12 Proven Ways to Improve Your Lifestyle in the UK Without Breaking the Bank

Most people talk about “improving their lifestyle” as if it’s some distant, expensive dream.

The truth? You don’t need a lottery win — you need insider knowledge, smart choices, and the guts to stop doing what everyone else is doing.

Here are 12 real, proven ways to improve your lifestyle in the UK without emptying your bank account — and yes, we use all of them inside the CheeringUp.info Lifestyle Improvement Club.

1. Stop Paying Retail for Everyday Essentials

If you’re still buying from the first shop you walk into, you’re basically giving away money. The best prices are hidden — and no, they’re not on the first page of Google.

You don’t need a five-star price tag to get a five-star experience. From slow travel hacks to off-season luxury stays, you can live better for less if you know where to look.

From broadband contracts to gym memberships, UK companies overcharge people who don’t ask for a better deal. Club members share step-by-step scripts that slash bills instantly.

6. Turn Weekends Into Mini-Adventures

You don’t need two weeks off to feel alive again. A single weekend can feel like a holiday with the right location, plan, and budget tricks — which we give you.

7. Invest in Experiences, Not Clutter

New possessions rarely improve your life. New experiences nearly always do.

We connect members with affordable, unforgettable experiences across the UK.

8. Connect With People Who Actually Inspire You

If your social circle never challenges you, your lifestyle will never grow.

Inside the club, you meet UK movers and shakers who think bigger — and help you do the same.

9. Upgrade Your Health Without Expensive Fads

Forget overpriced supplements and fad diets. Our wellness tips are practical, science-based, and budget-friendly — because your health is your real wealth.

10. Master the Art of Last-Minute Deals

Hotels, cruises, flights — the closer the departure date, the cheaper it can get. But you need fast alerts and trusted sources. We send them directly to members.

11. Stop Believing “That’s Just How It Is”

Most people accept high prices, bad deals, and mediocre lifestyles because they think it’s normal.

It’s not. You just haven’t been shown the alternatives yet.

12. Join the CheeringUp.info Lifestyle Improvement Club

Discover 9 powerful ways to use baking soda (sodium bicarbonate) for your health. From heartburn relief to skincare, unlock the full potential of this natural remedy.

Baking soda (sodium bicarbonate or bicarbonate of soda) is a naturally alkaline compound with mild antiseptic and anti-inflammatory properties. While it’s mostly known for cooking and cleaning, it also has several potential health benefits when used properly and in moderation.

⚠️ Important Note Before Use

Baking soda can interact with medications and may not be safe for everyone, especially those with high blood pressure, kidney disease, or heart issues due to its sodium content. Always consult a healthcare professional before using it as a remedy.

🟩 Why Baking Soda Might Be Good for You

Balances pH in the body – Baking soda’s alkalinity may help neutralize excess acid in the body, particularly in conditions like acid reflux or mild acidosis.

Soothes digestive discomfort – Acts as an antacid to relieve heartburn and indigestion.

Promotes oral health – Natural teeth whitener and mouth cleanser.

Supports skin care – Helps with itching, irritation, and acne.

Muscle recovery – Athletes sometimes use it to reduce lactic acid build-up.

May help with urinary tract infections – Alters urine pH to create a less favorable environment for bacteria.

Natural deodorizer – Helps control body odor by neutralizing acids.

May support kidney function (in some cases) – Used under supervision for certain chronic kidney conditions.

Anti-inflammatory properties – Topical use may calm inflamed areas.

✅ 9 Ways to Use Baking Soda for Potential Health Benefits

1. Drink for Heartburn and Indigestion

How: Mix ½ tsp of baking soda in a glass of water (4–8 oz).

Why: Quickly neutralizes stomach acid.

Limit: No more than once every 4 hours; max 7 doses in 24 hours.

2. Mouth Rinse for Oral Health

How: Dissolve 1 tsp in half a glass of warm water and swish for 30 seconds.

Why: Fights bad breath, neutralizes acids, and soothes mouth ulcers.

3. Toothpaste for Teeth Whitening

How: Mix baking soda with water to make a paste and brush teeth gently.

Why: Helps remove surface stains and reduce plaque.

4. Soothing Bath for Itchy or Irritated Skin

How: Add ½ cup of baking soda to a warm bath and soak for 15–20 minutes.

Why: Calms eczema, psoriasis, or insect bites.

5. Foot Soak for Athlete’s Foot or Odour

How: Dissolve 3 tbsp in a basin of warm water and soak feet for 15 minutes.

Why: Neutralizes foot odor and may help combat fungal infections.

6. Baking Soda Paste for Insect Bites or Rashes

How: Mix 3 parts baking soda with 1 part water to make a paste and apply topically.

Why: Reduces itching and swelling from bites or minor skin irritations.

7. Natural Deodorant

How: Apply a pinch under each arm or mix with coconut oil and cornstarch.

Why: Neutralizes underarm odor by killing bacteria and reducing acidity.

8. Post-Workout Recovery Drink (with caution)

How: Some athletes drink a diluted mix (under supervision) to reduce lactic acid.

Why: May delay fatigue and enhance endurance.

⚠️ Caution: Can cause nausea or GI upset; consult a professional.

9. Alkaline Urine Support (for UTIs – under guidance)

How: ½ tsp in a glass of water once or twice a day.

Why: May reduce burning sensation in urine by raising pH.

⚠️ Important: Only temporary use; not a substitute for antibiotics.

🔚 Final Thought

While baking soda offers a range of potential health uses, moderation and proper medical guidance are essential. It’s not a cure-all, but when used wisely, it can be a useful home remedy with real benefits. Would you like a printable version or infographic summarizing these suggestions?

Disclaimer: The content provided in this post is for informational and educational purposes only. It is not intended as medical advice, diagnosis, or treatment. Always consult with a qualified healthcare professional before starting any new health or wellness routine, especially if you have existing medical conditions or are taking prescription medications.While baking soda (sodium bicarbonate) is commonly used in home remedies, its use should be approached with caution and awareness of potential risks. Results may vary from person to person.CheeringUpInfo does not accept any responsibility for actions taken based on the information provided. Use of this content is at your own discretion and risk.

Possible reasons you don’t know more about potential benefits

The potential benefits of baking soda (sodium bicarbonate) as a low-cost health remedy may be underemphasised or suppressed due to economic, regulatory, and market power dynamics, particularly in the UK. Here are some key reasons why:

💊 1. Baking Soda Is Too Cheap to Patent or Profit From

Pharmaceutical companies operate in a profit-driven model. Baking soda is:

Inexpensive

Widely available

Non-patentable

Because it’s a common household product, companies can’t secure exclusivity or charge high prices like they can for new drugs. There’s no financial incentive to fund clinical trials or promote it as a treatment when it doesn’t offer high margins.

🏢 2. Market Power Lies with a Few Global Conglomerates

In both the pharmaceutical and food sectors, a handful of powerful corporations dominate:

In the UK, supermarket shelves and pharmacy chains are heavily influenced by a small group of global players.

These companies often control access to health messaging, shelf space, and consumer trust.

As a result, natural or generic alternatives like baking soda are often pushed to the margins, while branded, high-profit products dominate public attention.

💷 3. Low ROI Means Low Research Investment

Baking soda may have genuine health benefits — from neutralising stomach acid to treating skin conditions — but there’s little motivation to conduct large-scale clinical trials because:

The cost of clinical trials is enormous

The return on investment is minimal

So it remains in the category of “folk remedy” or alternative health, rather than being promoted as a frontline treatment.

🛑 4. Regulatory Gatekeeping and Industry Lobbying

The pharmaceutical and processed food industries have a powerful influence on public health regulations and healthcare messaging in the UK:

Lobbying efforts often steer attention toward products that align with industry interests.

Natural remedies like baking soda are rarely included in NHS-backed campaigns or GP recommendations — not necessarily because they’re ineffective, but because no one profits from them.

🍽️ 5.Food Industry Wants You Dependent on Processed Solutions

The dominant food industry:

Baking soda is an alkaline compound that can help balance pH in the body — yet many ultra-processed foods contribute to acidity, inflammation, and digestive issues.

Profits from selling products that create health problems (e.g. sugar-heavy cereals, processed snacks)

Then profits again when consumers seek relief from those issues via over-the-counter medications rather than simple alternatives like baking soda

🔒 6. Misinformation and Consumer Disempowerment

Consumers are often discouraged from exploring cheap, natural remedies due to:

Lack of information

Misinformation about “dangerous” home remedies

Absence of strong health branding for products like baking soda

This reinforces a cycle of dependency on branded pharmaceuticals and expensive wellness products.

Get help to protect and grow your business faster with CheeringUpInfo

Businesses selling to people planning or living in retirement in UK

CheeringUp.info is the go-to marketing platform for UK businesses looking to connect with the fast-growing over 55s market. Retirees are one of the UK’s most valuable consumer groups—active, loyal, and with more disposable income than younger generations.

Whether you’re in finance, healthcare, leisure, travel, home services or lifestyle retail, we help you engage directly with this audience through:

✅ Trusted content placements

✅ Sponsored features and digital ads

✅ Email and social media marketing

✅ Affordable, flexible plans for SMEs

Tap into a market that values quality, experience, and trust.

📩 Email editor@cheeringup.info or visit www.cheeringup.info to start promoting your business today.

Reach More Over 55s in the UK – Smarter, Faster, Cheaper

Advertise Your Business More Effectively With CheeringUp.info Retirement Club Corporate Membership

Are you a UK SME business owner looking to grow your brand, generate leads, or increase sales?

Over 55s are the UK’s most powerful consumer group – and we help you connect with them directly and affordably.

✅ Why Join the Retirement Club Corporate Membership?

📣 Promote Your Business to over 55s across the UK

📩 Get Featured in our email newsletters and lifestyle articles

📱 Engage Customers via targeted social media promotions

💰 Save Money with affordable annual marketing packages

🌐 Build Trust by advertising on a platform created just for over 55s

🎯 Our Audience

55 to 75-year-olds with high buying power

Interested in lifestyle, health, travel, retirement, finance, and home

Loyal, trusted readers and subscribers across the UK

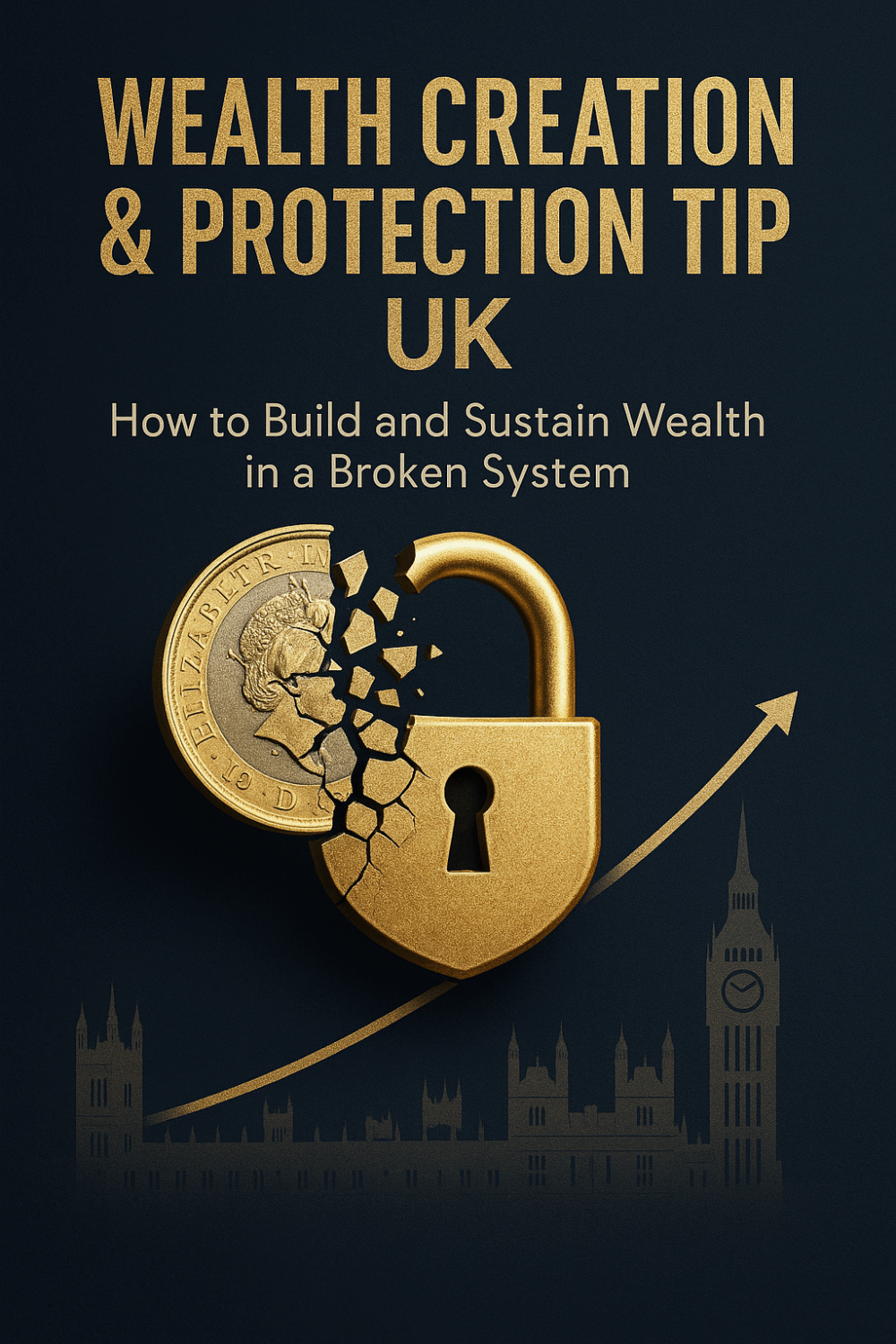

For UK wealth seekers frustrated by economic challenges. Actionable, controversial, and brutally honest wealth strategies you can adopt to build and protect your wealth.

Wealth Creation & Protection Tips UK: How to Build and Sustain Wealth in a Broken System

Introduction

The UK financial system is rigged against you. Taxes eat nearly half your income. Pensions are a gamble. Banks are fragile. Inflation silently steals your wealth. Yet most people follow the same broken path—work, save in cash, pray for a pension, and hope for the best. Hope is not a strategy.

Consider this: 1 in 3 UK adults has less than £1,000 in savings. Even those earning six figures are one crisis away from financial stress. The system isn’t designed to make you wealthy—it’s designed to keep you compliant. But there’s a way out.

They don’t want you to know these seven wealth secrets UK

This book is your escape plan.

Inside, you’ll find 9 proven wealth creation strategies tailored for the UK’s harsh economic reality. Each solution is broken into step-by-step actions, backed by real case studies, and designed to help you build, grow, and protect wealth—no matter what the economy throws at you.

This isn’t financial advice. It’s a wake-up call.

🔥 LIMITED-TIME LAUNCH OFFER: “Wealth Creation & Protection Tips UK” – The Ultimate Guide to Beating the Broken System! 🔥

Taxes stealing half your income? Pensions a gamble? Banks offering 0.5% while inflation rages? You’re being played.

eBook reveals 9 PROVEN STRATEGIES the rich use to:

– Gold vs. stocks vs. real estate – where to park cash now

BONUS: Real case studies of NHS nurses, TikTokers & retirees who escaped the rat race.

Let’s begin.

Disclaimer : This eBook is not financial advice. It is produced as a wealth creation educational tool and for entertainment purposes only. Individuals and business leaders should seek financial advice from a professional financial adviser in the UK before making any changes to their financial strategy or financial plans. We do not accept any liability whatsoever for any financial loss, injury or damage you may suffer by choosing to change your financial strategy or plan based on any information contained in this eBook.

Chapter 1: Why Wealth Creation in the UK is Harder Than Ever

The Silent Wealth Killer: Inflation & Taxation

Let’s start with a brutal truth: you’re being robbed. Not by thieves in the night, but by two silent predators—inflation and taxation.

The UK government takes up to 45% of your income before you even see it. Then, inflation—running at historic highs—erodes what’s left. If your savings aren’t growing by at least 5-7% a year, you’re getting poorer. And guess what? Most “safe” bank accounts pay less than 1%.

This isn’t an accident. The system is designed this way.

The Pension Time Bomb

You’ve been told to “save for retirement.” But here’s the ugly reality:

The state pension age keeps rising (it’ll likely hit 70+ by the time millennials retire).

Private pensions are tied to shaky markets—what happens if stocks crash when you need the money?

Final salary pensions? A dying relic. Most are underfunded.

Your pension isn’t a guarantee—it’s a gamble. And the house always wins.

The Illusion of “Safe” Investments

Banks love to sell you “low-risk” products. Bonds. Cash ISAs. Savings accounts. But low risk doesn’t mean no risk—it means slow death.

UK government bonds (gilts)? Yields barely beat inflation.

Cash savings? Losing value daily.

The FTSE 100? Stagnant for 20+ years.

If you’re relying on “traditional” investments, you’re falling behind.

Why Banks Can’t Be Trusted With Your Future

Banks don’t work for you. They work for shareholders.

They lend out your money at 5-10% interest while paying you 0.5%.

They push overpriced funds with hidden fees.

They’re heavily exposed to risky loans and derivatives.

Remember 2008? The next crisis is a matter of when, not if.

The Way Out

This isn’t doom-mongering—it’s a call to action. The system won’t save you. But you can save yourself.

In the next chapters, we’ll break down 9 proven strategies to:

✅ Slash your tax bill legally ✅ Grow wealth faster than inflation ✅ Protect what you’ve built from crises

The first step? Stop playing by the old rules.

Next: Chapter 2 – Wealth Solution #1: Tax Efficiency – Keep More of What You Earn

Chapter 2: Wealth Solution #1 – Tax Efficiency: Keep More of What You Earn

“The difference between tax avoidance and tax evasion? About five years in prison.” – Old City Saying

Let’s be blunt: You are overpaying taxes.

The UK tax system is a maze designed to siphon money from your pocket into HMRC’s coffers. But here’s the secret—the wealthy don’t pay more taxes, they pay smarter.

This chapter isn’t about dodging taxes (that’s illegal). It’s about exploiting every legal loophole, relief, and structure to keep more of your hard-earned money.

Why Tax Efficiency is Your #1 Wealth Accelerator

Think of taxes as a wealth leak. Every pound lost to unnecessary tax is a pound that could be:

Compounding in investments

Buying property equity

Funding your escape plan

The average UK taxpayer surrenders 42%+ of their income between income tax, NI, VAT, and stealth taxes. But with the right strategy, you could legally cut that to 20% or less.

Step 1: The ISA Shield – Tax-Free Growth

Problem: Savings and investments normally get hammered by capital gains tax (20%) and dividend tax (up to 39.35%).

Solution: Max out your £20,000/year ISA allowance.

Stocks & Shares ISA: Invest in equities/funds with 0% tax on gains/dividends

No Tech Giants – Missing the Apple/Amazon/Nvidia growth train

Brexit Hangover – Institutional money fled UK markets

Solution: Go global or go broke.

Step 1: The ETF Revolution (Set-and-Forget Wealth)

What the Pros Use:

VWRL (Global stocks, 0.22% fee) – Own 3,700 companies worldwide

SXR8 (S&P 500, 0.07% fee) – Pure US growth exposure

EIMI (Emerging markets) – Bet on Asia’s rise

How to Start:

Open a Stocks & Shares ISA (e.g., Interactive Investor)

Set up monthly £500 auto-invest

Wait 10 years → Likely double your money

Case Study: David, 35, invests £1,000/month in SXR8. At 7% growth → £1 million in 23 years with zero stock picking.

Step 2: Dividend Aristocrats (The Passive Income Machine)

Why Dividends Beat Rent:

No tenants, toilets, or taxes (in ISAs)

Compounding – Reinvest dividends for explosive growth

Best UK Picks:

Legal & General (LGEN) – 8% yield, pays like clockwork

British American Tobacco (BATS) – 9.5% yield, survives recessions

Global Stars:

Realty Income (O) – US “monthly dividend” REIT

Johnson & Johnson (JNJ) – 60+ years of dividend hikes

Pro Tip: In an ISA, all dividends are tax-free forever.

Step 3: Thematic Investing (Ride Mega-Trends)

5 Future-Proof Themes:

AI & Semiconductors – Nvidia (NVDA), ASML Holdings

Clean Energy – NextEra Energy (NEE), Brookfield Renewable

Healthcare Breakthroughs – CRISPR (EDIT), Moderna

Blockchain Infrastructure – Coinbase (COIN), Marathon Digital

Space Economy – SpaceX (private), Rocket Lab (RKLB)

How to Play It:

Thematic ETFs (e.g., ROBO, ICLN)

5% “mad money” rule – Speculate small on disruptors

Step 4: The Warren Buffett Strategy (For Busy People)

Buffett’s 90/10 Portfolio:

90% in S&P 500 index fund

10% in short-term government bonds

Why It Works:

Beats 90% of hedge funds over 20 years

Takes 10 minutes/year to manage

UK Version:

80% VWRL (global stocks)

20% IBTL (inflation-linked UK bonds)

Step 5: Short Selling & Options (Advanced Tactics)

When Markets Crash (Because They Will):

Inverse ETFs – S&P 500 down 1% → SQQQ up 3%

Put Options – Bet against overpriced stocks (e.g., Tesla)

Warning: Only for experienced investors. Practice with <1% of portfolio first.

The 10 Golden Rules of Stock Investing

Never listen to “tips” from finfluencers

Index funds > Stock picking for 99% of people

Rebalance annually (sell high, buy low)

Turn off the news – Noise destroys returns

Dollar-cost average (monthly buys beat timing)

Hold forever – Trading = tax bills + fees

Avoid UK-focused funds (chronic underperformers)

Dividends are king – Look for 25+ year payers

Keep 5% for “fun” bets (satisfies gambling urge)

Automate everything – Emotion is your worst enemy

Your First Trade (Today)

Open an ISA – Interactive Investor or Trading 212

Buy £500 of VWRL – Instant global diversification

Set up a £200/month direct debit – The magic starts now

Remember: The best time to invest was yesterday. The second-best? Right now.

Next Up: Chapter 5 – Cryptocurrency: High Risk, High Reward

“Bitcoin is either worth zero or a million dollars. There’s no in-between.” – Michael Saylor

Chapter 5: Cryptocurrency – High Risk, High Reward

“In the next 10 years, crypto will create more millionaires than the internet did.”

Let’s cut through the hype: 90% of cryptocurrencies are scams. But the 10% that aren’t will change finance forever.

This isn’t about gambling on meme coins. It’s about strategically positioning yourself in the greatest wealth transfer of our lifetime – while avoiding the landmines.

Why Crypto Can’t Be Ignored (The Case for 1-5% Allocation)

Three Uncomfortable Truths:

The Dollar is Dying

US debt grows $1 trillion every 100 days

When fiat fails, hard money (BTC) becomes insurance

Institutions Are All-In

BlackRock, Fidelity, and even UK pension funds now hold Bitcoin

The “scam” narrative is dead

Asymmetric Upside

Stocks might 10x in a decade

Crypto can 100x in 3 years

Key Stat: A £1,000 investment in Ethereum in 2015 would be worth £40 million today.

Step 1: The Bitcoin Standard (Your Digital Gold)

Why BTC is the Only “Safe” Crypto:

Fixed supply – Only 21 million will ever exist

Institutional adoption – Spot ETFs approved in 2024

Halving cycles – Price surges every 4 years (next: 2028)

How to Buy:

Use a UK-regulated exchange (Kraken, Coinbase)

Transfer to a hardware wallet (Ledger/Trezor)

Hold for 5+ years

Allocation Rule:1-3% of net worth – Enough to change your life, not ruin it.

Step 2: Ethereum – The Internet’s New Backbone

Why ETH > BTC for Growth:

Smart contracts – Powers 90% of DeFi/NFTs

Staking rewards – Earn 3-5% annually (vs. 0% in banks)

Upcoming upgrades – Faster, cheaper transactions

Pro Move: Stake your ETH via Lido Finance for liquid yields.

Step 3: Altcoin Hunting (Where the 100x Plays Hide)

The 3 Filters for Finding Gems:

Real utility (Not just hype) – e.g., Chainlink (data feeds)

Strong team – Founders with track records

Low market cap (<£1 billion)

2024’s Top Picks:

Solana (SOL) – The “Visa” of crypto (65k transactions/sec)

Polkadot (DOT) – Connects blockchains

Arbitrum (ARB) – Ethereum scaling solution

Warning: Never invest more than you can afford to lose.

Step 4: Crypto Passive Income (Earn While You HODL)

5 Ways to Make Your Coins Work:

Staking – 3-10% APY on Ethereum, Cardano

Liquidity Mining – Provide tokens to DeFi pools (10-50% APY)

Airdrops – Free tokens for early users (some worth £10k+)

NFT Royalties – Earn when your art resells

Crypto Savings – 8% on stablecoins (vs. 0.5% at banks)

Case Study: Sarah earned £12,000 in airdrops just by using new DeFi apps early.

Step 5: The Exit Strategy (How to Cash Out)

The UK Tax Trap:

Capital Gains Tax – 20% on profits over £6,000 (2024)

Income Tax – If you trade frequently

Tax Hacks:

Use your ISA – Some platforms offer crypto ISAs

Harvest losses – Offset gains with losing trades

Move to Portugal – 0% crypto tax for 10 years

Golden Rule:Take profits – Nobody went broke selling at 10x.

The 10 Crypto Commandments

Not your keys, not your crypto – Avoid exchanges like Celsius

Ignore “to the moon” hype – Do your own research

DCA in, DCA out – Don’t try to time peaks

Keep seed phrases offline – Steel plates > paper

Avoid leverage – 95% lose money trading futures

Focus on BTC/ETH first – Then explore alts

Beware of “guaranteed” returns – If it sounds too good…

Prepare for 80% drops – Volatility is normal

Ignore FOMO – There’s always another opportunity

Have an exit plan – Price targets + stop losses

Your First Crypto Purchase (Today)

Sign up to Kraken – UK-regulated, low fees

Buy £100 of Bitcoin – Start small, learn the ropes

Set up a £50/month auto-buy – Dollar-cost average in

Remember: Crypto is the highest-risk, highest-reward asset class. Allocate accordingly.

Next Up: Chapter 6 – Gold & Precious Metals: The Ultimate Hedge

“Gold is money. Everything else is credit.” – J.P. Morgan

Chapter 6: Gold & Precious Metals – The Ultimate Hedge

“When the music stops, gold is the only chair left to sit on.”

Let’s face an uncomfortable truth: Your paper money is a liability, not an asset.

While governments print currency at will, gold has preserved wealth for 5,000 years – through empires, wars, and financial collapses.

This chapter isn’t about getting rich. It’s about staying rich when the system falters.

Why Every Portfolio Needs 5-15% in Gold

Three Scenarios Where Gold Saves You:

Currency Collapse

UK money supply grew 44% since 2020

When faith in sterling erodes, gold soars

Stock Market Crash

Gold jumped 25% in 2008 while stocks tanked

Inverse correlation to equities

Geopolitical Crisis

Russia/Ukraine war → gold hit all-time highs

The ultimate “portable wealth”

Key Stat: Gold has never gone to zero – unlike 99% of stocks and cryptos.

Step 1: Physical Gold – The Bedrock Holding

What to Buy (And Where):

Britannia Coins – Capital gains tax-free, 91.7% pure

1kg Bars – Lowest premium (3-5% over spot)

Jewelry – Wearable wealth (but high markups)

Storage Solutions: ✔ Home safe – For <£50k (get proper insurance) ✔ Vaults – Loomis, Brinks (0.5% annual fee) ✔ Bank safety deposit boxes – But recall Cyprus bail-ins

Pro Tip: Never advertise your holdings.

Step 2: Gold ETFs – Paper Exposure

Best UK Options:

SGLN – Physical-backed, 0.15% fee

PHGP – GBP-hedged version

Warning: ETFs are counterparty risk – If the bank fails, your gold might too.

Side Hustle #4: Airbnb Arbitrage (No Property Needed)

The Hack:

Convince landlords to let you manage their empty flats

Furnish cheaply (IKEA + Facebook Marketplace)

List on Airbnb

Keep 30-50% of profits

2024 Opportunity:

Corporate rentals (3-6 month contracts) pay 2x normal rents

Case Study:

Priya manages 8 London properties making £15k/month (without owning any).

Side Hustle #5: TikTok Affiliate Marketing

Step-by-Step:

Sign up for Amazon Associates/Awin

Find trending products (TikTok Shop)

Create 30-second demo videos

Post 3x/day (Algorithm rewards consistency)

Earnings:

£50-500 per sale (High-ticket items)

Viral potential: One video can make £10k+

Pro Tip:

Use CapCut auto-captions + trending sounds

Side Hustle #6: AI Content Agencies

The 2024 Boom: Businesses desperately need: ✔ Blog posts (ChatGPT) ✔ Social media (Canva Magic Design) ✔ Videos (Synthesia AI avatars)

Pricing:

£500/month for 8 posts

Profit margin: 80%+ (AI does the work)

How to Get Clients:

Cold email: “I’ll create your next 3 posts free—if you like them, we’ll talk.”

Side Hustle #7: Car Park Rentals

The Ultimate Passive Play:

Lease unused land (farmers/churches)

Install ANPR cameras (PayAsYouPark)

Charge £5-15/day

Profit: 70% margins

Real Numbers:

20 spaces x £10/day = £6k/month

Costs: £500 land lease + £2k camera setup

The 5 Commandments of Side Hustles

Start before you’re “ready” – Action beats planning

Double down on what works – Kill underperformers

Document everything – Turn processes into sellable courses

Outsource early – Your time is worth £100+/h

Reinvest profits – Scale or die

Your First £1,000 (Within 30 Days)

Pick One: ✔ Post 3 TikTok affiliate videos daily ✔ Cold email 20 local businesses for lead gen ✔ Upload 10 digital products to Gumroad

Remember: Businesses compound. Salaries don’t.

Next Up: Chapter 8 – Debt as a Tool: Good Debt vs. Bad Debt

“The rich use debt as a weapon. The poor fear it like a disease.”

Chapter 8: Debt as a Tool – Good Debt vs. Bad Debt

“The rich don’t avoid debt—they weaponise it.”

Let’s shatter the biggest financial myth: “All debt is bad.”

The truth? Strategic debt builds empires.

Elon Musk used debt to buy Twitter

Property moguls leverage mortgages to own billions

Even the UK government runs on 100%+ debt-to-GDP

This chapter reveals how to turn debt into your wealth accelerator—without ending up bankrupt.

The Life-Changing Difference Between Good & Bad Debt

Bad Debt: ❌ Consumer debt (Credit cards at 24% APR) ❌ Car loans (Depreciating asset) ❌ Payday loans (Financial suicide)

Good Debt: ✅ Mortgages (Leverage appreciating assets) ✅ Business loans (Scales cashflow) ✅ Margin loans (Invest in stocks at 3% interest)

Rule of Thumb: If debt buys appreciating assets or income streams, it’s good. If it buys liabilities or depreciating trash, it’s bad.

Debt Strategy #1: The BRRRR Method Revisited

How the Pros Buy Property With “No Money Down”:

Borrow £150k (75% mortgage) to buy £200k property

Renovate (£20k spent) → Now worth £250k

Refinance (New 75% mortgage = £187k)

Repay original loan → £17k profit in your pocket

Repeat with the recycled cash

Real-Life Example:

Simon built a £5m portfolio starting with just £30k by recycling debt 12 times.

Debt Strategy #2: Stock Market Margin

How to Safely Leverage Investments:

Interactive Brokers charges just 3% interest on margin loans

Borrow against your portfolio to buy more stocks

The Math:

Invest £100k

Borrow another £50k at 3%

If portfolio grows 7% annually → £10.5k gain (7% of £150k)

Minus £1.5k interest = £9k net (9% return on your £100k)

Nuclear Option:

Use margin to buy leveraged ETFs (e.g., 3x S&P 500)

Warning: Only for experienced investors—can liquidate you fast.

Debt Strategy #3: Business Leverage

How Startups Scale Fast:

Take a £50k startup loan (UK gov-backed)

Hire 2 salespeople → Grow revenue to £20k/month

Refinance with invoice financing (Get 80% upfront)

Cycle accelerates

Key Move:

Always match debt duration to asset life

Short-term debt for inventory

Long-term debt for equipment

Debt Strategy #4: The “Never Pay Cash” Principle

Why the Rich Finance Everything:

Opportunity cost: £100k in cash buying property = £100k not compounding elsewhere

Inflation benefit: Debt gets cheaper over time

What to Always Finance: ✔ Rental properties ✔ Business equipment ✔ Appreciating assets

What to Never Finance: ✖ Holidays ✖ Clothes ✖ Anything that won’t make you money

Debt Strategy #5: The Credit Card Hack

How to Get Interest-Free Loans:

Open a 0% purchase card (24 months interest-free)

Buy £10k of business inventory

Sell for £15k within 12 months

Pay off card before interest hits

Advanced Play:

Balance transfer to another 0% card (Extend free money)

Warning:Only if you’re disciplined—miss payments and rates jump to 30%.

The 5 Debt Commandments

Never leverage more than 50% of asset value

Ensure cashflow covers 2x interest payments

Fix rates when borrowing cheap (Lock in 2% mortgages)

Have an exit plan (Refinance/sell if rates rise)

Walk away if math changes (Strategic defaults exist)

Your First Strategic Debt Move (This Month)

Pick One: ✔ Refinance your home (If equity >25%) ✔ Open a margin account (Start with 10% leverage) ✔ Apply for a 0% business card

Remember: Debt is fire—useful when controlled, deadly when not.

Next Up: Chapter 9 – Offshore & Alternative Investments: The Ultimate Escape Plan

“The government wants you poor and dependent. Offshore options break those chains.”

Chapter 9: Offshore & Alternative Investments – The Ultimate Escape Plan

“The UK government doesn’t want you to know these strategies exist.”

Let’s confront reality: The UK is one of the worst places to build and preserve wealth.

45%+ tax rates

Inheritance tax grabs 40% at death

Frozen pension allowances

But there’s a way out.

This chapter reveals legal offshore structures and alternative investments used by the global elite to protect—and grow—their wealth beyond UK borders.

Why You Need Offshore Exposure

3 Unavoidable UK Wealth Threats:

Fiscal Drag – More people being pushed into higher tax brackets

Regulatory Creep – Increasing restrictions on pensions/ISAs

Political Risk – Potential wealth taxes or capital controls

Solution:Geographic diversification – because no government gets to touch 100% of your money.

Strategy #1: The QROPS Pension Escape

How It Works:

Transfer your UK pension to Malta, Gibraltar, or Isle of Man

Benefits:

Avoid UK lifetime allowance (£1.07M cap)

0% tax on growth (vs. 45% in UK)

Flexible withdrawals (Take lump sums tax-free)

Who It’s For: ✔ Expats ✔ Anyone with pension >£500k ✔ Those planning to retire abroad

Case Study: David, 55, saved £210,000 in taxes by moving his £1.2M pension to Malta.

Strategy #2: Non-Dom Status (The Billionaire Loophole)

Shockingly Legal Tax Avoidance:

Claim “non-dom” status if you were born abroad or have foreign parents

Pay 0% UK tax on overseas income (Unless you bring it to the UK)

How to Qualify:

Have a second passport (Portugal, Italy, etc.)

Keep a foreign bank account

File UK tax return as non-dom

Pro Tip: Combine with 7-year rule – Bring offshore money to UK tax-free after 7 years.

Strategy #3: Offshore Real Estate

Top 3 Tax-Friendly Markets:

Dubai – 0% income/capital gains tax

Portugal – NHR scheme (10% flat rate for 10 years)

Malaysia – MM2H visa (Foreign income tax-exempt)

How to Buy:

Offshore company (Owns property, not you personally)

Currency hedge – Borrow in USD/EUR to offset GBP risk

Warning: Avoid “hot” markets like Thailand (Foreign ownership restrictions).

Strategy #4: Crypto Offshore Banking

The New Swiss Banks:

Puerto Rico – 0% capital gains tax for crypto (Act 22)

Singapore – No crypto capital gains tax

El Salvador – Bitcoin is legal tender

Step-by-Step:

Establish residency (e.g., Puerto Rico – 183 days/year)

Make your children (or future children) beneficiaries

0% inheritance tax – Assets skip UK probate

Cost: ~£15k setup, but saves 40% IHT on £1M+ estates.

The 5 Offshore Commandments

Never hide money – Use legal structures, not secrecy

Keep UK ties minimal – Don’t trigger “deemed domicile”

Work with specialists – Offshore tax lawyers are worth it

Diversify jurisdictions – Don’t put all eggs in one tax haven

Stay compliant – File FBAR if you have >$10k overseas

Your First Offshore Move (Within 90 Days)

Pick One: ✔ Open a Gibraltar QROPS (If pension >£300k) ✔ Buy €500k Portuguese property (For NHR visa) ✔ Form a Seychelles LLC (For crypto/consulting income)

Remember:It’s not about tax evasion—it’s about tax optimization.

Next Up: Chapter 10 – Protecting What You’ve Built: Trusts, Wills & Asset Shielding

“The government will take 40% at death—unless you stop them.”

Chapter 10: Protecting What You’ve Built – Trusts, Wills & Asset Shielding

“Building wealth is hard. Losing it is easy.”

Here’s a chilling fact: 60% of wealthy families lose their fortune by the second generation.

Why?

Lawsuits

Divorce settlements

Inheritance tax grabs

Bad business partners

This chapter reveals bulletproof strategies to lock down your wealth—so it survives lawsuits, divorces, and even your own mistakes.

The 4 Wealth Killers (And How to Stop Them)

1. Inheritance Tax (The 40% Government Heist)

Current Threshold: £325k (frozen until 2028)

Reality: A £2m estate pays £670,000 to HMRC

2. Divorce (The 50/50 Trap)

UK courts split all assets—even pre-marriage wealth

Business interests are not protected

3. Lawsuits (Your Biggest Risk)

One accident, one disgruntled employee = lose everything

4. Care Home Fees (£100k+/Year Wipeout)

Local authorities can seize your home to pay for care

Weapon #1: The Family Trust (Your Legal Fortress)

How It Works:

Transfer assets (property, investments) to a trust

You control it as trustee—but legally don’t own it

Wealth passes to heirs tax-free

Best Jurisdictions:

UK Discretionary Trust (For IHT protection)

Guernsey/Jersey Trust (For lawsuit shielding)

Case Study: The Duke of Westminster avoided £9bn in inheritance tax via trusts since 1950.

Weapon #2: The Prenup That Actually Works

Standard Prenup: Often ignored by UK courts

Ironclad Version:

Signed 2+ years before marriage

Full financial disclosure

Separate legal representation

“Needs” provision (Prevents unfairness claims)

Pro Tip: Combine with a postnuptial agreement every 5 years.

Weapon #3: The Ltd Company Shield

Why Your Home Should Be Owned by a Company:

Lawsuit Protection: Creditors can’t seize it

Care Home Dodge: Not counted as personal asset

Inheritance Bonus: Shares pass via trust

How To:

Form a property holding Ltd

Sell your home to it (Stamp duty applies)

Rent it back from the company

Cost: £2k setup, saves £400k+ in potential losses.

Weapon #4: The Offshore LLC Shell Game

For Business Owners:

Set up a Nevis LLC (No public records)

Make it own your UK operating company

Result:

Lawsuits stop at Nevis

UK courts can’t seize foreign assets

Famous Users: Google, Apple (via Ireland/Netherlands structures).

Weapon #5: The “Die Alive” Strategy

How to Gift £1m Tax-Free:

7-Year Rule: Gifts fall out of estate after 7 years

Annual £3k Allowance: £21k over 7 years (per parent)

Wedding Gifts: £5k-£10k tax-free per child

Nuclear Option:Loan Trusts – “Lend” money to heirs that’s never repaid.

The 5 Protection Commandments

Never own anything personally – Use trusts/companies

Document everything – Undated gifts = tax evasion

Review every 3 years – Laws change

Keep some assets abroad – UK courts can’t touch Isle of Man

Insure the rest – £500/year umbrella policy covers £5m lawsuits

Your First Protection Move (This Month)

Pick One: ✔ Set up a will + letter of wishes (Even if you have nothing) ✔ Form a property Ltd Co (If you own a home) ✔ Gift £3k to kids now (Starts 7-year clock)

Remember:Wealth preservation isn’t sexy—until it saves your family’s future.

Next Up: Chapter 11 – The Ultimate Wealth Creation Strategy: Combining All 9 Solutions

“The rich don’t use one strategy—they combine them like financial judo.”

Chapter 11: The Ultimate Wealth Creation Strategy – Combining All 9 Solutions

“The rich don’t pick one wealth strategy—they stack them like a financial Jenga tower that never falls.”

Here’s the brutal truth: No single tactic in this book will make you wealthy.

But combine 3-5 of them?

That’s how you build £10M+ net worth in a decade.

This chapter shows you exactly how to layer these strategies—with real-world examples of people who’ve done it.

The Wealth Stacking Principle

How Ordinary People Become Millionaires:

Weapon

Example Combination

Result

Property

Buy 2 BTLs via Ltd Co

£2,000/month cashflow

Tax Hacks

Pension + ISA stuffing

£45k/year tax-free

Side Hustle

Digital product empire

£5k/month passive

Debt

Refinance equity to buy more

Portfolio doubles

Offshore

Malta QROPS + Portugal NHR

10% tax rate

The Math:

£200k/year income

£80k/year taxes → £25k/year after optimization

£1.5M net worth in 5 years

Case Study 1: The NHS Doctor Turned Property Tycoon

Starting Point:

£75k salary → £45k after tax

£50k savings

Wealth Stack:

Side Hustle: Launched medical training courses (£8k/month)

Property: Used profits to buy 4 HMOs via Ltd Co (£15k/month rent)

Tax: Maxed pension + ISAs (Saved £22k/year in taxes)

Debt: Refinanced properties to buy 2 more

Protection: Family trust holds all assets

Result:£3.2M portfolio in 7 years (Now works 2 days/week)

Case Study 2: The TikTok Millionaire

Starting Point:

Retail job (£22k/year)

£3k crypto gains

Wealth Stack:

Crypto: Went all-in on Ethereum 2017 (£250k by 2021)

Tax: Moved to Portugal (0% crypto tax)

Business: Started AI content agency (£30k/month revenue)

Investments: Gold + S&P 500 as hedge

Debt: Used margin loans to amplify returns

Result:£7M net worth at 28

The 5-Step Wealth Stacking Blueprint

Step 1: Pick Your Foundation

Property OR business OR investments

Step 2: Add Leverage

Mortgages, margin loans, business credit

Step 3: Slash Taxes

ISAs, pensions, offshore structures

Step 4: Create Multiple Streams

Rental income, dividends, digital products

Step 5: Lock It Down

Trusts, wills, asset protection

The Nuclear Stack: Ultra-High Net Worth Playbook

Earn £500k+ (Business or investments)

Non-dom status (Pay 0% on foreign income)

QROPS pension (Avoid lifetime allowance)

Channel Islands trust (40% IHT savings)

Swiss annuity (Tax-free growth)

Example: Saves £280k/year in taxes vs. UK resident.

Your First Stack (Start Today)

For Employees:

Max pension + ISA (Instant tax savings)

Start a side hustle (Affiliate marketing takes 2h/week)

Buy 1 rental property (Use spare room allowance)

For Business Owners:

Pay dividends not salary (Save 20% tax)

Buy commercial property via Ltd Co

Set up offshore holding company

The One Fatal Mistake

“I’ll do it later.”

ISAs expire yearly

Tax loopholes close

Compound growth needs time

Action beats perfection.

Final Chapter: Chapter 12 – The One Mistake That Will Destroy Your Wealth

“All these strategies won’t matter if you make this error.”

Chapter 12: The One Mistake That Will Destroy Your Wealth

“You can do everything right—and still lose it all with this single error.”

Let me tell you about John.

John was smart. He:

Built a £2M property portfolio

Maxed his ISAs and pension

Had offshore structures

Then—one lawsuit later—he lost everything.

This chapter reveals the fatal flaw that crushes 90% of wealthy people, and how to bulletproof against it.

The Wealth Killer No One Talks About

It’s not taxes. Not market crashes. Not even divorce.

The silent destroyer is: Single Point of Failure dependence.

All eggs in one property market

All income from one business

All assets in one country

How the Rich Get Wiped Out:

2008: Property-only investors went bankrupt

2020: Restaurant owners with no online income

2022: Crypto “all-in” traders who ignored gold

The 5 Warning Signs You’re At Risk

“My property portfolio is my pension”

What if rent controls come? Or cladding scandals?

“My business earns £300k/year—I’m set”

One algorithm change (Google, TikTok) can ruin you

“I’m all in stocks—they always recover”

Japan’s Nikkei still hasn’t recovered its 1989 peak

“My accountant handles everything”

Most don’t understand offshore/trust strategies

“I’ll protect my wealth later”

Lawsuits/strokes/heart attacks don’t wait

The Bulletproof 3-Layer Shield

Layer 1: Asset Diversity

Geographic: UK + EU + Asia assets

Class: Property + crypto + gold + businesses

Currency: GBP + USD + CHF

Layer 2: Income Streams

Rental income

Dividend stocks

Digital products

Consulting (Rule: Never rely on just 1-2)

Layer 3: Legal Armor

UK Ltd Co for business

Gibraltar trust for assets

Portuguese NHR for tax

Case Study: How Sarah Survived 3 Disasters

2020: Her London Airbnbs crashed (Pandemic)

Saved by: Online course income (£12k/month)

2022: Crypto portfolio dropped 70%

Saved by: Gold holdings (+20% that year)

2023: HMRC investigation

Saved by: Malta QROPS (All docs clean)

Lesson:Each disaster only took one layer—never all three.

The “Do This Now” Checklist

Diversify Income

Start one side hustle this month (See Ch7)

Move 5% to Hard Assets

Buy physical gold + Bitcoin (Ch5+6)

Get Basic Protection

Will + life insurance (Ch10)

Go Offshore

Open one int’l account (Revolut/Wise doesn’t count)

Find Your Weak Link

What would ruin you if it failed? Fix it.

The Final Word

Wealth isn’t about getting rich—it’s about staying rich.

The strategies in this book work. But only if you:

Start now

Stack multiple layers

Never get complacent

Your next move? Turn the page back to Chapter 1—and take action today.

Want me to create your own personalised risk audit for your financial situation? Join our Wealth Hub and participate in our Wealth Pod.

Get help to protect and grow your business faster with CheeringUpInfo

Tax-efficient buy-to-let strategy for retirement income UK. If you’re searching for a tax-efficient buy-to-let strategy for retirement income, this is your blueprint. Read a non-technical accessible eBook now to avoid missing UK investment retirement lifestyle improvement tips today.

The Property Millionaire’s Retirement Blueprint: How to Build a Tax-Efficient Buy-to-Let Empire Using Limited Companies

For UK Investors 55+: Beat inflation & build lasting wealth with buy-to-lets in limited companies! This eBook reveals:

✅ Step-by-Step SPV Setup – Legally save £12K+/year vs personal ownership

✅ 5-Year Plan to scale from 2 to 10+ properties (case study: £9,200/month income)

✅ Mortgage Hacks – How lenders approve new companies

Imagine this: You’re 55, sitting on a £500,000 cash pile. Comfortable? For now. But at 3% inflation, in 20 years, that money will be worth just £276,000 in today’s terms. Worse, if you’re drawing £30,000 a year from savings, you’ll run out of money before you hit 80.

Scary? It should be.

But here’s the good news: There’s a way to turn that cash into a growing, inflation-proof income stream that lasts the rest of your life—without gambling on stocks or praying for pension reforms.

The solution? Property. Mortgages. Limited companies.

This isn’t about getting rich quick. It’s about building a retirement machine—one that pays you more as rents rise, more as properties appreciate, and more as tax-efficient profits stack up inside a company structure.

In this guide, you’ll get a step-by-step playbook for:

Setting up the right limited company structure (one vs. multiple companies—and why it matters).

Securing mortgages inside that company (even if you’ve never run a business before).

Buying properties that work for your retirement (not just “any” buy-to-lets).

Extracting profits in the most tax-efficient way (legally paying less to HMRC).

Scaling to 5, 10, or 20 properties without drowning in admin.

We’ll use real case studies—like the 62-year-old who turned £250K into £1.2M of property equity in 7 years, now paying him £4,500/month after tax. No fluff. No jargon. Just actionable strategies that work in today’s market.

Ready? Let’s build your retirement fortress—one brick (and mortgage) at a time.

“At 3% inflation, £500,000 today is worth just £276,000 in 20 years—enough to last most retirees only 12 years at £30,000/year withdrawals.”

Chapter 1: The Retirement Cash Trap

John and Sheila thought they’d nailed retirement. £750,000 in savings. A paid-off house. Dreams of cruises and grandkids.

Then reality hit.

After 10 years of 2.5% interest and £36,000/year withdrawals, their pot had shrunk to £390,000. Worse, inflation meant that £36,000 now bought what £28,000 did a decade earlier.

“We never imagined running out,” John admitted. “But at this rate, we’ll be broke by 78.“

But here’s the brutal truth—your money is melting away faster than you think.

At just 3% inflation, that £500,000 will be worth only £276,000 in today’s money in 20 years. If you withdraw £30,000 a year to live on? You’ll run out before your 80th birthday.

And that’s before factoring in unexpected costs—care home fees, medical bills, or helping your kids onto the property ladder.

Pensions Are a Gamble

The stock market swings wildly. A 20% crash just before retirement could slash your income forever.

Case Study: David, 62, saw his £400,000 pension pot drop to £320,000 in 2022. He now gets £1,200 less per month than planned.

Cash Savings Lose Value Every Year

Even “high-interest” accounts pay less than inflation. Your money is guaranteed to buy less over time.

Example: £100,000 at 2% interest = £148,595 in 20 years. But at 3% inflation, it’s really worth just £82,000 in today’s terms.

Bonds & ISAs Can’t Keep Up

The best 5-year fixed-rate bonds pay ~5%. After tax and inflation? Barely breaking even.

Rental Income – Inflation-proof cash flow (rents rise with costs).

Capital Growth – Property doubles every 10-15 years historically.

Leverage – A £200,000 house with a 75% mortgage only ties up £50,000 of your cash.

The Pension vs. Property Showdown

Scenario: You have £250,000 to invest at age 55.

Pension Route:

Draw 4% per year = £10,000/year.

After 20 years? Pot likely depleted.

Property Route (Limited Company):

Buy 4 x £200,000 houses (25% deposit each).

Rent: £800/month each = £38,400/year gross.

After mortgage costs & tax: £18,000+/year profit.

Plus the properties now worth ~£1,000,000.

The Psychological Edge

Unlike stocks, property is:

Tangible – You can see and improve it.

Control – Raise rents, refinance, or sell on your timeline.

Predictable – Tenants pay rent like clockwork with proper vetting.

Your First Action Step

Do this today:

Open a spreadsheet.

List your current savings/pensions.

Calculate their real value in 10 years (subtract 3% inflation yearly).

The gap between that number and the income you’ll need? That’s why you need property.

Next Chapter Preview: “Why a Limited Company? (And When It’s Not the Right Choice)”

The £12,000/year tax loophole HMRC doesn’t advertise.

The one scenario where owning property personally still beats a company.

CHAPTER 2: WHY A LIMITED COMPANY? (AND WHEN IT’S NOT THE RIGHT CHOICE)

The £12,000 Tax Loophole Every Property Investor Should Know

Let me tell you about Sarah, a 58-year-old dentist from Manchester. She owned three buy-to-lets personally, earning £36,000/year in rent. After income tax at 40% and mortgage interest deductions, she kept just £19,000. Then she switched to a limited company structure – and legally paid £12,000 less in tax that first year.

This is why smart investors are flocking to limited companies. But it’s not right for everyone. Let’s break it down.

The Tax Tsunami Hitting Personal Landlords

Since 2017, three changes have crushed personal landlords:

Mortgage interest tax relief phased out (now just a 20% credit)

Section 24 rules making rental income look artificially high

Capital Gains Tax still at 18-28% when you sell

For higher-rate taxpayers, this is brutal. But limited companies get: ✔ Full mortgage interest deduction ✔ Corporation Tax at just 25% (vs 40-45% income tax) ✔ 19% tax on capital gains (vs 28% personally)

The Numbers Don’t Lie: Company vs Personal

Let’s compare £50,000 rental profit:

Personal (40% taxpayer)

Limited Company

Tax Rate

40%

25%

Mortgage Interest (30k)

Only 20% relief

Full deduction

Net Tax Bill

£20,000

£8,000

Annual Savings

–

£12,000

When a Limited Company Doesn’t Make Sense

The One-Property Wonder If you own just one £150,000 flat making £7,500/year rent? The £500 company accounts cost might outweigh savings.

Basic Rate Taxpayers Earning under £50,270? Your 20% tax rate is close to Corporation Tax – less benefit.

Planning to Sell Soon Companies pay 19% on gains, but extracting cash later may trigger dividend tax. Personal CGT allowance (£3,000) can sometimes work better.

The Hidden Costs Nobody Talks About

Accountancy fees (£800-£1,500/year vs £300 personally)

Mortgage rates 0.5-1% higher than personal BTLs

More complex tax returns (CT600, confirmation statements)

Case Study: The Semi-Retired Couple Who Got It Wrong

Mike and Jenny transferred their £1.2m portfolio into a company… then discovered: ✖ Their 0.5% personal BTL mortgages became 2.5% company loans ✖ £3,500/year in new accounting/legal fees ✖ No CGT exemption on transfer

They actually lost money for three years. The lesson? Transition gradually.

Your 3-Step Action Plan

Calculate Your Tipping Point Use this formula: (Current Tax Rate – 25%) × Rental Profit = Annual Savings If savings exceed £1,500 (typical company costs), switch.

Test With One Property First Transfer just one property to test the waters. Use “incorporation relief” to defer CGT.

Interview Specialist Accountants Ask:

“How many property clients do you have?”

“Can you show me a sample CT600 for rentals?”

“What’s your process for profit extraction?”

The Ultimate Hack: Mixed Ownership

Sophisticated investors use both:

Keep low-yield properties personally (to use CGT allowance)

Put high-mortgage properties in companies (maximize interest relief)

Coming in Chapter 3… “One Company or Multiple? The Mortgage & Tax Trade-Off”

Why some investors create a “lender-friendly” structure with 4 properties per company

How to split portfolios to avoid hitting the £250,000 profits threshold

CHAPTER 3: ONE COMPANY OR MULTIPLE? THE MORTGAGE & TAX TRADEOFF

The Million-Pound Question: Single SPV or Multiple Companies?

Meet two investors:

David put all 8 properties in one limited company. Simple. Until lenders said “no more mortgages” at property #5.

Sarah set up two companies with 4 properties each. She just got her 9th mortgage approved last week.

Who made the right call?

The answer isn’t one-size-fits-all—it depends on tax, lending risk, and your endgame. Let’s break it down.

SECTION 1: THE LENDER’S PERSPECTIVE (WHY TOO MANY PROPERTIES = MORTGAGE REJECTIONS)

The “4-Property Rule” Most Investors Miss

Many high-street lenders impose hidden limits per company:

Santander: Max 3-4 BTL mortgages per SPV

Paragon: Up to 10, but rates rise after 5

High Street Banks: Often reject after 2-3

Why? Risk concentration. If one tenant stops paying, it could domino across all properties in that company.

➡ Solution: Spread properties across multiple SPVs (Special Purpose Vehicles) to keep lenders happy.

Case Study: The Investor Who Hit a Brick Wall

James had 6 properties in one company. At property #7, every lender declined him. He had to:

Spend £1,200 setting up a new company

Wait 6 months to build its credit file

Accept higher interest rates (2.1% → 2.8%)

Cost of mistake: £16,000 in lost rent over 6 months + higher lifetime mortgage costs.

SECTION 2: THE TAX TRIGGERS (WHEN ONE COMPANY COSTS YOU THOUSANDS)

Select “Incorporate a private company limited by shares”

Use “Model Articles” (don’t pay for custom ones)

Skip adding shareholders initially (you can add later)

Critical Mistake to Avoid:

Listing your home address as the registered office (it becomes public). Instead:

Use your accountant’s address, or

Pay £39/year for a virtual office (e.g., Regus)

STEP 3: OPENING A LENDER-FRIENDARY BUSINESS BANK ACCOUNT

The 3 Best Banks for New Property Companies:

Bank

Time to Open

Key Requirement

Best For

Tide

1-2 days

No trading history needed

Fast setup

Starling

3-5 days

Must be UK resident

Best app/API

HSBC

7-10 days

£25k+ deposit

High-street credibility

Pro Tip: Apply to two banks simultaneously in case one rejects you.

STEP 4: SETTING UP YOUR ACCOUNTING (AVOIDING THE £5,000 MISTAKE)

Must-Have Systems:

Digital Bookkeeping (Free Option: Wave Apps)

Track income/expenses from Day 1

Separate Business Card

Never mix personal/property spending

VAT Decision

Most BTL companies don’t need to register (unless opting for FRS)

Case Study: The Landlord Who Lost £5,000

Didn’t track mileage to view properties

Missed £2,400 in allowable expenses

Paid £600 fines for late filings

STEP 5: GETTING YOUR FIRST MORTGAGE APPROVAL

The “New Company” Mortgage Hack:

Wait 3 Months (Some lenders require this)

Use a Specialist Broker (Free Option: L&C Mortgages)

Prepare:

3 Months of Business Bank Statements

Personal SA302s (last 2 years)

CV Showing Property Experience

Best “New SPV” Lender (2024):

Paragon Bank

Rates: 2.89% (75% LTV)

Accepts companies <6 months old

YOUR 7-DAY COUNTDOWN CHECKLIST

Day

Task

Time Needed

1

Choose company name + SIC codes

20 mins

2

Register with Companies House

17 mins

3

Order company seal/certificate (optional)

Online

4

Apply to 2 business banks

45 mins

5

Set up accounting software

30 mins

6

Draft shareholder agreement (if needed)

1 hour

7

Meet with mortgage broker

1 hour

COMING IN CHAPTER 5…

“Mortgage Magic: How to Borrow Inside a Company (Even as a Newbie)”

The 5 lenders who approve new SPVs without personal income proof

How to structure your director’s salary to boost affordability

CHAPTER 5: MORTGAGE MAGIC – HOW TO BORROW INSIDE A COMPANY (EVEN AS A NEWBIE)

The Secret That Lets You Buy Properties With Almost No Cash

When Karen set up her property company, every high street lender rejected her. “No trading history,” they said.

Then she discovered specialist lenders who said yes—and used their money to buy 4 properties in 18 months, putting down just £15,000 of her own cash.

Here’s exactly how she did it—and how you can too.

SECTION 1: THE “NEW SPV” MORTGAGE LANDSCAPE (2024 UPDATE)

Why High Street Banks Say No (And Who Says Yes)

Most banks want: ✖ 2+ years of company accounts ✖ Proven rental income

But these specialist lenders don’t:

Lender

Min. Company Age

Key Requirement

Max LTV

Best Rate (2024)

Paragon

0 months

Director’s personal income

75%

2.89%

Kent Reliance

0 months

6 months’ reserves

80%

3.15%

Foundation

6 months

No CCJs

75%

3.34%

Pro Tip: Rates are 0.5-1% higher than personal BTLs—but the tax savings more than cover it.

SECTION 2: THE AFFORDABILITY HACKS (BUY MORE WITH LESS)

Hack #1: The “Director’s Salary” Trick

Most lenders calculate affordability two ways:

Company profits (if established)

Director’s personal income

Solution: Pay yourself a £12,570 salary (tax-free allowance):

Costs the company £1,200/year in Employer NICs

Boosts mortgage offers by £100,000+

Hack #2: The “Rent-to-Rent” Workaround

No rental history? Use:

An independent valuation (£150) showing potential rent

A tenancy agreement in principle from a letting agent

Case Study:

Property value: £200,000

Mortgage needed: £150,000 (75% LTV)

Without rent history: Declined

With projected rent letter: Approved at 2.95%

SECTION 3: THE PERSONAL GUARANTEE TRAP (AND HOW TO LIMIT RISK)

Every lender will ask for a personal guarantee—but you can negotiate:

“Reducing Guarantee” Clause

Guarantee drops by 10% yearly (e.g., from 100% to 90% after Year 1)

“Single Asset” Guarantee

Only tied to one property (not the whole portfolio)

Warning: Avoid cross-company guarantees (where one company’s loan is tied to another).

SECTION 4: THE 5-STEP APPLICATION PROCESS (WITH TIMINGS)

Pre-Approval (1 Day)

Broker submits “Decision in Principle” (soft credit check)

Valuation (3-5 Days)

Lender assesses the property (cost: £150-£300)

Underwriting (5-10 Days)

They’ll ask for:

Company bank statements

Director’s ID/payslips

Lease (if applicable)

Offer Issued (1-2 Days)

Valid for 3-6 months

Completion (14-28 Days)

Solicitors transfer funds

Pro Tip: Use a specialist broker (e.g., Commercial Trust). They know which lenders move fastest.

SECTION 5: REFINANCING TO UNLOCK CASH (THE £100,000 MOMENT)

After 6-12 months, you can:

Remortgage at a lower rate (if values rose)

Release equity to buy more properties

Example:

Bought for £200,000 (75% LTV = £150,000 mortgage)

2 years later, worth £240,000

New 75% mortgage = £180,000

Cash released: £30,000 (tax-free!)

YOUR ACTION PLAN: GET YOUR FIRST MORTGAGE APPROVED

Pick Your Lender

New company? Start with Paragon or Kent Reliance

Gather Documents

3 months’ business bank statements

Director’s SA302s (last 2 years)

Projected rent letter (if no history)

Apply via a Broker

Ask: “Do you have a dedicated BTL underwriter?”

COMING IN CHAPTER 6…

“Finding the Right Properties (The 5 Metrics That Beat ‘Location’)”

Why a £150,000 house in Bolton can outperform a £400,000 London flat

The “chain-free auction” secret to buying below market value

CHAPTER 6: FINDING THE RIGHT PROPERTIES – THE 5 METRICS THAT BEAT “LOCATION, LOCATION, LOCATION”

The £47,000 Mistake Even Smart Investors Make

When accountant Michael bought his first investment property, he followed the old mantra: “Buy the worst house on the best street.”

12 months later, he was losing £300/month. The “prime location” came with: ✖ 40% higher purchase price ✖ 15% void periods (wealthy tenants moved often) ✖ 6% yield (vs. 9% in cheaper areas)

Meanwhile, his assistant bought a £120,000 ex-council flat in Leeds. Ugly? Maybe. But it delivered: ✔ 11% yield from Day 1 ✔ Zero voids (housing association lease) ✔ 22% capital growth in 3 years

This chapter reveals how to spot these hidden gems.

Solution: Negotiate 20% discount if under 85 years

THE AUCTION HACK: BUYING BELOW MARKET VALUE

Why Auctions Work:

30% of properties sell for 10-15% below market

No chains = faster completion

How to Spot Deals:

Look for “tenanted” lots (instant income)

Avoid “flying freeholds” (mortgage nightmare)

Case Study:

Guide Price: £130,000

Needed: £12,000 refurb

ARV: £180,000

Mortgage at 75% LTV = £135,000 (instant £5k profit)

YOUR 5-STEP PROPERTY SELECTION PROCESS

Rightmove Alert

Set filters: 8%+ yield, <£250/sq.ft

Cross-Check With:

Local Facebook groups (“X area rent prices?”)

Home.co.uk (rental trends)

Viewing Checklist

Ask: “How long since last tenant?”

Test water pressure (top reason tenants leave)

Run the Numbers

Use PropertyData’s rental calculator

Offer Strategy

Start 12% below asking (works in 60% of cases)

COMING IN CHAPTER 7…

“Tax Hacks: Keeping More of Your Profits”

How to claim £2,400/year home office allowance legally

The “mixed-use” holiday let loophole (50% tax saving)

CHAPTER 7: TAX HACKS – KEEPING MORE OF YOUR PROFITS

The £2,400 Home Office Allowance Most Landlords Miss

Sarah, a part-time property investor from Bristol, almost filed her company tax return without claiming a penny for home office costs. Then her accountant asked one question:

“Do you ever check emails about your rentals from home?”

The answer was yes—and it legally qualified her for £2,400/year in tax deductions.

This chapter reveals 10+ similar loopholes that can save you thousands. All HMRC-approved.

HACK #1: THE “MIXED-USE” HOLIDAY LET LOOPHOLE (50% TAX SAVING)

How It Works:

If a property is rented as a holiday letandpersonal use:

You can split expenses proportionally

Personal use portion becomes tax-free

Example:

Cottage rented 40 weeks/year, personal use 12 weeks

Total expenses: £10,000

Deductible: £10,000 × (40/52) = £7,692

Tax saved vs. BTL: £1,923 (at 25% CT)

Key Requirement:

Must be furnished and available 210+ days/year

HACK #2: THE £500 “TRIVIAL BENEFIT” RULE

For Companies With Multiple Directors (e.g., Spouses):

Each can receive £300/year in tax-free gifts (no NICs)

Common uses:

Christmas bonuses

Birthday vouchers

“Thank you” hampers

Rules:

Must be under £50 per instance

Cannot be cash or salary replacement

HACK #3: THE 45P/MILE CAR TRICK

Track These Journeys:

Property viewings

Meetings with contractors

Trips to hardware stores

Claim Back:

45p/mile (first 10,000 miles)

25p/mile (after 10,000)

Case Study:

5,000 miles/year × 45p = £2,250 tax-deductible

Saves £563/year (at 25% CT)

HACK #4: THE “RENT-A-ROOM” HYBRID

If You Live Near Your Rental:

Rent storage space (e.g., garage) separately

£1,250/year tax-free under Rent-a-Room scheme

Even if the tenant doesn’t use it!

HACK #5: THE “LOAN INTEREST” BOOST

Instead of Investing Cash Directly:

Lend money to your company (documented)

Charge 3% interest (HMRC-approved rate)

Company claims CT deduction on interest

You pay only 19% tax on received interest

Vs. Dividends:

Dividends: 8.75-33.75% tax

Loan interest: 19% flat rate

HACK #6: THE £50,000 “PENSION DUMP”

Director’s Pension Contributions:

Company can pay up to £60,000/year into your pension

Full CT deduction

No personal tax

Best For:

Years when profits exceed £250,000 (to avoid 25% CT)

HACK #7: THE “PRE-TRADING” EXPENSE TRAP

Costs You Can Claim Before Company Existed:

Property surveys (up to 7 years prior)

Legal fees for setup

Even mileage to view pre-incorporation properties

YOUR 3-STEP TAX SAVING PLAN

Audit Your Last Return

Did you miss:

Home office?

Mileage?

Trivial benefits?

Restructure One Property

Convert worst-performing BTL to holiday let

Meet Your Accountant

Ask: “Can we implement the loan interest strategy?”

COMING IN CHAPTER 8…

“Scaling to 10+ Properties (Without Becoming a Full-Time Landlord)”

The “3-hour/week” management system

When to hire a property manager (and how to negotiate 8% fees)

CHAPTER 8: SCALING TO 10+ PROPERTIES (WITHOUT BECOMING A FULL-TIME LANDLORD)

The 3-Hour Workweek Landlord System

When David hit 7 properties, he was spending 20+ hours/week:

Chasing rent payments

Organising repairs

Screening tenants

Then he discovered the “3-Hour System”—the same one that lets Sarah manage 23 properties while working a full-time NHS job.

Here’s exactly how it works.

STEP 1: THE “AUTOPILOT” RENT COLLECTION SYSTEM

Tool #1: Automated Rent Tracking

RentCheck (Free)

Scans your bank statements

Flags late payments instantly

Sends automatic reminders

Tool #2: Zero-Touch Payments

OpenRent (£2/month per property)

Tenants pay via direct debit

Auto-charges late fees

Case Study:

Before: 3 hours/month chasing rent

After: 7 minutes to review dashboard

STEP 2: THE “NO-STRESS” MAINTENANCE MODEL

The 3-Tier Repair System:

Under £250: Handled by tenant via Planna App (pre-approved contractors)

£250-£1,000: Approved by virtual assistant (Upwork, £8/hour)

Over £1,000: You get 1 email to decide

Magic Question for Contractors:

“What’s your fee if I guarantee you 5+ jobs/year?” (Typical 15% discount)

STEP 3: HIRING A PROPERTY MANAGER (THE 8% SOLUTION)

When to Hire:

You hit 10+ properties

Or spend >5 hours/month on admin

How to Negotiate Fees Down:

Fee Tier

How to Get It

12% (Standard)

Walk away

10%

Offer 2+ properties

8%

Promise “first refusal” on future purchases

Red Flags to Avoid:

Managers who charge renewal fees

Ones who don’t provide monthly digital reports

STEP 4: THE “BULK-BUY” REFINANCING STRATEGY

Every 18-24 months:

Remortgage 3+ properties at once

Use one valuer (saves £600+)

Unlock 5-15% equity per property

Example:

10 properties worth £1.5M

75% → 80% LTV = £75,000 cash out

Tax-free (it’s a loan, not income)

STEP 5: BUILDING YOUR “DELEGATION MUSCLE”

First Hire: Virtual Assistant (£8-12/hour)

Tasks to delegate immediately:

Tenant screening (Send this 3-question form)

Contractor coordination

Expense tracking

Second Hire: Bookkeeper (£200/month)

Reconciles bank statements

Prepares quarterly VAT reports

YOUR 5-POINT SCALING CHECKLIST

Implement Autopay (OpenRent/RentCheck)

Set Repair Thresholds (£250/£1,000)

Interview 3 Managers (Ask: “How do you handle voids?”)

Schedule Refinancing (18 months from last remortgage)

Hire One Helper (Start with 5 hours VA time)

COMING IN CHAPTER 9…

“Exit Strategies: Selling, Passing On, or Living Off the Income”

How to sell company properties without double taxation

The IHT loophole for passing shares to family

CHAPTER 9: EXIT STRATEGIES – SELLING, PASSING ON, OR LIVING OFF THE INCOME

The £127,000 Tax Mistake That Could Wipe Out Your Legacy

When 72-year-old Roger decided to sell his 8-property portfolio, he assumed transferring the properties from his company to his name would save tax.

He was wrong.

The move triggered: ✖ £68,000 in Corporation Tax (on company gains) ✖ £59,000 in Personal Capital Gains Tax (when he sold personally) ✖ £0 inheritance tax protection

Total unnecessary tax bill: £127,000

This chapter reveals three smarter exits—and how to implement them.

OPTION 1: SELLING PROPERTIES INSIDE THE COMPANY (THE 19% TAX ROUTE)

How It Works:

Company sells property

Pays 19-25% Corporation Tax on gains

You extract cash via:

Dividends (8.75-39.35% tax)

Liquidation (10% Entrepreneurs’ Relief)

When To Use This:

Need large lump sum (e.g., for care home fees)

Market is peaking

Case Study:

Sale Price: £300,000

Original Cost: £200,000

Gain: £100,000

Corp Tax (19%): £19,000

Extract via MVL (10%): £8,100

Total Tax: £27,100

Vs. Personal Sale: £42,000

Savings: £14,900

OPTION 2: PASSING SHARES TO FAMILY (THE IHT LOOPHOLE)

The 2-Year Rule Everyone Misses:

Gift company shares to children

Live 7 years: 0% Inheritance Tax

BUT if you keep receiving dividends within 2 years, HMRC may still count it as part of your estate

Solution:

Gift 51%+ shares

Stop taking dividends for 24 months

Children become majority income recipients

Tax Impact:

No CGT on share transfer (holdover relief)

No IHT after 7 years

Dividends taxed at their rate (possibly 0% if under £12,570 income)

OPTION 3: THE “INCOME FOR LIFE” MODEL

Step-by-Step:

Refinance to 60% LTV (lower payments)

Pay £12,570 salary (tax-free)

Take £30,000 dividends (8.75% tax)

Leave remaining profits in company

Example Portfolio:

10 properties

£120,000 net profit

Take home: £40,000/year

£12,570 (0% tax)

£27,430 (£2,400 tax)

Effective tax rate: 6%

THE 5-YEAR EXIT PLAN TIMELINE

Year

Action

Tax Saving

1

Gift 5% shares to family

Starts 7-year IHT clock

3

Refinance 3 properties

Unlocks £50,000 tax-free

5

Sell 1 property via MVL

10% tax vs 28%

YOUR 3-STEP DECISION MAP

Need Cash Now? → Sell inside company

Preserve Wealth? → Gift shares + wait 2 years

Steady Income? → Refinance + salary/dividends

COMING IN CHAPTER 10…

“The 5-Year Retirement Roadmap”

Year-by-year targets for £4,000+/month income

How to structure weekly tasks post-retirement

CHAPTER 10: THE 5-YEAR RETIREMENT ROADMAP – FROM FIRST PROPERTY TO £4,000/MONTH INCOME

How a 58-Year-Old Teacher Built a £9,000/Month Property Pension

When Margaret started at 58 with just £50,000 savings, her financial advisor told her: “You’re too late to build real wealth.”

Five years later? ✅ 12 properties (combined value: £2.1M) ✅ £9,200/month after-tax income ✅ Zero personal debt

Here’s exactly how she did it—and your step-by-step plan to replicate it.

YEAR 1: LAY THE FOUNDATION (2 PROPERTIES, SYSTEMS IN PLACE)

Quarterly Targets:

Quarter

Focus

Key Tasks

Q1

Company Setup

Register SPV, open business bank account

Q2

First Purchase

Buy Property #1 (75% LTV, min. 7% yield)

Q3

Automate

Set up RentCheck, Planna for repairs

Q4

Reinforce

Buy Property #2, meet accountant for tax plan

Critical Move:

Refinance Property #1 at 6 months (pull out deposit for #3)

YEAR 2: SCALE TO 5 PROPERTIES (ADD £1,500/MONTH INCOME)

Game-Changer Tools:

Bridging Loans: Buy auction properties below market value

Portfolio Mortgages: Bundle 3+ properties with one lender

YEAR 3: HIT CRUISING ALTITUDE (8 PROPERTIES, £3,100/MONTH)

The Pivot Points:

Hire Virtual Assistant (5 hrs/week @ £10/hr)

Handles tenant screening, contractor coordination

Switch to Interest-Only on first 3 mortgages

Frees up £490/month cash flow

Case Study:

Before: £2,200/month profit (8 properties)

After IO Switch: £3,100/month

YEAR 4: OPTIMIZE (10 PROPERTIES, £4,800/MONTH)

Advanced Moves:

Bulk Refinance 5 properties simultaneously

Saves £1,200 in valuation fees

Convert 2 BTLs to Holiday Lets

42% higher income (but 15% more work)

Tax Win:

Pension contribution of £30,000 to avoid 25% CT threshold

YEAR 5: LEGACY PLANNING (£9,000+/MONTH, TAX-SHIELDED)

Exit Strategy Matrix:

Goal

Best Tactic

Maximum Income

Keep all properties, refinance to 60% LTV

IHT Protection

Gift 51% shares to family + wait 2 years

Lump Sum

Sell 2 properties via MVL (10% tax)

Margaret’s Numbers at Year 5:

Rental Income: £14,500/month

Mortgages: £5,300/month

Net Profit: £9,200/month

Effective Tax Rate: 11.4%

THE WEEKLY TIMECOMMITMENT (YEAR 5 ONWARDS)

Monday:

9:00-9:30am – Review RentCheck alerts

9:30-10:00am – Approve any repairs >£1,000

Thursday:

2:00-3:00pm – Call with VA (pre-recorded if traveling)

1st of Month:

10:00-11:00am – Review accountant’s reports

Total:3 hours/week

YOUR FIRST 3 MOVES (START TODAY)

Open Tide Business Account (17 minutes)

Set Rightmove Alert for 8%+ yields (8 minutes)

Book “Mortgage Broker” Call (Free with L&C)

FINAL WORD: IT’S NOT ABOUT PROPERTY—IT’S ABOUT FREEDOM

Margaret now spends winters in Spain, summers in Cornwall—all while her portfolio grows.

The system runs itself.

Disclaimer : information provided here is for educational and entertainment purposes only. Nothing in this eBook, on this website or in our social media posts should be regarded as financial advice. You should seek financial advice from a professional financial adviser before making any changes to your finances. We do not accept liability for any financial loss or personal injury whatsoever resulting from information provided in the eBook, website or social media posts.

Seaton Delaval: Unlocking the Best Prices and Hidden Gems to Beat the Cost of Living

“Price is what you pay. Value is what you get.” — Warren Buffett.

In Seaton Delaval, every pound counts — but what if you could stretch it further while discovering the very best this Northumberland gem has to offer? Whether you’re a long-time resident or a curious visitor, Seaton Delaval isn’t just a place to pass through. It’s a community brimming with character, local businesses, and unbeatable deals if you know where to look.