAS. Surround yourself with positive, supportive individuals who uplift and inspire you. Their energy and attitude will influence your own, reinforcing positive thought patterns and behaviours that align with your goals.

Utilise Affirmations: Affirmations are powerful statements that help reprogramme your subconscious mind and activate your RAS for success. Create affirmations that reflect your goals and aspirations, and repeat them regularly with conviction and belief. By consistently affirming the outcomes you desire, you send powerful signals to your RAS, guiding it towards opportunities that align with your intentions.

Embrace Continuous Learning: Stagnation is the enemy of progress. To keep your RAS sharp and receptive to new opportunities, embrace a mindset of continuous learning and growth. Whether it’s through formal education, self-study, or experiential learning, seek out opportunities to expand your knowledge and skills. The more you learn, the more avenues your RAS will explore, leading to greater success and fulfillment.

Take Inspired Action: While setting goals and visualising success are essential, they must be followed by action. Take inspired action towards your goals, trusting that your RAS will guide you towards the right opportunities and resources. Break down your goals into manageable steps, and consistently take action towards their attainment. Each step you take reinforces your commitment and activates your RAS, propelling you closer to success.

Monitor Your Thoughts: Your thoughts have a profound impact on your RAS. Negative thought patterns and self-limiting beliefs can inhibit its effectiveness, leading to missed opportunities and unfulfilled potential. Practice mindfulness and self-awareness to monitor your thoughts regularly. When negative or limiting beliefs arise, challenge them and replace them with empowering alternatives that support your goals and aspirations.

Celebrate Your Successes: Finally, celebrate your successes along the way. Acknowledge and appreciate the progress you’ve made, no matter how small. Celebrating your achievements reinforces positive behaviour and activates your RAS to seek out more opportunities for success and fulfillment.

The reticular activating system plays a pivotal role in shaping our experiences and outcomes in life. By understanding how this system operates and implementing the techniques outlined in this article, individuals can train their RAS for success and achieve their goals with greater clarity and purpose. Whether you’re pursuing career advancement, personal growth, or improved relationships, harnessing the power of your RAS can unlock a world of opportunities and possibilities, leading to a more fulfilling and rewarding life in the United Kingdom.

15 Transformative Steps to Reinvent Yourself After 55 in the UK

Reinventing oneself is not exclusive to any age group; it’s a journey of continuous growth and self-discovery. However, for individuals over 55 in the UK, embarking on this journey can be particularly empowering and liberating. Whether driven by a desire for personal fulfillment, a career change, or simply a new chapter in life, reinvention offers endless possibilities. Here are 15 transformative steps to help you reinvent yourself after 55 in the UK.

Reflect on Your Passions and Strengths: Take time to reflect on what truly ignites your passion and what you excel at. Consider your hobbies, past experiences, and skills acquired over the years. Identifying your strengths will lay the foundation for your reinvention journey.

Set Clear Goals: Define specific, achievable goals that align with your passions and strengths. Whether it’s starting a new business, pursuing further education, or exploring a creative endeavour, clarity in your objectives will guide your reinvention process.

Embrace Lifelong Learning: In today’s fast-paced world, continuous learning is key to staying relevant and adaptable. Explore educational opportunities such as online courses, workshops, or even pursuing a degree in a field of interest. Lifelong learning not only enhances your skills but also keeps your mind sharp and engaged.

Embrace Technology: Embrace technology as a tool to facilitate your reinvention efforts. From building an online presence to learning new digital skills, technology opens up a world of opportunities for career transitions, networking, and personal growth.

Explore Flexible Work Arrangements: With the rise of remote work and flexible schedules, explore opportunities that allow you to balance work with other passions and interests. Consider freelancing, consulting, or part-time roles that offer flexibility and autonomy.

Cultivate Resilience: Reinvention often involves stepping out of your comfort zone and facing challenges along the way. Cultivate resilience by embracing failure as a learning opportunity, practicing self-care, and maintaining a positive mindset even in the face of setbacks.

Volunteer and Give Back: Engage in volunteer work or community service as a way to contribute to society while exploring new interests and passions. Not only does volunteering provide a sense of fulfillment, but it also expands your social network and exposes you to new experiences.

Prioritise Health and Wellness: Investing in your physical and mental well-being is essential for a successful reinvention journey. Prioritise regular exercise, healthy eating, and stress management techniques such as meditation or mindfulness to ensure you have the energy and resilience to pursue your goals.

Embrace Creativity: Tap into your creative side and explore artistic endeavours such as painting, writing, or music. Creativity not only fosters self-expression but also stimulates innovation and problem-solving skills, essential qualities for reinvention.

Travel and Explore New Cultures: Travelling provides an opportunity to gain new perspectives, broaden your horizons, and immerse yourself in different cultures. Whether it’s a solo adventure or group tour, travelling can inspire creativity, spark new interests, and fuel your reinvention journey.

Stay Curious and Open-Minded: Approach life with a curious and open-minded attitude, embracing new experiences and opportunities as they arise. Be willing to challenge assumptions, explore unconventional paths, and adapt to changing circumstances on your journey of reinvention.

Seek Professional Guidance: Consider seeking guidance from career coaches, counsellors, or therapists who specialise in midlife transitions. Professional support can provide valuable insights, clarity, and accountability as you navigate the complexities of reinvention.

Celebrate Progress and Milestones: Celebrate your achievements, no matter how small, and acknowledge the progress you’ve made on your reinvention journey. Take time to reflect on your accomplishments, learn from your experiences, and recalibrate your goals as needed.

Stay Connected to Your Purpose: Throughout your reinvention journey, stay connected to your core values and sense of purpose. Align your goals and actions with what truly matters to you, and let your passion and purpose drive your continued growth and transformation.

Reinventing yourself after 55 in the UK is an opportunity to embrace new beginnings, explore untapped potential, and create a life that aligns with your passions and aspirations. By reflecting on your strengths, setting clear goals, and embracing lifelong learning, you can embark on a transformative journey of self-discovery and personal growth. With resilience, curiosity, and an open mind, the possibilities for reinvention are endless, allowing you to write the next chapter of your life with confidence and purpose.

Join our Retirement Club to be inspired to live a better life in retirement in UK

What happens if you don t have enough money for retirement UK? Long life secure your future.

24 ways to avoid the Looming retirement crisis in uk from living too long – with not enough money

While living a long life is a positive thing, it can strain retirement finances if you haven’t prepared adequately. Here are 24 ways to address the challenge of longevity and potential shortfalls in retirement income:

Financial Planning

Start Saving Early: The earlier you start saving, the more time your money has to grow through compound interest.

Increase Contribution Rates: Even small increases to your pension contributions can significantly boost your retirement nest egg.

Maximise Employer Matching: Contribute enough to your workplace pension to get the full employer match, essentially free money.

Track Your Spending: Understanding your spending habits helps identify areas where you can cut back and free up more money for savings.

Create a Retirement Budget: Estimate your retirement expenses to determine how much you need to save.

Debt Management

Pay Off High-Interest Debt: High-interest debts can quickly eat away at your retirement savings.

Develop a Debt Repayment Plan: Create a strategy to eliminate debt before or during retirement.

Avoid Unnecessary Debt: Be mindful of taking on new debt, especially close to retirement.

Lifestyle Adjustments

Consider Downsizing Your Home: Moving to a smaller home can free up equity and reduce housing costs.

Explore Affordable Housing Options: Consider retirement communities or co-housing arrangements for affordability.

Reduce Discretionary Spending: Analyse your spending and cut back on non-essential expenses.

Embrace Frugal Living: Find ways to enjoy life without spending a lot of money.

Travel During Off-Peak Seasons: Travelling during shoulder seasons can be significantly cheaper.

Explore Free or Low-Cost Activities: Many hobbies and leisure activities don’t require a lot of money.

Income Strategies

Delay Retirement:Working a few extra years allows you to contribute more to your retirement savings and receive a higher state pension.

Pursue a Side Hustle: A part-time job or freelance work can supplement your retirement income.

Rent Out a Room or Property: Renting out a spare room or property can generate additional income.

Invest in Income-Generating Assets: Consider investments like dividend-paying stocks or rental properties.

Government Support

Understand State Pension Benefits: Research the eligibility requirements and amount of state pension you’ll receive.

Explore Pension Credit: This benefit tops up your state pension if your income is low.

Seek Free Financial Advice: The government offers free financial guidance to help you plan for retirement.