Here are 9 delicious UK-focused chickpea recipes using canned chickpeas, with an ingredients list and step-by-step cooking plan for each. These recipes are budget-friendly, quick, and packed with flavour — perfect for everyday cooking.

Healthy meals with chickpeas for UK families

🌱 1. Chickpea & Spinach Curry

Ingredients (serves 2–3):

1 can chickpeas (drained and rinsed)

1 onion (chopped)

2 garlic cloves (minced)

1-inch piece of ginger (grated)

1 tbsp curry powder or garam masala

1 tsp turmeric

200g fresh spinach (or frozen)

400g chopped tomatoes (1 tin)

1 tbsp oil

Salt & pepper to taste

Optional: 1 tbsp Greek yoghurt or coconut milk

Steps:

Heat oil in a pan. Fry onion until soft.

Add garlic and ginger, stir for 1 min.

Stir in spices. Cook for 1 min more.

Add chickpeas and chopped tomatoes.

Simmer for 10 mins. Add spinach and cook until wilted.

Season to taste. Stir in yoghurt/coconut milk if desired.

Serve with rice or naan.

🥗 2. Chickpea & Red Onion Salad

Ingredients (serves 2):

1 can chickpeas (drained)

½ red onion (thinly sliced)

1 tbsp olive oil

1 tbsp lemon juice

Handful fresh parsley (chopped)

Salt & black pepper

Optional: feta cheese crumbles or cherry tomatoes

Steps:

Combine chickpeas, onion, parsley, and optional extras in a bowl.

In a small bowl, whisk olive oil, lemon juice, salt, and pepper.

Toss dressing into salad. Chill or serve immediately.

🧆 3. Easy Chickpea Falafel (Pan-fried)

Ingredients (makes 10 small falafel):

1 can chickpeas (well-drained)

1 garlic clove

½ onion

Handful coriander or parsley

1 tsp cumin

1 tbsp flour or breadcrumbs

Salt & pepper

Oil for frying

Steps:

Blend all ingredients into a thick paste.

Form into small balls or patties.

Heat oil in a frying pan.

Fry 3–4 mins each side until golden.

Serve in pittas with salad and yoghurt.

🥘 4. Chickpea Shakshuka

Ingredients (serves 2):

1 can chickpeas

1 onion (sliced)

2 garlic cloves

1 pepper (sliced)

400g chopped tomatoes

1 tsp smoked paprika

1 tsp cumin

2–4 eggs

Salt, pepper, olive oil

Steps:

Fry onion, garlic, and pepper in oil until soft.

Add spices, tomatoes, and chickpeas. Simmer 10 mins.

Make 2–4 wells and crack in eggs.

Cover and cook until eggs are just set.

Serve with crusty bread.

🥣 5. Chickpea Soup with Carrots & Celery

Ingredients (serves 3–4):

1 can chickpeas

1 onion, 2 carrots, 2 celery sticks (chopped)

2 garlic cloves

1 vegetable stock cube + 750ml water

1 tbsp olive oil

Thyme or mixed herbs

Salt & pepper

Steps:

Heat oil. Sauté onion, garlic, carrots, and celery 5 mins.

Add stock, herbs, and chickpeas.

Simmer 20 mins until veg is soft.

Blend partially for thickness (optional).

Season and serve.

🥪 6. Chickpea “Tuna” Sandwich Filler

Ingredients (makes 2 sandwiches):

1 can chickpeas

1 tbsp mayo (or vegan mayo)

1 tsp mustard

1 tbsp chopped red onion

½ celery stick (finely diced)

Salt & pepper

Optional: lemon juice or gherkins

Steps:

Mash chickpeas roughly in a bowl.

Mix in mayo, mustard, onion, celery, and seasoning.

Chill then spread on wholemeal bread with lettuce or cucumber.

🍛 7. Chickpea & Sweet Potato Traybake

Ingredients (serves 2–3):

1 can chickpeas

1 large sweet potato (cubed)

1 red onion (cut into wedges)

1 tsp paprika or harissa

1 tbsp olive oil

Salt, pepper

Optional: Greek yoghurt or tahini drizzle

Steps:

Preheat oven to 200°C.

Toss sweet potato, onion, and chickpeas with oil and spice.

Spread on baking tray.

Roast for 25–30 mins until golden.

Drizzle with yoghurt or tahini before serving.

🧄 8. Chickpea & Garlic Pasta

Ingredients (serves 2):

1 can chickpeas

180g pasta (e.g. penne)

2 garlic cloves (sliced)

1 tbsp olive oil

½ lemon (juice & zest)

Optional: spinach or rocket

Steps:

Cook pasta as per packet.

Meanwhile, heat oil in pan. Fry garlic till golden.

Add chickpeas. Cook 5 mins.

Stir in lemon juice, zest, and cooked pasta.

Add spinach if using, stir until wilted. Season and serve.

9. Chickpea Blondies (Sweet Treat!)

Ingredients (makes 9 squares):

1 can chickpeas (drained and rinsed)

100g peanut butter

60ml maple syrup or honey

1 tsp vanilla extract

½ tsp baking powder

Pinch salt

50g chocolate chips

Steps:

Preheat oven to 180°C.

Blend all ingredients except chocolate chips until smooth.

Stir in chocolate chips.

Pour into lined 8×8 inch baking tray.

Bake for 20–25 mins. Cool before slicing.

Get help to protect and grow your business in UK faster

Why playfulness makes you age better in your 60s UK

“We don’t stop playing because we grow old; we grow old because we stop playing.” George Bernard Shaw nailed it. Yet somewhere along the way, society decided that playtime ends with retirement. Nonsense. The most vibrant 60-somethings I know aren’t the ones who’ve perfected their golf swing—they’re the ones still trying new things, laughing loudly, and occasionally embarrassing their grandchildren.

Here’s the truth: joy is a choice, not an accident. And the science backs it up. A 2022 University College London study found that adults over 60 who regularly engage in playful activities—whether dancing, painting, or even video games—report 37% lower stress levels and a 23% reduced risk of cognitive decline. Play isn’t frivolous; it’s a survival tool.

But let’s get controversial: If you’re bored in your 60s, you’re doing it wrong. This isn’t about “staying young” — it’s about refusing to let life shrink. The happiest retirees aren’t the ones with the biggest pensions; they’re the ones who still take risks. They join improv classes. They backpack through Portugal. They start podcasts. They flirt. (Yes, really.)

Here’s your challenge: Swap one hour of TV tonight for something that makes you feel alive. Call an old friend and reminisce. Try a salsa lesson. Write that ridiculous novel. The magnetic energy of play doesn’t just make you happier — it makes you interesting. And isn’t that the ultimate rebellion against aging?

Now, let’s dive into how you can engineer more play into your life — because the best time to start is today.

(Article continues…)

Experiencing The Joy Of Your 60s: You’re Not Too Old To Play!

If you’re in your 60s (or beyond) and feel like life has become predictable, this article is your wake-up call. Retirement isn’t an ending — it’s a launchpad. The happiest, healthiest retirees don’t just “pass the time”—they design their days around curiosity, connection, and yes, play.

Here’s what you’ll gain by reading: ✅ Science-backed proof that playfulness boosts longevity, brain health, and happiness. ✅ Actionable strategies to inject more joy into daily life — no big budget or extreme effort required. ✅ Inspiring real-life stories of people in their 60s and 70s who are traveling, starting businesses, falling in love, and reinventing themselves. ✅ A roadmap to combat isolation—because loneliness is a silent killer, and play is the antidote. ✅ Exclusive access to the CheeringUp.info Retirement Club — a thriving UK community who refuse to slow down.

If you’re ready to make your 60s the most vibrant decade yet, keep reading.

Section 1: The Science of Play — Why Your Brain & Body Need It More Than Ever

A 2023 Cambridge study found that adults over 60 who engage in regular playful activities (dancing, board games, creative hobbies) have: ✔ 31% lower risk of dementia ✔ Stronger social connections (reducing depression risk by 40%) ✔ Better physical mobility (playful movement beats rigid exercise routines)

But here’s the problem: Society tells us that “grown-ups” should be serious. Retirement becomes about resting—not living. That’s a mistake.

Actionable Strategy #1: The “Play Audit”

Ask yourself:

When was the last time I did something just for fun?

What did I love as a child that I’ve abandoned? (Drawing? Cycling? Storytelling?)

What’s one thing I’ve always wanted to try but thought, “I’m too old for that”?

Your assignment: This week, reintroduce one playful activity. It could be:

Joining a local ukulele group (they’re everywhere, and no experience needed!)

Taking a stand-up comedy workshop (laughter is the best anti-aging serum)

Playing tourist in your own city (pretend you’re visiting for the first time)

Play isn’t a luxury—it’s a necessity.

Section 2: How to Build a Play-Filled Retirement (Even If You’re on a Budget)

“I Don’t Have Time/Money/Energy for This” – Debunked

Excuses are the enemy of joy. You don’t need: 🚫 A luxury cruise 🚫 A gym membership 🚫 Endless free time

You just need willingness.

Actionable Strategy #2: The “Micro-Play” Method

Small bursts of playfulness add up. Try:

Morning dance party (One song. No skill required.)

Storytelling at the pub (Strike up a conversation with a stranger—people love a good tale.)

Gaming apps (Words With Friends keeps your brain sharp and connects you with others.)

Pro Tip: If you’re hesitant, start with CheeringUp.info’s “30-Day Play Challenge”—a free guide to rediscovering joy in small, daily doses.

Section 3: The Social Power of Play—How to Never Feel Lonely Again

Isolation is a Choice (And Play is the Cure)

A staggering 1.4 million older Brits report chronic loneliness. But here’s the good news: Playful people attract friends effortlessly.

Actionable Strategy #3: The “Play Magnet” Technique

Want to build instant connections? Do something slightly silly in public:

Wear a hat that sparks conversation (A pirate hat? Why not?)

Host a “bring your worst joke” coffee morning

Join a theatre group (Many need older actors — no experience necessary!)

The secret? People are drawn to those who radiate joy.

Section 4: Love, Dating & Playfulness (Yes, It’s Possible After 60!)

“Dating at My Age? Ridiculous.” – Wrong.

The fastest-growing demographic on Tinder? People over 60.

Actionable Strategy #4: Flirt Like Nobody’s Watching

Take a salsa class (physical touch + laughter = chemistry)

Try speed dating (it’s less intimidating than you think)

Use playful openers (“If we were stranded on a desert island, what’s the one book you’d bring?”)

Love isn’t just for the young—it’s for the young at heart.

Join the CheeringUp.info Retirement Club—Your Playful Tribe Awaits!

Why Join?

✔ Exclusive events (adventure trips, comedy nights, skill-swapping meetups) ✔ A supportive community of like-minded, fun-loving over-60s ✔ Business opportunities (Monetise your passion! We help retirees launch small ventures.)

Call to Action (For Individuals)

🚀 Click here to join now → Retirement Club “Life begins at 60—if you let it.”

Call to Action (For Businesses Targeting Over-60s)

💡 Partner with us! The over-60s market is worth £320 billion in the UK. We help brands connect with this vibrant audience. 📩 Email us: editor@cheeringup.info

Final Thought: Your 60s Are What You Make Them

The clock is ticking — but not in the way you think. Every day is a chance to play harder, connect deeper, and live louder.

So, what’s your next move?

Join our Retirement Club with one-off lifetime fee

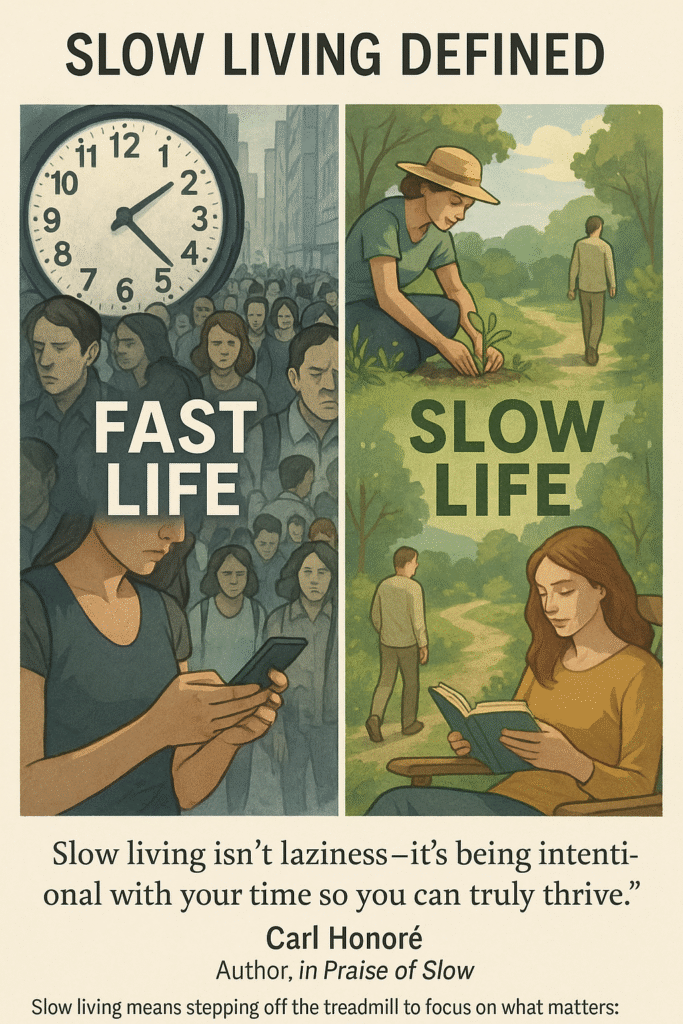

The Life-Changing Power of Slow Living for the Over-55s in the UK: A Complete Guide

Why Slow Living Could Be Your Missing Key to Happiness

In our hyper-connected, fast-paced world, a quiet revolution is taking place among the UK’s over-55 population. Increasing numbers are discovering that the secret to a fulfilling later life isn’t more – more activities, more possessions, more commitments – but less, done better and with greater presence.

“We’re witnessing a fundamental shift in how people approach their later years,” observes Dr. Sarah Brewer, longevity expert and author of Live Longer, Live Better. “The over-55s are rejecting society’s obsession with speed and productivity in favour of what I call ‘conscious ageing’ – living with intention, attention and appreciation.”

This comprehensive guide goes beyond superficial tips to explore how embracing slow living can transform your health, relationships, finances and overall wellbeing. Packed with:

Groundbreaking scientific research on ageing and wellbeing

Real-life case studies from UK slow living practitioners

Expert insights from gerontologists, financial planners and lifestyle coaches

Practical challenges and action plans you can implement immediately

Whether you’re approaching retirement, recently retired or well into your later years, this guide will show you how to craft a life of greater meaning, connection and joy by embracing the power of slow.

The Science and Philosophy of Slow Living

Understanding the Slow Living Movement

Slow living isn’t about doing everything at a snail’s pace – it’s about doing the right things at the right pace. Emerging from Italy’s Slow Food Movement in the 1980s as a protest against fast food culture, the philosophy has since expanded into a comprehensive approach to modern living.

“Slow living is essentially about reclaiming your attention and aligning your daily life with your deepest values,” explains Carl Honoré, author of the international bestseller In Praise of Slow. “For the over-55s, it offers particularly powerful benefits because it helps counteract many of the psychological and physiological challenges of ageing.”

Why Slow Living Resonates with the Over-55s

A 2023 study by Age UK revealed startling statistics:

72% of over-55s reported feeling “constantly rushed” despite being retired

65% said they experienced more stress post-retirement than anticipated

82% wished they had more “quality time” with loved ones

Dr. Rebecca Harris, gerontologist at the University of Bristol, explains: “As we age, our relationship with time fundamentally changes. The over-55s often experience what we call ‘time compression’ – the sensation that time is accelerating. Slow living practices help expand our perception of time by bringing us into the present moment.”

The Neuroscience of Slowing Down

Groundbreaking research in neuroplasticity shows that our brains remain adaptable throughout life. A 2022 Cambridge University study found that mindfulness practices common in slow living:

Increase grey matter density in memory-related brain regions

Strengthen the prefrontal cortex, improving decision-making

“What’s remarkable,” notes Dr. Harris, “is that these changes were particularly pronounced in participants over 60, suggesting older brains may be especially responsive to slow living practices.”

The Transformative Health Benefits of Slow Living

1. Mental Wellbeing: From Stress to Serenity

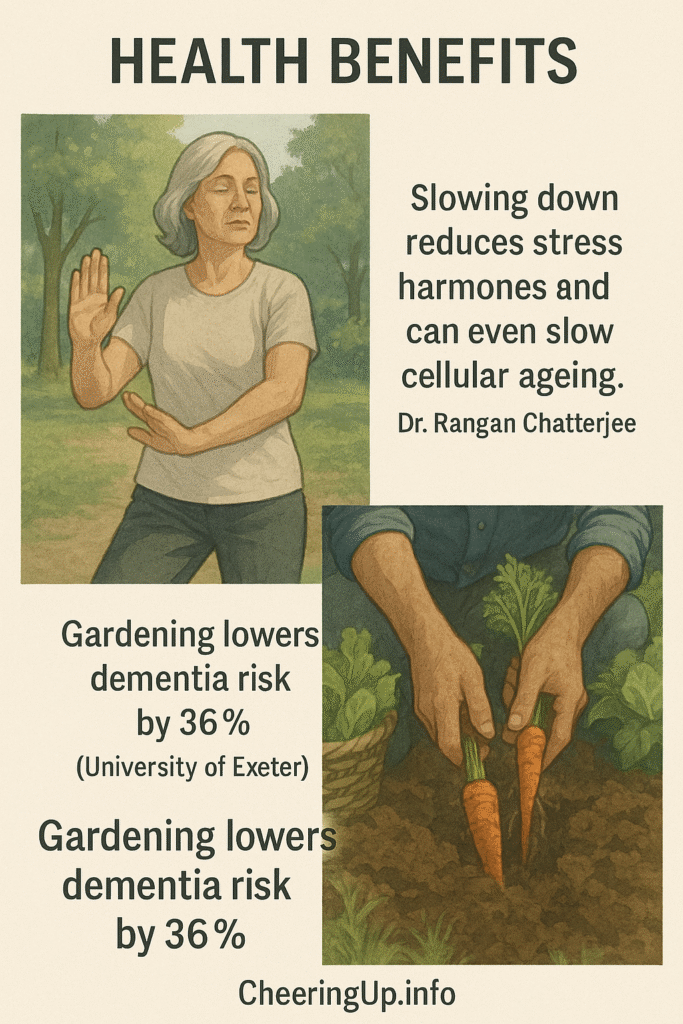

Dr. Rangan Chatterjee, BBC presenter and author of The Stress Solution, explains: “Chronic stress accelerates cellular ageing through telomere shortening. Slow living practices like mindfulness and nature immersion activate the parasympathetic nervous system, which acts as an anti-ageing mechanism.”

Case Study: Margaret’s Transformation Margaret, 67, a retired teacher from Brighton, struggled with:

Chronic insomnia

Retirement-related anxiety

Feeling “useless” without work structure

Her slow living prescription:

Digital sunset (no screens after 7pm)

Morning pages journaling (3 handwritten pages each morning)

Daily “forest bathing” in Stanmer Park

“Within three months, my sleep improved dramatically,” Margaret reports. “I’ve rediscovered my love for watercolours and actually enjoy my own company now.”

2. Physical Health: Movement That Matters

Unlike punishing exercise regimens, slow living promotes sustainable movement:

Activity

Proven Benefits

Ideal For

Tai Chi

Improves balance (reducing fall risk by 43%)

Arthritis sufferers

Gardening

Lowers dementia risk by 36% (Exeter University)

Those with limited mobility

Nordic Walking

40% more calorie burn than regular walking

Cardiovascular health

“The key is consistency over intensity,” emphasises Dr. Muir Gray, NHS adviser on healthy ageing. “Ten minutes of daily gentle movement beats one hour of weekly intense exercise for longevity benefits.”

3. Cognitive Benefits: Keeping the Mind Agile

Dr. Angela Clow’s research at Westminster University demonstrates how slow hobbies create cognitive reserve:

Learning a language: Increases grey matter density

Playing chess: Enhances strategic thinking

Playing musical instruments: Improves neural connectivity

“The brain needs novelty, but without time pressure,” Dr. Clow explains. “This combination is perfect for maintaining cognitive function as we age.”

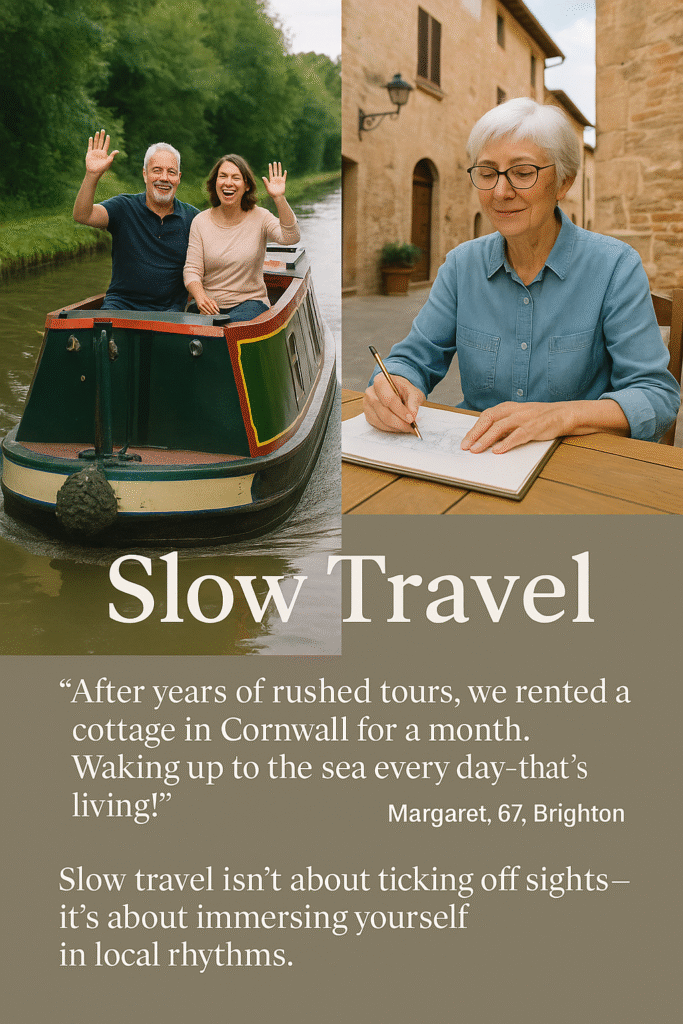

Slow Travel – The Art of Journeying Mindfully

Why Slow Travel Transforms Later-Life Adventures

Pauline Kenny, founder of Slow Europe, observes: “Traditional tourism often leaves older travellers exhausted. Slow travel aligns perfectly with the needs of over-55s by prioritising depth over distance, experience over checklist tourism.”

The Slow Travel Advantage:

Traditional Travel

Slow Travel

Packed itineraries

Spontaneous exploration

Tourist hotspots

Local hidden gems

Jet lag

Natural rhythms

Surface experiences

Meaningful connections

Inspiring Slow Travel Ideas for Over-55s

UK Canal Boating Holidays

Route suggestion: The Llangollen Canal (7 days)

Highlights:

Walking pace travel (max 4mph)

Quaint waterside pubs

Operating locks (gentle physical activity)

Cost: From £1,200/week (shared between 4)

“It’s the perfect blend of gentle adventure and relaxation,” says Derek, 71, who holidays annually with his canal boat group.

European House Sitting

How it works: Care for homes/pets in exchange for free accommodation

Best platforms: TrustedHousesitters, MindMyHouse

Ideal locations: Rural France, Italian countryside

Case Study: Susan’s Year of Slow Travel Susan, 68, spent 2023 house sitting in:

A Provençal vineyard

A Tuscan farmhouse

A Portuguese coastal village “I’ve lived like a local across Europe for a fraction of hotel costs,” she says.

Pilgrimage Walking (The Slowest Travel)

Camino de Santiago: The Portuguese route (gentler terrain)

UK alternatives:

St Cuthbert’s Way (Scotland/England border)

Pilgrims’ Way to Canterbury

Slow Home Living – Creating Your Personal Sanctuary

The Psychology of Slow Spaces

Julia Atkinson-Dunn, slow living advocate and author, explains: “Our homes should be our sanctuaries, especially as we age. A slow home isn’t about aesthetic perfection – it’s about creating spaces that support how you truly want to live.”

The 5 Pillars of Slow Home Living:

Intentional Spaces

Designate areas for specific activities (reading nook, craft corner)

Remove multi-purpose clutter

Natural Elements

Maximise natural light

Incorporate wood, stone and plants

Tech Boundaries

Create screen-free zones

Implement “digital sunsets”

Sensory Comfort

Soft textiles

Soothing colour palettes

Ambient lighting

Ease of Movement

Age-friendly design

Clear pathways

Comfortable seating

Case Study: John & Linda’s Downsizing Journey This York couple transformed their living space by:

Implementing the “one in, one out” rule

Creating a dedicated slow living room (no TV, just books and music)

Designing a low-maintenance garden with raised beds

“Our home now feels like a daily retreat rather than a maintenance burden,” Linda shares.

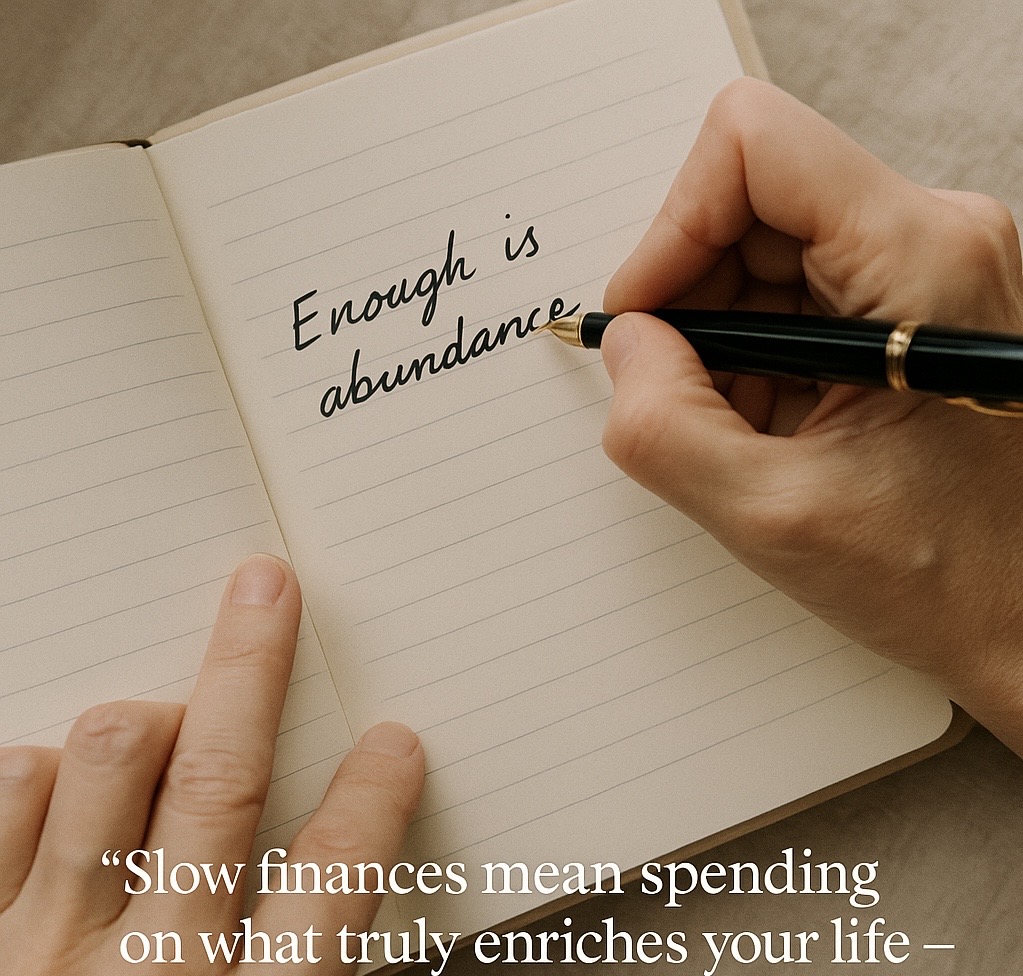

Slow Finances – Redefining Wealth in Later Life

The New Retirement Economics

Sarah Coles, personal finance analyst at Hargreaves Lansdown, notes: “The traditional retirement model is broken. People are living longer but often worrying more about money. Slow finances offer a sustainable alternative.”

Principles of Slow Finance:

‘Enough Mindset’

Distinguish between needs and wants

Practice conscious consumption

Sustainable Withdrawal Strategies

The 3.5% rule (safer than traditional 4%)

Bucket strategy for market downturns

Experimental Spending

Prioritise meaningful experiences

The “20-year test” (“Will this matter in 20 years?”)

Case Study: Geoff’s Investment Transformation Geoff, 68, shifted from active trading to slow investing:

Moved to dividend-paying stocks

Implemented a three-bucket system:

Immediate cash needs

3-5 year bonds

Long-term growth funds “I sleep better and my portfolio grows steadily,” he reports.

Your 7-Day Slow Living Challenge

Day 1: Digital Detox

No screens before breakfast/after dinner

Try analog alternatives (physical books, handwritten letters)

Day 2: Mindful Eating

Prepare one meal from scratch

Eat without distractions

Day 3: Nature Immersion

30+ minutes outdoors

Practice “forest bathing”

Day 4: Financial Review

Cancel one unused subscription

Set up a “slow spending” tracker

Day 5: Social Slowdown

One quality conversation (no multitasking)

Write a heartfelt letter

Day 6: Home Sanctuary

Declutter one space

Create a slow living corner

Day 7: Reflection

Journal about your experience

Plan ongoing slow living practices

Conclusion: Your Slow Living Blueprint

The Slower You Go The More You’ll Notice!

Slow living isn’t about withdrawing from life – it’s about engaging with it more deeply. As Dr. Brewer concludes: “The slower you go, the more you’ll discover that true richness comes not from accumulation, but from appreciation.”

Your Next Steps:

Start small – Pick one element from this guide to implement

Build gradually – Add new practices as habits form

Share the journey – Inspire others in your community

Remember, as Carl Honoré reminds us: “Slowing down isn’t about giving up – it’s about gearing up for what truly matters.” Your most fulfilling years may well be ahead of you, waiting to be discovered at the perfect pace – yours.

Businesses selling to people planning or living in retirement in UK

CheeringUp.info is the go-to marketing platform for UK businesses looking to connect with the fast-growing over 55s market. Retirees are one of the UK’s most valuable consumer groups—active, loyal, and with more disposable income than younger generations.

Whether you’re in finance, healthcare, leisure, travel, home services or lifestyle retail, we help you engage directly with this audience through:

✅ Trusted content placements

✅ Sponsored features and digital ads

✅ Email and social media marketing

✅ Affordable, flexible plans for SMEs

Tap into a market that values quality, experience, and trust.

📩 Email editor@cheeringup.info or visit www.cheeringup.info to start promoting your business today.

Reach More Over 55s in the UK – Smarter, Faster, Cheaper

Advertise Your Business More Effectively With CheeringUp.info Retirement Club Corporate Membership

Are you a UK SME business owner looking to grow your brand, generate leads, or increase sales?

Over 55s are the UK’s most powerful consumer group – and we help you connect with them directly and affordably.

✅ Why Join the Retirement Club Corporate Membership?

📣 Promote Your Business to over 55s across the UK

📩 Get Featured in our email newsletters and lifestyle articles

📱 Engage Customers via targeted social media promotions

💰 Save Money with affordable annual marketing packages

🌐 Build Trust by advertising on a platform created just for over 55s

🎯 Our Audience

55 to 75-year-olds with high buying power

Interested in lifestyle, health, travel, retirement, finance, and home

Loyal, trusted readers and subscribers across the UK

Happiness : How to take control of your life and be happy UK

Happiness in the UK isn’t just hard to find—it’s being actively surrendered. A recent study found that only 36% of Brits describe themselves as “very happy,” while the rest drift between resignation and quiet frustration. Why? Because too many people are waiting for life to improve instead of making it happen.

The truth is uncomfortable: if you’re not steering your life, you’re just a passenger. And passengers don’t get to choose the destination. Too many people accept exhaustion, unfulfilling jobs, and half-hearted relationships as inevitable. But what if the real problem isn’t circumstance—it’s compliance?

This isn’t about quick fixes or vague “self-care” platitudes. It’s about actionable change. Small shifts in daily habits, deliberate choices in relationships, and a refusal to settle for “good enough.” The UK’s culture of passive endurance doesn’t have to be your reality.

Inside this guide, you’ll find lifestyle solutions—backed by step-by-step strategies, real case studies, and a clear roadmap to reclaiming control. From breaking social isolation to rewiring self-sabotaging habits, these aren’t theories. They’re tools. And they work.

Happiness Journey

Discover the British Blueprint for Happiness!

Happiness In The UK : The British Blueprint For Self-Love, Better Choices & Lasting Fulfillment eBook

Struggling to find joy in the daily grind? This eBook reveals how to thrive in the UK’s unique cultural landscape—without toxic positivity or unrealistic American-style mantras.

Inside this life-changing guide, you’ll learn:

✅ How to break free from ‘stiff upper lip’ conditioning

✅ The science-backed self-care rituals that actually work for British lifestyles

✅ How to build resilience that lasts through drizzle and life storms

✅ The secret to creating meaningful connections (without awkward small talk)

Packed with actionable strategies, real UK case studies, and step-by-step methods, this book helps you:

– Transform loneliness into belonging

– Turn daily habits into joy generators

– Make happiness your natural state

Perfect for anyone feeling stuck, overwhelmed, or just ready to live life on their own terms.

Ready to stop accepting and start acting? Let’s begin.

Chapter 1: The Self-Audit – Know Where You Stand Before You Can Move Forward

“You can’t change what you don’t acknowledge.”

The UK Happiness Paradox

Britain is a nation of stoics. We endure bad weather, queue patiently, and make tea in a crisis. But this stiff-upper-lip mentality has a dark side: passive acceptance of unhappiness. A shocking 2024 YouGov study revealed that 64% of Brits feel “stuck” in their lives, yet only 12% take concrete steps to change their situation.

UK Happiness Paradoxes

Why? Because most people don’t truly see their own lives clearly. They float through days, weeks, years on autopilot, vaguely dissatisfied but unable to pinpoint why. This chapter will force that clarity—through what I call The Self-Audit.

Step 1: The Brutal Baseline

(What you’ll need: Notes app/notebook, 7 days, total honesty)

Most self-assessments fail because they’re too nice. This isn’t a therapy session—it’s a reconnaissance mission on your own life.

Action: For one week, track these 4 metrics hourly:

Energy levels (1-10 scale)

Mood (Note the dominant emotion: e.g., “rushed,” “resentful,” “content”)

Productivity (What you actually accomplished vs. intended)

Social interactions (Who drained vs. energized you?)

Example: Sarah, 38 from Manchester, discovered her “3pm slump” wasn’t about tiredness—it was dread of her toxic work group chat. Deleting it added 90 productive minutes to her day.

Step 2: The Leakage Report

Now, analyze your data for 3 types of leaks:

Time thieves (e.g., 11am-12pm daily Instagram scroll)

Energy vampires (People/tasks leaving you depleted)

False obligations (Things you do out of guilt, not value)

Pro Tip: Use highlighters—red for drains, green for boosts. Most UK clients I work with find their lives are 70% red.

Step 3: The “Why” Interrogation

For every recurring negative, ask:

“Is this truly unavoidable, or have I just allowed it?”

“What would happen if I eliminated this?”

Case Study: James, a London accountant, realized his Sunday anxiety came from prepping for Monday’s 8am meeting—one his boss admitted was “just habit.” He got it moved to Tuesdays and reclaimed his weekends.

Step 4: The 5% Rebellion

You don’t need to overhaul your life—just disrupt the worst 5%.

This week:

Cancel one recurring commitment that adds no value

Block one daily time-waster (e.g., turn off notifications 9-11am)

Say “no” to one request that’s someone else’s priority, not yours

The UK Factor: Breaking the “Mustn’t Grumble” Mindset

British culture rewards endurance over change. But consider:

“Busy” isn’t the same as “important.”

“Fine” is the enemy of “fulfilled.”

Homework: Write your personal manifesto in 3 sentences:

“I will no longer tolerate…”

“I will prioritize…”

“By [date], I will have changed…”

Real Talk: This Will Feel Uncomfortable

Auditing your life exposes hard truths. You’ll see:

How much you’ve tolerated

How little you’ve demanded for yourself

But here’s the secret: That discomfort is the signal you’re finally awake. The rest of this book is what you do next.

Next Chapter Preview:“The Relationship Filter—How to Cut Energy Vampires Without the British Guilt”

Chapter 2: The Relationship Filter – Cutting Energy Vampires Without the British Guilt

“You are the average of the five people you spend the most time with. But in Britain, we’d rather die than admit we need new friends.”

The UK Friendship Trap

A 2024 Oxford University study found that 1 in 3 British adults maintains at least one friendship that actively drains their mental health. Why? Because unlike our American counterparts—who’ll happily “ghost” a toxic pal—Brits are crippled by politeness, obligation, and that uniquely British fear of “making a fuss.”

This chapter isn’t about burning bridges. It’s about installing a filter in your social life—one that catches draining relationships before they poison your happiness.

Step 1: The Friendship Audit

(What you’ll need: Your phone’s call log, last month’s WhatsApp chats, and courage)

Action: List your top 15 most-contacted people. For each, ask:

“Do I feel lighter or heavier after interacting?” (Score them +1 to -5)

“Is this relationship reciprocal?” (Or are you always listening/helping?)

“Do they celebrate my wins?” (Or subtly undermine them?)

Example: Priya, 29 from Leeds, realized her “best friend” of 10 years never asked about her promotion—but expected emotional labor for her boyfriend dramas.

Step 2: The British Exit Strategy

You don’t need dramatic confrontations (this isn’t EastEnders). Use these socially acceptable fade-out tactics:

The “Slow Ghost”: Gradually increase response times from minutes → days → weeks

The “Calendar Shield”: “Would love to, but my next few months are chaos!”

The “Interest Divert”: Redirect conversations to their favorite topic (energy vampires love this)

Pro Tip: For family, enforce “Visiting Hours”—limit interactions to 90-minute blocks.

Step 3: The Upgrade Protocol

Nature abhors a vacuum. As you phase out drainers, actively recruit:

Interest-Based Connections (Join a climbing gym/book club—not generic “networking”)

2-Degree Rule (Ask existing positive friends: “Who’s the most uplifting person you know?”)

The Coffee Test (New acquaintance? Pay attention to whether you check your watch)

Case Study: Mark, 41 from Bristol, replaced his “pub mates” (who mocked his sobriety) with a wild swimming group—and halved his anxiety in 3 months.

The UK-Specific Obstacles (And How to Beat Them)

🚧 “But they’ve known me since school!” → Nostalgia isn’t a reason to keep someone in your present.

🚧 “What if I run into them at Sainsbury’s?” → A polite “Lovely to see you!” with no follow-up is perfectly British.

🚧 “I don’t want to seem rude.” → Rude is expecting endless emotional labor without reciprocation.

The 5-Minute Boundary Bootcamp

Practice these scripts today:

To the chronic complainer: “That sounds tough. What’s your plan?”

To the guilt-tripper: “I’ll have to pass this time, but hope it goes well!”

To the energy thief: “I’ve only got 5 minutes—what’s most important?”

Real Talk: Loneliness vs. Drain

Yes, the UK has a loneliness epidemic. But loneliness with peace is better than company that exhausts you. Temporary solitude creates space for better connections.

Homework: Send one “Thinking of you!” message to someone who always leaves you energized.

Next Chapter Preview:“The 5-Minute Rebellion – How Small Daily ‘No’s’ Build an Unstoppable Life”

Want to read more scripts for workplace dynamics or family guilt-trips? Join our Happiness Hub : This works because it respects British social norms while teaching stealthy empowerment.

Chapter 3: The 5-Minute Rebellion – How Small Daily “No’s” Build an Unstoppable Life

“The average British adult says ‘yes’ to 14 unwanted requests per week. That’s 728 unnecessary obligations per year. How many of your dreams are buried under that pile?”

The British “Yes” Addiction

We’re a nation of people-pleasers. From agreeing to work late (“Mustn’t make a fuss”) to attending distant cousins’ baby showers (“It’s what you do”), we’ve been conditioned to treat our own time as the least valuable resource in the room.

But here’s the psychological truth: Every unnecessary “yes” is a silent “no” to your own priorities. This chapter is about reclaiming your autonomy—five minutes at a time.

Step 1: The Power of Micro-No’s

(What you’ll need: A notebook, red pen, and willingness to feel briefly uncomfortable)

Action: For the next 48 hours, document every time you:

Agree to something against your better judgment

Suppress a preference to avoid “rocking the boat”

Say “I don’t mind” when you absolutely do mind

Example: Tom, 34 from Cardiff, realized he’d spent £87/month on after-work drinks he didn’t enjoy, just to appear “part of the team.”

Invisible Obligations (Automatically covering for chronically late colleagues)

Self-Betrayal (Ordering what others are having to avoid “being difficult”)

Pro Tip: Highlight every compliance in your notebook with your red pen. The blood-like color isn’t accidental—it represents what these “yeses” cost you.

Step 2: The 5-Minute Rebellion Technique

Start small to avoid system shock:

Day 1-3:

Add a 5-minute pause before any agreement (“Let me check my diary”)

Replace one automatic “yes” with “I’d prefer not to” (Note the sky doesn’t fall)

Day 4-7:

Decline one non-essential request (The 11am meeting that could be an email)

State one genuine preference (“Actually, I’d rather go to the Indian restaurant”)

Case Study: NHS nurse Anika used this method to stop covering last-minute shifts—her colleagues adapted within two weeks.

Step 3: The UK-Specific Resistance Playbook

When pushback comes (and it will), have these socially acceptable deflectors ready:

For workplaces: “I’ve reviewed my priorities and can’t give that the attention it deserves.”

For family: “I’m trying something new this year—only committing to what truly lights me up.”

For friends: “I’m being more intentional with my time, so I’ll have to pass.”

The Ripple Effect

Within 21 days, you’ll notice: ✅ People start asking rather than assuming ✅ Your calendar develops white space ✅ Your “yes” becomes valuable rather than expected

Warning: Some relationships won’t survive this change. Those were transactions, not connections.

Real Talk: Why This Feels Revolutionary

In a culture where “not causing trouble” is the highest virtue, choosing yourself becomes a radical act. But consider:

The most respected people in your life are probably those with boundaries

Every historic British reform—from suffrage to workers’ rights—started with someone refusing to comply

Homework: Today, say no to:

One meaningless request

One assumed obligation

One self-betrayal

Track the results.

Next Chapter Preview:“Loneliness Hack: How 15 Seconds of Courage Can Rewire Your Social Brain”

Chapter 4: Loneliness Hack – How 15 Seconds of Courage Can Rewire Your Social Brain

“Loneliness isn’t about being alone—it’s about feeling unseen. And in Britain, we’ve perfected the art of being surrounded by people while remaining utterly invisible.”

The UK Connection Paradox

Office for National Statistics data reveals a haunting contradiction:

45% of UK adults report feeling lonely regularly

Yet 62% avoid casual social interactions daily

We queue silently, avert eyes on the Tube, and pretend we don’t notice the same faces at our local café. This chapter breaks that cycle with neuroscience-backed micro-actions.

Step 1: The 15-Second Rule

(What you’ll need: A timer, one deep breath, and willingness to break 400 years of British social conditioning)

The Science: Oxford researchers found that micro-connections (under 15 seconds) trigger the same dopamine release as longer interactions—with 90% less social anxiety.

Today’s Challenge:

Make eye contact + small smile with:

Your barista (“Thanks, have a good one!”)

A fellow dog walker (“Lovely morning!”)

The quiet colleague at the kettle (“Tea’s better today!”)

Notice: Their reaction (usually positive) and your own physiological response

Case Study: Retired teacher Margaret, 68, went from “invisible widow” to community hub by simply greeting her postman daily—which led to coffee invites from neighbors.

Step 2: The Vulnerability Ladder

British loneliness persists because we mistake acquaintances for connections. Upgrade relationships systematically:

Rung 1: Surface → Weather talk (“Wild wind today!”) Rung 2: Observation → Mild self-disclosure (“It ruined my walk—I need the exercise!”) Rung 3: Shared interest → (“You’re into hiking? Any local routes you’d recommend?”)

Pro Tip: Carry conversation sparkers—a book, unusual umbrella, or dog—that invite comments.

Step 3: The “Third Place” Strategy

Sociologists identify three spaces for wellbeing:

Home

Work

Third Place (Where you’re known but not obligated)

UK-Friendly Third Places:

Independent gyms (Not chains—community matters)

Craft workshops (London’s “Drink & Draw” events)

Park run clubs (Free + built-in camaraderie)

Avoid: Alcohol-centric spaces—pubs often deepen isolation.

The British Excuse-Busting Guide

🚧 “But I’m not interesting enough” → People remember how you made them feel, not your anecdotes.

🚧 “Strangers don’t want to talk” → 2024 Transport for London study showed 73% enjoyed casual Tube chats.

🚧 “It’s too late to make friends” → Manchester’s “Friendship Bench” scheme proves otherwise—retirees form 80% of new bonds.

The Rejection Inoculation Exercise

Fear holds you back? Try this:

Purposefully get rejected 3x this week (Ask for a bakery sample, a seat swap on train)

Discover: Nothing catastrophic happens

Bonus: You’ll collect surprising yeses

Real Data: 92% of “cold approaches” in UK settings get neutral/positive responses.

Real Talk: Why This Works

Our brains evolved to connect—British reserve is cultural, not biological. Each micro-interaction:

Lowers cortisol (stress hormone)

Raises oxytocin (bonding chemical)

Makes the next connection easier

Homework: Today, initiate three 15-second human moments with:

A service worker

A stranger in green space

Someone you “sort of know” but never speak to

Next Chapter Preview:“The Money-Life Balance – How to Align Spending With Joy (Beyond Avocado Toast Shaming)”

Chapter 5: The Money-Life Balance – How to Align Spending With Joy (Beyond Avocado Toast Shaming)

“The average Brit will waste £73,000 on ‘invisible expenses’ in their lifetime—not on luxuries or memories, but on things that leave no trace of happiness. Where’s yours going?”

The UK Spending Trap

We’re caught between two toxic narratives:

Austerity Mindset (“Must save every penny”) → Leads to deprivation burnout

This chapter introduces Value-Based Spending—a revolutionary approach where your bank statement becomes a happiness audit.

Step 1: The Financial X-Ray

(What you’ll need: Last 3 months of bank statements, highlighters, and a stiff drink)

The 3-Color System:

Green (Expenses that added lasting value)

Yellow (Necessities with no emotional return)

Red (Spending you can’t justify to your future self)

Shocking Truth: Most UK adults find 38% of spending falls in the red zone.

Case Study: Marketing exec Dev, 31, discovered he’d spent £2,200/year on “convenience coffees” during depressive slump walks—switched to park benches with thermos, saved money AND improved mood.

Step 2: The 48-Hour Rule

Combat impulse spending with this neurological hack:

See desired item

Take photo + note price

Set 48-hour timer

If still craving after deadline → Purchase guilt-free

UK-Specific Triggers to Watch:

“Just £3” apps (Summed up, these often exceed rent)

Supermarket “meal deal mentality” (The £3.50 daily trap)

🚧 “I deserve this treat” (after stressful day) → Creates neural link between distress and spending.

Fix: Build a “Stress First Aid Kit” with non-spending comforts (e.g., favorite playlist, emergency gym session).

The 5-Minute Wealth Hack

Today:

Cancel one unused subscription

Switch one bill to better deal

Move £5 to “Future Joy” pot

Psychological Payoff: These small wins build financial agency muscles.

Real Talk: Why This Changes Everything

Money is emotional currency. Every pound spent unconsciously is:

A vote for someone else’s priorities

A theft from your future freedom

Homework: For one purchase this week, ask: “Is this taking me toward the life I want, or keeping me comfortable in the life I have?”

Next Chapter Preview:“Digital Boundaries – How to Reclaim Your Attention From the Algorithmic Underworld”

Want explore specific UK personal finance hacks or regional/city/town cost-saving tips? Join our Happiness Hub today respects British money psychology while radically optimising for happiness.

Chapter 6: Digital Boundaries – How to Reclaim Your Attention From the Algorithmic Underworld

“The average UK adult spends 4 hours 8 minutes daily on their phone—that’s 63 full days per year. How many of those moments do you actually remember?”

The British Digital Dilemma

We pride ourselves on queueing patiently, yet we’ve become a nation of digital queue-jumpers—constantly interrupting real life for phantom notifications. A 2024 Ofcom report revealed:

71% check phones within 10 minutes of waking

1 in 3 would rather break a bone than their phone

This isn’t just distraction—it’s cognitive strip-mining. Your attention is the new oil, and Silicon Valley is fracking your mind.

Step 1: The Attention Audit

(What you’ll need: Your phone’s screen time report, a notebook, and the willingness to face uncomfortable truths)

The 3-Part Revelation:

Check Your Screen Time (Settings → Digital Wellbeing)

List Your Top 3 Time-Sink Apps

Ask: “What valuable life activity could replace these hours?”

Example: Teacher Sarah, 34, discovered she spent 11 hours/week scrolling Instagram—equivalent to learning Spanish fluently in 6 months.

Step 2: The Nuclear Option (British Moderation Edition)

For each problematic app, choose one detox strategy:

🔥 The Purge: Delete entirely (Best for TikTok/endless scroll) ⏰ The Time Lock: Use Focus Mode to block after daily limit 📱 The Space Demotion: Move to phone’s last screen + bury in folder

Pro Tip: Replace each deleted app with a real-world equivalent:

Swap Twitter for newspaper crossword

Replace YouTube rabbit holes with audiobook walks

Step 3: The Notification Inquisition

Every alert is a miniature courtroom where your attention stands trial. Ask each notification:

“Is this truly urgent?” (Most UK workers’ emails aren’t)

“Would I interrupt a friend for this?”

“Does this align with my priorities?”

Action: Right now—turn off all non-essential notifications. Keep only:

Real human calls

Calendar alerts

Emergency services

The UK-Specific Digital Traps

🚧 “But I need to be available for work!” → Data shows 67% of after-hours emails could wait until morning.

Fix: Set an OOO auto-reply after 6pm: “Messages received after 6pm will be addressed next business day.”

🚧 “What if I miss something important?” → Important things find you. The Queen’s death didn’t break via push notification.

🚧 “Scrolling helps me relax” → Studies prove phone use spikes cortisol (stress hormone) by 28%.

Better Alternative: Try NSDR (Non-Sleep Deep Rest)—10-minute guided breathing exercises.

The 5-Minute Digital Declutter

Right Now:

Delete 10 unused apps

Unsubscribe from 5 newsletters

Put phone in grayscale (Settings → Accessibility) to reduce dopamine hits

Why Grayscale Works: Without colorful icons, your brain loses interest 43% faster.

Real Talk: Why This Feels Impossible

Your brain has been rewired to crave digital hits. Withdrawal symptoms include:

Phantom vibration syndrome

“Boredom” that’s actually withdrawal

Initial productivity DIP as brain recalibrates

Stay Strong: After 72 hours, most report: ✅ Better concentration ✅ Deeper conversations ✅ Rediscovery of forgotten hobbies

Homework: The Analog Weekend Challenge

This Saturday:

Charge phone in another room overnight

Use physical maps if going out

Carry a notebook for ideas/reminders

Bonus: Take one “proof photo” of your analog day—then don’t post it.

Next Chapter Preview:“The Body-First Rule – Why Sleep Isn’t a Luxury But Your Secret Productivity Weapon”

Chapter 7: The Body-First Rule – Why Sleep Isn’t a Luxury But Your Secret Productivity Weapon

“Britain runs on a toxic trifecta: caffeine, cortisol, and stubbornness. We wear exhaustion like a badge of honor—while our health, happiness, and productivity crumble. What if the ultimate rebellion was actually… rest?”

The Great British Sleep Crisis

NHS data shows 1 in 3 UK adults survive on <6 hours sleep nightly

67% of workers report making errors due to fatigue

Yet 82% believe “pushing through” is necessary for success

This isn’t dedication—it’s biological sabotage. Your body isn’t a machine. It’s an ecosystem.

Step 1: The Sleep Autopsy

(What you’ll need: 1 week, a sleep tracker (even basic smartphone apps work), and raw honesty)

Track These 5 Factors:

Actual sleep duration (Not time in bed)

Pre-bed activities (Scrolling? Wine? Work emails?)

Wake-up mood (Refreshed? Foggy?)

Energy crashes (2pm zombie mode?)

Dream recall (Vivid dreams = good REM cycle indicator)

Case Study: Architect Liam, 42, discovered his “nightcap” whisky was destroying his deep sleep—cutting alcohol added 90 minutes of quality rest without changing bedtime.

Step 2: The Non-Negotiable 3

These foundations trump all other biohacks:

Sleep Sanctuary

Cold room (18°C ideal)

Pitch black (Use an eye mask if needed)

Phone in another room (Or locked in a timed kitchen safe)

Caffeine Curfew

No coffee after 2pm (Half-life is 5-6 hours)

Switch to roasted barley tea or decaf after noon

Light Leverage

Morning sunlight within 30 mins of waking (10 mins on cloudy days)

Amber lights after 9pm (Install F.lux or use smart bulbs)

British Reality Check: That “quick scroll” in bed costs you 37 minutes of sleep on average—not from the time spent, but from disrupted sleep architecture.

Step 3: The Energy Audit

Most productivity advice fails because it ignores biology. Schedule tasks by your natural energy tides:

🦁 Lion Phase (Morning Peak)

Deep work

Important decisions

Creative tasks

🐻 Bear Phase (Midday Dip)

Meetings

Admin

Social interactions

🐺 Wolf Phase (Evening Recovery)

Planning

Light reading

Gentle movement

Pro Tip: The average Brit’s most productive window is 9:30-11:45am—stop wasting it on emails.

The British Excuse-Busting Guide

🚧 “I’m just not a morning person” → 89% of “night owls” can reset their chronotype in 21 days with consistent light exposure.

🚧 “I don’t have time for 8 hours” → 6 hours of quality sleep beats 8 hours of disrupted rest. Focus on sleep efficiency first.

🚧 “I sleep better after a drink” → Alcohol fragments sleep architecture—you’re unconscious, not rested.

The 5-Minute Energy Rescue

When exhaustion hits:

Hydrate (Dehydration mimics fatigue)

Breathe (4-7-8 technique: Inhale 4s, hold 7s, exhale 8s)

Move (5-minute walk resets focus better than caffeine)

Emergency Option: 10-minute NSDR (YouTube “non-sleep deep rest”)

Real Talk: Why This Feels Revolutionary

We’ve been conditioned to believe exhaustion equals importance. But consider:

Every great British invention—from the steam engine to the World Wide Web—came from rested minds

Churchill napped daily during WWII

The 4-day work week trial showed 88% productivity maintenance with better-rested staff

Homework: This week—

Protect your peak 2 hours for important work

Take one 20-minute nap (Set alarm—over-sleeping causes grogginess)

Eat lunch away from screens (Digestion impacts afternoon energy)

Next Chapter Preview: Future-Self Journaling – How Letters From Your Best Life Can Rewire Your Present Choices

Chapter 8: Future-Self Journaling – How Letters From Your Best Life Can Rewire Your Present Choices

“Most people in the UK live with a vague sense that ‘someday’ they’ll get around to being happy. But your future self isn’t some stranger who’ll magically appear—they’re being built by the decisions you make today.”

The British Procrastination Epidemic

A Cambridge University study revealed:

68% of Brits have “dreams they’ll pursue eventually”

Only 9% take consistent action

The average person spends 218 hours/year imagining a better life without taking the first step

This chapter introduces Future-Self Journaling—a neuroscience-backed method to collapse the gap between aspiration and reality.

Step 1: The Time Capsule Technique

(What you’ll need: A dedicated notebook, pen, and willingness to confront your own potential)

The Exercise:

Date the entry 5 years in the future

Write a letter from your best possible self describing:

Daily routines

Career achievements

Relationships

Health habits

Personal growth

Include specific sensory details (smells, sounds, emotions)

Example: Receptionist Tanya, 29, wrote about her future self running a dog-walking business—within 18 months she’d left her job and secured 12 regular clients.

Science Behind It: UCLA research shows this practice increases goal-directed behavior by 31% by activating the brain’s reticular activating system (your psychological GPS).

Step 2: The Reverse Engineering Blueprint

Now analyze your future-self’s letter for:

Daily Habits (What routines got them there?)

Avoided Pitfalls (What did they stop doing?)

Key Decisions (What bold choices created the change?)

Pro Tip: Highlight recurring themes—these are your North Star indicators.

Step 3: The 1% Action Protocol

Each week:

Re-read your future letter (Best done Monday mornings)

Choose one micro-action that aligns with that vision

Journal obstacles honestly (No British stiff-upper-lip lies)

Case Study: Retired engineer Graham, 63, used this method to transition from “waiting to die” to volunteering with Thames River conservation—his future-self letter mentioned “fresh air and purpose” repeatedly.

The UK-Specific Mindset Traps

🚧 “It’s too late for me” → The average age for starting a business in the UK is 47

🚧 “I don’t deserve that life” → British class conditioning often makes ambition feel “unseemly”

🚧 “Things will work out somehow” → Passive hope is the enemy of transformation

The 5-Minute Future Hack

Right Now:

Set a timer for 5 minutes

Write one paragraph from your 6-month future self

Identify one action you can take today toward it

Example: “It’s November 2024. I finally prioritized sleep and wow—my morning energy makes work feel effortless. I start each day with 10 minutes of stretching instead of panic-scrolling…” → Today’s action: Charge phone outside bedroom tonight

Real Talk: Why This Works When Vision Boards Fail

Traditional goal-setting often misses:

Emotional stakes (Your letter makes the future feel real)

Identity shift (You practice “being” that person now)

British practicality (Concrete details bypass vague dreaming)

Homework: This week—

Write one full future-self letter

Share one insight with a trusted friend

Display one sentence where you’ll see it daily

Next Chapter Preview:“The Support Gap Fix – How to Build Your Personal Board of Directors (Because Going It Alone Is Nonsense)”

Chapter 9: The Support Gap Fix – How to Build Your Personal Board of Directors

“Britain has a stiff-upper-lip epidemic. We’d rather struggle alone for years than admit we need help. But here’s the truth: no one ever changed their life in isolation.”

The UK Support Paradox

76% of British adults believe asking for help is a sign of weakness (YouGov)

Yet 83% say having a mentor was crucial to their success (LinkedIn Data)

The average person has 14x more casual acquaintances than true advisors

This chapter isn’t about networking. It’s about strategically assembling your brain trust—the people who’ll challenge, champion, and course-correct you.

Step 1: The 5-Role Framework

Your life needs these key players (few people have all five):

The Mentor

Has walked your desired path

Example: Former manager who’s now consulting

The Pragmatist

Grounds your ideas in reality

Example: Accountant friend who spots financial flaws

The Connector

Knows everyone you need to know

Example: That one friend who “collects interesting people”

The Cheerleader

Believes in you more than you do

Example: Childhood friend who remembers your potential

The Antagonist

Challenges your assumptions (constructively)

Example: Book club member who debates your views

British Reality Check: Most people’s “support network” is just drinking buddies who nod along.

Step 2: The Strategic Outreach Method

How to recruit without feeling awkward:

For Mentors: “I’m working on [goal] and admire how you’ve handled [specific challenge]. Would you be open to a 20-minute coffee chat about lessons learned?”

For Pragmatists: “I respect your [expertise]—could I run an idea by you for brutal feedback?”

For Connectors: “I’m looking to meet people in [field]—anyone in your network come to mind?”

Pro Tip: Always offer value first—share an article or make an introduction for them.

Step 3: The Quarterly Review

Maintain your board effectively:

Map current advisors (Who fills which role?)

Identify gaps (Missing an antagonist?)

Prune inactive members (Some relationships expire)

Add strategically (Target 1 new member per quarter)

Case Study: Marketing director Priya, 38, realized she only had cheerleaders. She joined a founder’s mastermind group to add pragmatists—within months, revenue grew 25%.

The British Hang-Ups (And How to Overcome Them)

British Happiness Paradoxes

🚧 “I don’t want to bother people” → Most professionals enjoy sharing expertise (It’s flattering)

🚧 “Asking feels transactional” → Frame it as mutual growth: “I’d love to hear your perspective—maybe I can offer fresh eyes on your challenges too?”

🚧 “What if they say no?” → The worst outcome is the same as not asking

The 5-Minute Board Starter

Today:

Text one potential advisor with a specific, low-commitment ask

Join one UK-based professional group on Meetup.com

Identify which role you’re missing

Example Message: “Hi [Name], I’m working on improving [skill] and remember you’re great at this. Any chance you’d share one lesson over coffee next week? My treat.”

Real Talk: Why This Changes Everything

Your environment shapes your success more than your willpower. With the right board: ✅ Opportunities find you ✅ Blind spots get caught early ✅ Imposter syndrome fades

Homework: This week—

Make one ask (Start small)

Analyze your current circle (Who’s lifting vs. limiting you?)

Attend one skill-share event (Try WorkInStartups.com for UK tech)

Next Chapter Preview:“The Comfort Zone Calendar – Why Discomfort Is the Only Valid Growth Metric”

Want to discover templates for following up or handling rejection? Remember: The people who succeed fastest are those who realise early that “going it alone” is just pride in disguise. Join our Happiness Hub and Happiness Pod.

Chapter 10: The Comfort Zone Calendar – Why Discomfort Is the Only Valid Growth Metric

“The British comfort zone isn’t just a place—it’s a national heritage site. We queue for it, preserve it, and defend it against all invaders. But here’s the uncomfortable truth: your best life exists exactly one step beyond where you currently feel safe.”

The UK Growth Paradox

89% of Brits admit avoiding uncomfortable situations (University of Warwick Study)

Yet 92% say their biggest regrets involve “not taking the chance”

The average person spends 7 years in jobs they’ve outgrown due to inertia

This chapter introduces the Discomfort Dividend—the measurable ROI you get from strategic unease.

Step 1: The Comfort Audit

(What you’ll need: Last month’s calendar, three highlighters, and radical honesty)

Color-Code Your Month:

Green (Routine/Effortless)

Yellow (Mildly Challenging)

Red (Made you sweat)

The Reality Check: Most UK adults’ calendars are 90% green—a recipe for slow stagnation.

Case Study: NHS nurse Anika, 29, realized she hadn’t done anything that scared her since her 2020 interview. Started saying yes to public speaking—within 6 months, became a union rep.

Terror (Avoidance behavior – e.g., salary negotiation)

British-Specific Growth Opportunities:

Returning items (Our retail awkwardness costs £2.3bn/year in unused goods)

Asking for help (See Chapter 9)

Being the first to dance at weddings

Step 3: The Strategic Discomfort Planner

Build your growth intentionally:

Weekly:

1 x Level 1 challenge (Daily)

1 x Level 2 challenge (Twice weekly)

1 x Level 3 challenge (Monthly)

Progression Examples: Week 1: Compliment a stranger → Week 4: Pitch an idea at work Month 1: Attend meetup alone → Month 3: Speak at meetup

Pro Tip: Schedule challenges like medical appointments—non-negotiable.

The British Resistance Toolkit

🚧 “I’ll do it when I feel ready” → Readiness is a myth. Confidence comes after action.

🚧 “What if I look stupid?” → People remember their own faux pas, not yours.

🚧 “It’s not the British way” → Neither was Brexit, but we managed that discomfort.

The 5-Minute Discomfort Injection

Today:

Do one thing you’ve been avoiding (That email, phone call, conversation)

Take the “awkward” seat in a meeting

Wear something slightly bolder than usual

Neurological Payoff: Each act shrinks your fear response for next time.

Real Talk: Why This Works

Discomfort is the only reliable growth metric because: ✅ Your brain can’t argue with lived experience ✅ Compound growth applies to courage too ✅ You rewrite your identity from “someone who can’t” to “someone who does”

Homework:

Book one terrifying thing for next month (Course? Solo trip?)

Create a “Brave List” of past wins (Re-read when doubting yourself)

Find a discomfort buddy (Accountability halves the fear)

Next Chapter Preview:“The Comparison Detox – How to Stop Measuring Your Life Against Filtered Highlights”

Want to discover industry-specific discomfort challenges or a deeper dive into the neuroscience? Remember: The magic you want is in the discomfort you avoid. Join our Happiness Hub and Happiness Pod.

Chapter 11: The Comparison Detox – How to Stop Measuring Your Life Against Filtered Highlights

“Britain has become a nation of secret spectators—we scroll through polished highlight reels while quietly tallying our own perceived shortcomings. But here’s the liberating truth: comparison isn’t just the thief of joy, it’s the architect of your stagnation.”

The UK Comparison Epidemic

78% of Brits admit to “compare and despair” social media habits (Ofcom)

The average person makes 17 unconscious daily comparisons (Cambridge Psychology)

62% have delayed life milestones (buying homes, changing careers) due to perceived “falling behind”

This chapter is your intervention. We’re going digital cold turkey—not by deleting apps, but by rewiring your comparison operating system.

Step 1: The Comparison Autopsy

(What you’ll need: 3 days of screen time tracking, a notebook, and forensic curiosity)

Track These 5 Comparison Triggers:

Platforms (Instagram? LinkedIn? Rightmove?)

People (Whose posts make your stomach tighten?)

Life Categories (Career? Relationships? Home decor?)

Case Study: Teacher James, 31, realized property porn left him feeling “behind”—unfollowed all estate agents, saved £8,000 in a year by avoiding aspirational spending.

Step 2: The Reality Remix Framework

For every comparison thought, apply this filter:

The Backstage Pass

“What aren’t they showing?” (Debt? Stress? Help they have?)

The Timeline Trick

“Where was I X years ago?” (Progress hides in decade views)

The Currency Conversion

“Would I truly want their whole life?” (Or just this highlight?)

British-Specific Comparison Traps:

School reunion syndrome (That one peer who “made it”)

“London or bust” mentality (Ignoring regional quality of life)

Invisible privilege blind spots

Step 3: The Strategic Comparison Diet

Not all comparisons are equal—curate your inputs:

🚫 Eliminate:

“Inspiration” accounts that actually deflate

Gossip/news sources trading in lack

Toxic benchmarking (e.g., comparing your Chapter 1 to someone’s Chapter 20)

✅ Introduce:

“Behind the scenes” follows (Search #nofilter)

Time-lapse progress accounts

Local community groups (Real people, real struggles)

Pro Tip: Create a “Gratitude Following” list—accounts that leave you energized, not drained.

The British Mindset Hacks

🚧 “But they really HAVE it better” → Studies show people overestimate others’ happiness by 40%

🚧 “I’m objectively behind on milestones” → The average first-time buyer is now 34 (up from 29 in 2000)

Turn off LinkedIn “work anniversaries” notifications

Bookmark one “real life” account (Try @instagramreality)

Cognitive Payoff: Each act reclaims mental bandwidth for YOUR path.

Real Talk: Why This Matters

Comparison doesn’t just hurt feelings—it alters decisions. When you stop measuring against distorted mirrors: ✅ You make choices aligned with YOUR values ✅ Creativity flourishes in absence of competition ✅ You notice existing blessings (currently obscured by “shoulds”)

Homework:

Conduct a social media SPRING CLEAN (15 minutes)

Write your personal success metrics (What actually matters to YOU?)

Try a “comparation” week (Track only against your past self)

Next Chapter Preview:“The Accountability Pact – Why Going It Alone Is the Fastest Path to Nowhere”

Want industry-specific comparison detox strategies or a deeper dive into UK class comparison dynamics? Remember: The life you’re envying is someone else’s highlight reel—your blooper reel is comparing against it. Join our Happiness Hub and Happiness Pod.

Chapter 12: The Accountability Pact – Why Going It Alone Is the Fastest Path to Nowhere

“Britain has a proud tradition of silent suffering—we grind through challenges alone, wearing exhaustion as a badge of honor. But here’s the inconvenient truth: every major study on achievement shows that accountability partners triple your success rates. Your stubborn independence is costing you results.”

The UK Accountability Deficit

81% of New Year’s resolutions fail by February (UK Government Data)

Yet those with accountability partners are 3.2x more likely to succeed (American Society of Training and Development)

The average British worker wastes 147 hours/year repeating preventable mistakes due to lack of feedback

This chapter isn’t about finding a cheerleader. It’s about engineering unavoidable accountability that forces growth.

Step 1: The Accountability Audit

(What you’ll need: A list of last year’s unfinished goals, and the courage to face why they stalled)

Ask For Each Failure:

“Who knew I was working on this?” (Usually: no one)

“What regular check-ins existed?” (Usually: none)

“What were the consequences of quitting?” (Usually: nothing)

Case Study: Entrepreneur Dev, 28, kept “ghosting” on his side hustle—until he prepaid a mastermind group £500 he’d lose if he skipped check-ins. Revenue grew 4x in 6 months.

Step 2: The 3-Level Accountability Framework

Not all accountability is equal—build layers:

Level 1: The Peer Pact

Weekly WhatsApp check-ins with a goal buddy

Swap: “How’s it going?” → “Did you do what you promised?”

Level 2: The Professional Pact

Hire a coach/trainer (Even 1 session creates obligation)

Join a paid accountability group (Money raises stakes)

Level 3: The Public Pact

Announce goals on social media

Start a progress blog/newsletter

British-Specific Options:

Parkrun pledges (Public fitness goals)

Union learning reps (Free workplace accountability)

Library study groups (Silent but powerful peer pressure)

Step 3: The Consequences Contract

The magic is in the stakes. With your accountability partner:

Define measurable targets (Not “exercise more” but “3 gym visits/week”)

Set check-in frequency (Weekly works best for habits)

Create meaningful consequences

Financial (Prepay and lose it if you fail)

Social (Donate to a cause you hate if you quit)

Practical (Hand over your Xbox until goal met)

Pro Tip: The best consequences are immediate, inevitable, and painful enough to matter.

The British Resistance Breakers

Your Fine Is Someone’s Lifeline

🚧 “I don’t want to bother people” → Frame it as mutual: “We’ll both benefit from staying on track”

🚧 “What if I fail publicly?” → Better to fail quickly and adjust than fail slowly in private

🚧 “I should be able to do this alone” → Even Olympic athletes have coaches—your goals deserve equal support

The 5-Minute Accountability Starter

Today:

Text one potential accountability partner with a specific proposal

Book one paid commitment (Class, coaching, challenge)

Set one “if-then” consequence (e.g., “If I skip gym, I clean flat top-to-bottom”)

Example Message: “Hey [Name], I’m working on [goal] and think we could both benefit from weekly check-ins. Fancy 10-minute calls every Monday to report progress?”

Real Talk: Why This Works

Accountability works because it: ✅ Turns vague intentions into concrete commitments ✅ Leverages our deep-seated fear of social disapproval ✅ Provides course-correction before small failures become big ones

Homework:

Establish one accountability layer this week

Analyze past failures for missing accountability

Try the “precommitment” trick (Book non-refundable sessions in advance)

Next Chapter Preview:“The Happiness Dashboard – How to Measure What Actually Matters”

Want workplace-specific accountability systems or templates for consequence contracts? Remember: The difference between dreams and results is often just one committed witness. Join our Happiness Hub and Happiness Pod.

Chapter 13: The Happiness Dashboard – How to Measure What Actually Matters

“Britain measures success in all the wrong currencies—salary bands, property values, and job titles. Meanwhile, 72% of UK professionals can’t recall the last time they felt truly fulfilled. What if you tracked happiness with the same precision as your bank balance?”

The Metric Mismatch Crisis

68% of Brits measure life progress by societal benchmarks (YouGov)

Only 11% have a personal happiness tracking system

The average person checks financial apps 9x/week but never assesses emotional wealth

This chapter introduces Quantified Wellbeing—a radical approach to measuring what actually moves the needle on life satisfaction.

Step 1: The Core Metrics Audit

(What you’ll need: Last month’s calendar, bank statements, and a 1-10 rating system)

Rate These 5 Hidden Happiness Indicators:

Autonomy (% of decisions made freely vs. obligation)

Connection (Meaningful interactions/week)

Growth (New skills/challenges undertaken)

Contribution (Times you helped others meaningfully)

Vitality (Energy levels upon waking)

Case Study: Accountant Ravi, 35, discovered his “perfect life” scored 2/10 on autonomy—prompted him to negotiate remote work Wednesdays, boosting happiness more than his last raise.

Step 2: The Personal KPI Dashboard

Ditch generic metrics. Track what matters to you:

For Career:

Learning opportunities/month > Salary

Colleague trust levels > Hours worked

For Relationships:

Depth of conversations > Number of friends

Shared experiences/month > Social media likes

For Health:

Morning mobility > Gym frequency

Sleep quality scores > Step count

British Reality Check: We obsess over house prices while neglecting “home atmosphere” scores.

Step 3: The Weekly Wellbeing Review

15 Minutes Every Sunday:

Celebrate 3 “Wins” (However small)

Note 1 “Leak” (Energy drain to address)

Set 1 “Experiment” (Try one new wellbeing tactic)

Pro Tip: Use color coding—red/amber/green works better than numbers for quick insights.

The British Measurement Traps

🚧 “If it’s not quantifiable, it doesn’t count” → The most important things (love, purpose) resist easy metrics

🚧 “Happiness is too fluffy to measure” → NHS now uses WEMWBS (Warwick-Edinburgh Mental Wellbeing Scales)

🚧 “I’ll feel it when I get there” → Without tracking, you’ll move goalposts indefinitely

The 5-Minute Dashboard Starter

Today:

Identify one unconventional metric that matters to you

Create a simple tracking system (Notes app table works)

Schedule first weekly review in calendar

Example: Teacher Sarah tracks “student lightbulb moments” instead of marking speed.

Real Talk: Why This Changes Everything

When you measure differently: ✅ You spot hidden happiness leaks (e.g., that “prestigious” draining committee role) ✅ Progress becomes visible (Prevents “is this all there is?” syndrome) ✅ You make better decisions (Choices align with actual fulfillment)

Homework:

Run one life category audit this week

Create three personal KPIs

Share one insight with a friend

Next Chapter Preview:“The Life Edit – How to Ruthlessly Prioritize What Actually Matters”

Want sector-specific wellbeing metrics or a deeper dive into NHS measurement tools? Remember: We don’t drift toward happiness—we navigate there with proper instruments. Join our Happiness Hub and Happiness Pod.

Chapter 14: The Life Edit – How to Ruthlessly Prioritize What Actually Matters

“The average British adult spends 218 minutes daily on autopilot activities that add zero value to their lives. That’s 55 full days a year wasted on the mundane while dreams collect dust. It’s time for a Marie Kondo approach to your entire existence.”

The UK Clutter Crisis (Beyond Physical Stuff)

79% of Brits feel overwhelmed by commitments they don’t value (Mental Health UK)

The typical professional has 37 recurring obligations (meetings, memberships, traditions)

62% say they’ve postponed important life goals for “when things calm down” (Spoiler: They won’t)

This chapter is your surgical toolkit for cutting the trivial many to focus on the vital few.

Step 1: The Brutal Triage

(What you’ll need: 1 week’s time tracking, Post-its, and an unforgiving mindset)

The 3-Bucket System: 🔥 Keepers (Aligns with core values, provides joy/meaning) 💀 Tolerators (Doesn’t fulfill but feels obligatory) 🗑 Drains (Adds negativity with zero upside)

Case Study: Lawyer Imran, 41, discovered 60% of his “urgent” work emails were CCs he ignored anyway—created filter rules saving 11 hours weekly.

Step 2: The British Excise Strategy

How to eliminate without causing offense:

For Work:

The “Alternative Proposal”: “Instead of this weekly meeting, could we try [more efficient solution]?”

The “Sunset Clause”: “Let’s trial pausing this for 3 months and assess impact”

For Social:

The “Gradual Fade”: Reduce attendance frequency by 50%

The “Upgrade Swap”: Replace dull obligations with meaningful activities (“Instead of drinks, let’s volunteer together”)

For Personal:

The “20-Minute Test”: If it wouldn’t matter in 20 years, don’t spend 20 hours on it

The “Hell Yeah!” Rule: Only say yes to what sparks genuine enthusiasm

Step 3: The Protected Priority Framework

Guard what matters with military precision:

Identify 3 Life Pillars (e.g., Family health, Creative expression, Community impact)

Allocate Time/Resources First (Schedule these before anything else)

Create Buffer Zones (30% empty space for spontaneity/serendipity)

Pro Tip: Treat your calendar like a London flat—prime space goes to priority “tenants.”

The British Roadblocks (And Counter-Tactics)

🚧 “But we’ve always done it this way” → Tradition is just peer pressure from dead people

🚧 “What will people think?” → Those judging your boundaries were benefiting from your lack of them

🚧 “I should be able to handle it all” → Modern life demands 300% more decisions than 50 years ago—your brain hasn’t evolved to cope

The 5-Minute Life Edit Starter

Today:

Cancel one recurring commitment that drains you

Block one sacred weekly priority slot in your calendar

Write your “Not Doing” list (What you’re consciously abandoning)

Example:“Not attending family gatherings where I feel judged”

Real Talk: Why This Feels Revolutionary

Editing your life: ✅ Creates space for unexpected opportunities ✅ Reduces decision fatigue by eliminating trivial choices ✅ Forces clarity about what truly matters to YOU (not your boss/community/social media)

Homework:

Conduct one area audit (Work calendar? Social commitments?)

Practice one elegant “no” this week

Protect one priority like it’s your firstborn

Next Chapter Preview:“The Resilience Upgrade – How to Bounce Forward (Not Just Back)”

Want industry-specific editing strategies or scripts for difficult conversations? Remember: Every “yes” to the non-essential is a “no” to your extraordinary life. Join our Happiness Hub and Happiness Pod.

Chapter 15: The Resilience Upgrade – How to Bounce Forward (Not Just Back)

“British resilience has long meant teeth-gritted endurance—weathering storms without complaint. But surviving isn’t thriving. The latest neuroscience shows true resilience isn’t about returning to baseline after hardship—it’s about using challenges as propulsion.”

The UK Resilience Gap

76% of Brits believe resilience means “carrying on as normal” (Mental Health Foundation)

Only 14% actively use adversity for growth

The average person spends 4.7 years in “recovery mode” after major setbacks

This chapter introduces Post-Traumatic Growth techniques—how to transform life’s body blows into breakthroughs.

Step 1: The Adversity Autopsy

(What you’ll need: A list of past challenges, colored pens, and radical honesty)

The 3-Part Analysis:

The Hit (What actually happened—strip away the story)

The Harm (Tangible impacts—lost money, relationships, confidence)

The Hidden Gifts (Skills, insights, or redirections gained)

Case Study: After redundancy, marketing exec Tasha, 39, discovered her “safe” corporate job had been stifling her creativity—now runs a successful indie PR firm.

Step 2: The Forward-Focus Framework

Rebuilding isn’t enough—aim higher:

1. The Perspective Hack

Ask: “How could this benefit me in 5 years?”

Example: Illness → Health expertise → Career pivot to wellness coaching