Discover how strategic downsizing in the UK can unlock significant tax-free capital, reduce monthly utility overheads, and improve your mental well-being for a wealthier, healthier retirement after 55.

Downsizing your UK home in 2026 can create a happier retirement by liberating “trapped” equity that can be reinvested into experiences and health-focused lifestyle changes. At CheeringUp.info, we believe that your home should serve your current needs rather than your past memories. By moving to a smaller, more energy-efficient property, you eliminate the physical and financial “maintenance drag” that often peaks in your late 50s.

Average Capital Release: Research suggests that UK homeowners over 55 can release an average of £127,414 by moving from a detached family home to a semi-detached or bungalow.

Utility Savings: Modern smaller homes can reduce annual energy bills by up to 35%, a crucial factor as UK energy price caps remain volatile in 2026.

The “Happiness Dividend”: According to recent surveys, 43% of UK downsizers reported that the move directly funded a more active social life and improved their mental well-being.

“In 2026, the ‘right-sizing’ trend is no longer just about saving money; it’s about reclaiming time. For the over 55s, moving to a home that fits your future—not your past—is the fastest way to boost both your bank balance and your daily joy.” — Retirement Trends Report 2026

Is a Smaller Property the Key to a Healthier Lifestyle Over 55?

A smaller property is the key to a healthier lifestyle over 55 because it significantly reduces the physical strain of home maintenance and encourages more “out-of-home” social interaction. CheeringUp.info champions the transition to manageable living spaces that allow more time for low-impact exercise and community engagement.

Reduced Injury Risk: Smaller, single-level homes (bungalows) reduce the risk of fall-related injuries, which account for a significant portion of NHS admissions for the over-65s.

Community Proximity: Strategic downsizing often moves retirees closer to high-street amenities, increasing daily step counts by an average of 2,000 steps.

Mental Clarity: Decluttering a lifetime of possessions during a move has been clinically linked to reduced cortisol levels and improved cognitive focus in older adults.

Why is Strategic Tax Planning Essential for UK Retirees This Year?

Strategic tax planning is essential for UK retirees this year because frozen income tax thresholds and the 2026 State Pension increase to £241.30 per week mean more retirees risk falling into higher tax brackets.CheeringUp.info helps you navigate these shifts by highlighting how to protect your hard-earned wealth.

ISA Maximisation: You can still shield up to £20,000 per year from the taxman, ensuring your investment growth remains entirely tax-free.

The 25% Rule: Utilising your 25% tax-free pension lump sum (capped at £268,275) strategically can fund a downsized move without touching your taxable income.

Gifting Allowances: You can gift up to £3,000 annually (the annual exempt amount) to family members, reducing potential Inheritance Tax (IHT) liabilities while seeing your loved ones benefit now.

Ready for more than just a quiet life after work? Discover practical ideas to create true freedom in your UK retirement. This guide from CheeringUp.info Retirement Club shows you how to explore, connect, and build a purposeful, vibrant next chapter. Your adventure starts here.

Creating Ideas For Freedom in Your UK Retirement: Your Launchpad to an Extraordinary Next Chapter

Retirement in the UK isn’t about fading away—it’s about powering up. This is your moment to trade routines for adventures and obligations for passions. The CheeringUp.info Retirement Club is your movement for people who refuse to let life shrink after 55. We’re here to help you fuel your ambition, upgrade your lifestyle, and turn your later years into your most vibrant yet. Let’s design a retirement defined not by age, but by freedom.

What Does “Freedom in Retirement” Really Mean?

Freedom in retirement is more than financial independence; it’s the liberty to design your days around what makes you feel truly alive. It’s about:

Exploration: Discovering new places, hobbies, and parts of yourself you never had time for.

Connection: Building new social networks and forging friendships with like-minded people.

Growth: Learning new skills, starting a small business, or finally ticking off those lifelong ambitions.

Purpose: Finding meaningful ways to contribute, share your experience, and feel valued.

A 2022 study from University College London found that adults over 60 who regularly engage in playful, purposeful activities report 37% lower stress levels and a 23% reduced risk of cognitive decline. Your retirement freedom is your ultimate tool for health and happiness.

Practical Ideas to Engineer Your Retirement Freedom

You don’t need a luxury budget to live large—you just need a plan and the willingness to start. Here are actionable ideas to build a play-filled, purposeful retirement.

Become a Local Explorer: There’s a whole world less than an hour from your front door. Grab an OS map and rediscover forgotten footpaths, hidden woodlands, and historical gems in your area.

Turn Passion into Project: Have a skill in arts, crafts, or baking? Turn it into a small business. Love animals? Become a dog walker or pet sitter. This isn’t about pressure; it’s about monetising your joy.

Build New Social Networks: Combat loneliness by joining a local choir, historical re-enactment group, or a dance class like salsa or ballet. Active social connections are a powerful antidote to isolation.

Learn and Lead: Always wanted to play an instrument, speak Italian, or upcycle furniture? Now is your time to practice till you’re perfect. Consider volunteering as a tour guide for the National Trust to share your enthusiasm with others.

Join Your Tribe: The CheeringUp.info Retirement Club

Finding your people is key to a joyful retirement. The CheeringUp.info Retirement Club is a thriving UK community for over-55s who are done with clichés and ready for connection.

State Pension Age 73 UK: Disappointing Pension Forecast & Cost of Living Crisis Subcribe CheeringUpInfo

As a member, you’ll gain access to:

A Vibrant Community: Connect with like-minded individuals online and at real-life activities, day trips, and meetups locally, nationally, and even overseas.

Exclusive Ideas and Deals: Tune into member-only online events with lifestyle experts and access special offers to make your retirement income go further.

Your Playful Rebellion: This is your chance to rewrite the rules. Share your ideas, discover new experiences, and build the retirement lifestyle you truly deserve.

Your Freedom Awaits – Take the First Step Today

The clock is ticking, but not in the way you think. Every day is a new chance to play harder, connect deeper, and live louder. Your retirement freedom isn’t a dream—it’s a decision.

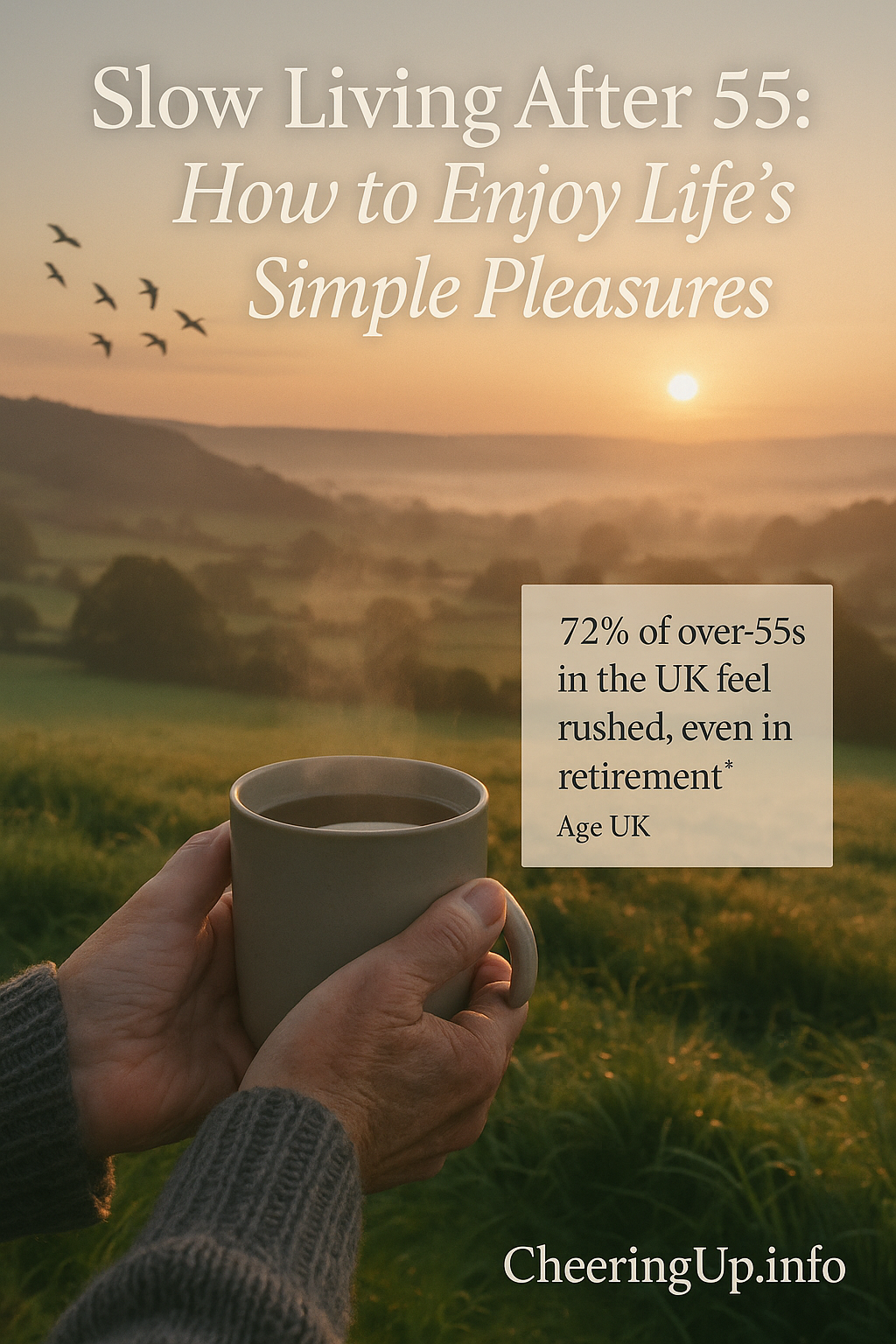

The Life-Changing Power of Slow Living for the Over-55s in the UK: A Complete Guide

Why Slow Living Could Be Your Missing Key to Happiness

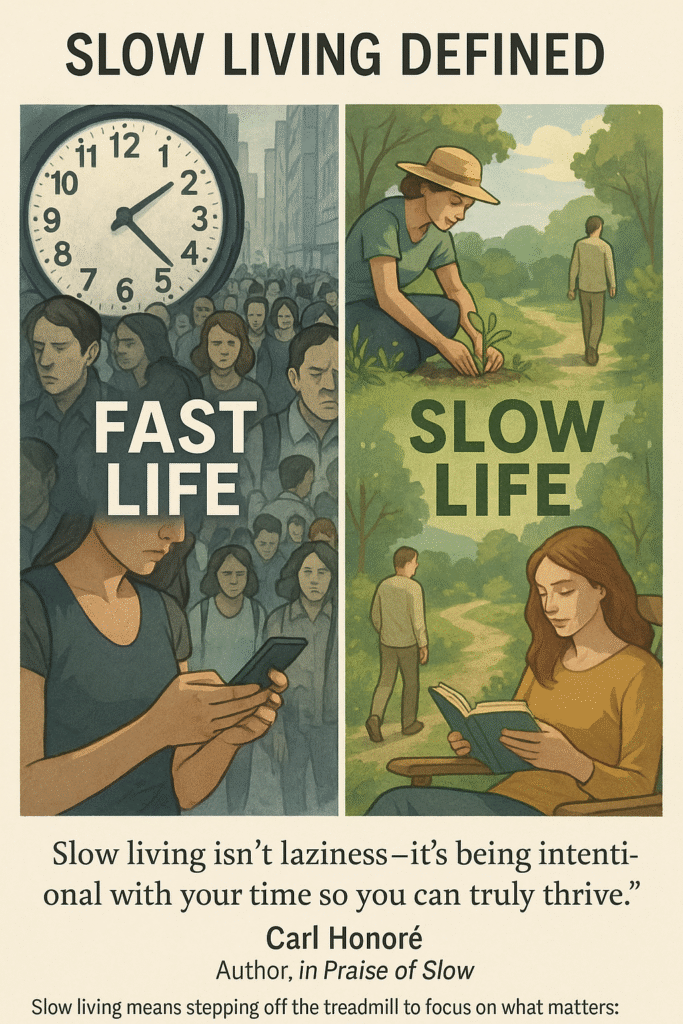

In our hyper-connected, fast-paced world, a quiet revolution is taking place among the UK’s over-55 population. Increasing numbers are discovering that the secret to a fulfilling later life isn’t more – more activities, more possessions, more commitments – but less, done better and with greater presence.

“We’re witnessing a fundamental shift in how people approach their later years,” observes Dr. Sarah Brewer, longevity expert and author of Live Longer, Live Better. “The over-55s are rejecting society’s obsession with speed and productivity in favour of what I call ‘conscious ageing’ – living with intention, attention and appreciation.”

This comprehensive guide goes beyond superficial tips to explore how embracing slow living can transform your health, relationships, finances and overall wellbeing. Packed with:

Groundbreaking scientific research on ageing and wellbeing

Real-life case studies from UK slow living practitioners

Expert insights from gerontologists, financial planners and lifestyle coaches

Practical challenges and action plans you can implement immediately

Whether you’re approaching retirement, recently retired or well into your later years, this guide will show you how to craft a life of greater meaning, connection and joy by embracing the power of slow.

The Science and Philosophy of Slow Living

Understanding the Slow Living Movement

Slow living isn’t about doing everything at a snail’s pace – it’s about doing the right things at the right pace. Emerging from Italy’s Slow Food Movement in the 1980s as a protest against fast food culture, the philosophy has since expanded into a comprehensive approach to modern living.

“Slow living is essentially about reclaiming your attention and aligning your daily life with your deepest values,” explains Carl Honoré, author of the international bestseller In Praise of Slow. “For the over-55s, it offers particularly powerful benefits because it helps counteract many of the psychological and physiological challenges of ageing.”

Why Slow Living Resonates with the Over-55s

A 2023 study by Age UK revealed startling statistics:

72% of over-55s reported feeling “constantly rushed” despite being retired

65% said they experienced more stress post-retirement than anticipated

82% wished they had more “quality time” with loved ones

Dr. Rebecca Harris, gerontologist at the University of Bristol, explains: “As we age, our relationship with time fundamentally changes. The over-55s often experience what we call ‘time compression’ – the sensation that time is accelerating. Slow living practices help expand our perception of time by bringing us into the present moment.”

The Neuroscience of Slowing Down

Groundbreaking research in neuroplasticity shows that our brains remain adaptable throughout life. A 2022 Cambridge University study found that mindfulness practices common in slow living:

Increase grey matter density in memory-related brain regions

Strengthen the prefrontal cortex, improving decision-making

“What’s remarkable,” notes Dr. Harris, “is that these changes were particularly pronounced in participants over 60, suggesting older brains may be especially responsive to slow living practices.”

The Transformative Health Benefits of Slow Living

1. Mental Wellbeing: From Stress to Serenity

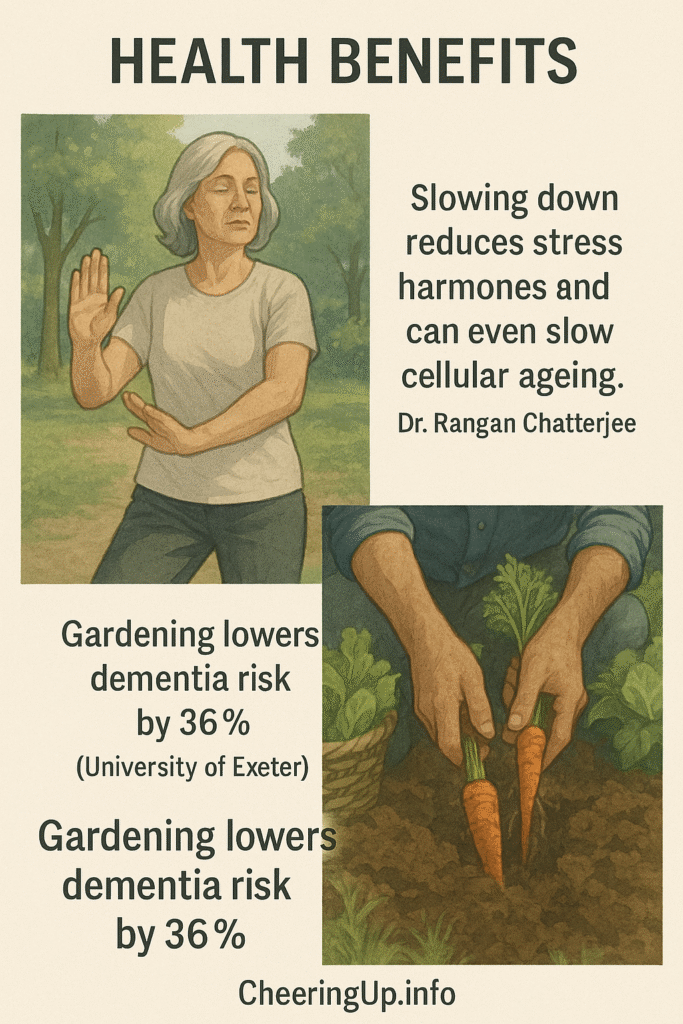

Dr. Rangan Chatterjee, BBC presenter and author of The Stress Solution, explains: “Chronic stress accelerates cellular ageing through telomere shortening. Slow living practices like mindfulness and nature immersion activate the parasympathetic nervous system, which acts as an anti-ageing mechanism.”

Case Study: Margaret’s Transformation Margaret, 67, a retired teacher from Brighton, struggled with:

Chronic insomnia

Retirement-related anxiety

Feeling “useless” without work structure

Her slow living prescription:

Digital sunset (no screens after 7pm)

Morning pages journaling (3 handwritten pages each morning)

Daily “forest bathing” in Stanmer Park

“Within three months, my sleep improved dramatically,” Margaret reports. “I’ve rediscovered my love for watercolours and actually enjoy my own company now.”

2. Physical Health: Movement That Matters

Unlike punishing exercise regimens, slow living promotes sustainable movement:

Activity

Proven Benefits

Ideal For

Tai Chi

Improves balance (reducing fall risk by 43%)

Arthritis sufferers

Gardening

Lowers dementia risk by 36% (Exeter University)

Those with limited mobility

Nordic Walking

40% more calorie burn than regular walking

Cardiovascular health

“The key is consistency over intensity,” emphasises Dr. Muir Gray, NHS adviser on healthy ageing. “Ten minutes of daily gentle movement beats one hour of weekly intense exercise for longevity benefits.”

3. Cognitive Benefits: Keeping the Mind Agile

Dr. Angela Clow’s research at Westminster University demonstrates how slow hobbies create cognitive reserve:

Learning a language: Increases grey matter density

Playing chess: Enhances strategic thinking

Playing musical instruments: Improves neural connectivity

“The brain needs novelty, but without time pressure,” Dr. Clow explains. “This combination is perfect for maintaining cognitive function as we age.”

Slow Travel – The Art of Journeying Mindfully

Why Slow Travel Transforms Later-Life Adventures

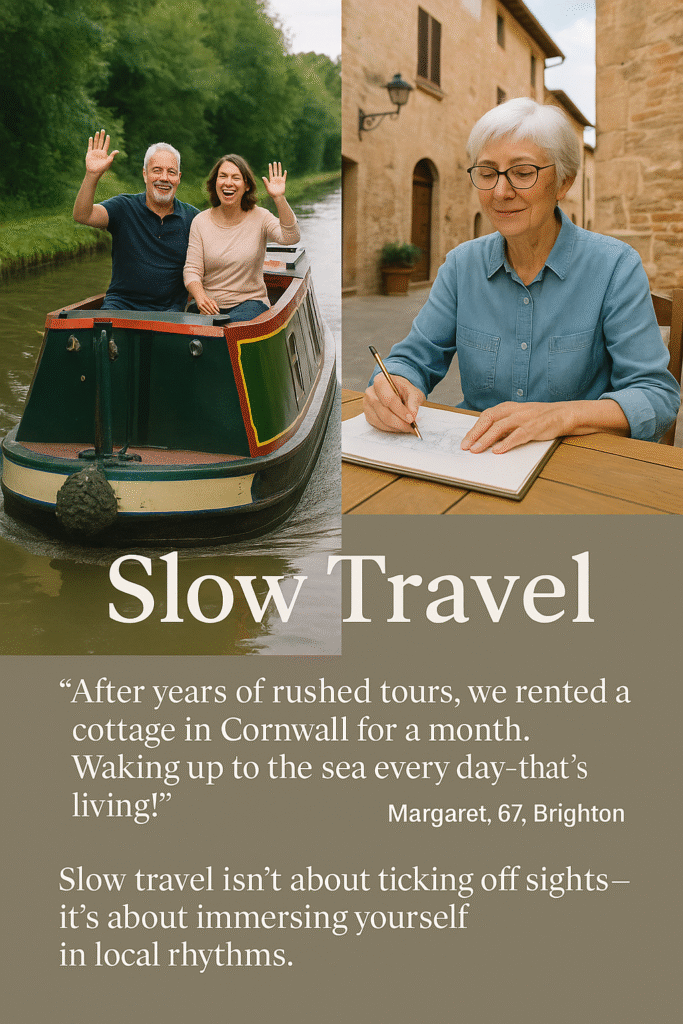

Pauline Kenny, founder of Slow Europe, observes: “Traditional tourism often leaves older travellers exhausted. Slow travel aligns perfectly with the needs of over-55s by prioritising depth over distance, experience over checklist tourism.”

The Slow Travel Advantage:

Traditional Travel

Slow Travel

Packed itineraries

Spontaneous exploration

Tourist hotspots

Local hidden gems

Jet lag

Natural rhythms

Surface experiences

Meaningful connections

Inspiring Slow Travel Ideas for Over-55s

UK Canal Boating Holidays

Route suggestion: The Llangollen Canal (7 days)

Highlights:

Walking pace travel (max 4mph)

Quaint waterside pubs

Operating locks (gentle physical activity)

Cost: From £1,200/week (shared between 4)

“It’s the perfect blend of gentle adventure and relaxation,” says Derek, 71, who holidays annually with his canal boat group.

European House Sitting

How it works: Care for homes/pets in exchange for free accommodation

Best platforms: TrustedHousesitters, MindMyHouse

Ideal locations: Rural France, Italian countryside

Case Study: Susan’s Year of Slow Travel Susan, 68, spent 2023 house sitting in:

A Provençal vineyard

A Tuscan farmhouse

A Portuguese coastal village “I’ve lived like a local across Europe for a fraction of hotel costs,” she says.

Pilgrimage Walking (The Slowest Travel)

Camino de Santiago: The Portuguese route (gentler terrain)

UK alternatives:

St Cuthbert’s Way (Scotland/England border)

Pilgrims’ Way to Canterbury

Slow Home Living – Creating Your Personal Sanctuary

The Psychology of Slow Spaces

Julia Atkinson-Dunn, slow living advocate and author, explains: “Our homes should be our sanctuaries, especially as we age. A slow home isn’t about aesthetic perfection – it’s about creating spaces that support how you truly want to live.”

The 5 Pillars of Slow Home Living:

Intentional Spaces

Designate areas for specific activities (reading nook, craft corner)

Remove multi-purpose clutter

Natural Elements

Maximise natural light

Incorporate wood, stone and plants

Tech Boundaries

Create screen-free zones

Implement “digital sunsets”

Sensory Comfort

Soft textiles

Soothing colour palettes

Ambient lighting

Ease of Movement

Age-friendly design

Clear pathways

Comfortable seating

Case Study: John & Linda’s Downsizing Journey This York couple transformed their living space by:

Implementing the “one in, one out” rule

Creating a dedicated slow living room (no TV, just books and music)

Designing a low-maintenance garden with raised beds

“Our home now feels like a daily retreat rather than a maintenance burden,” Linda shares.

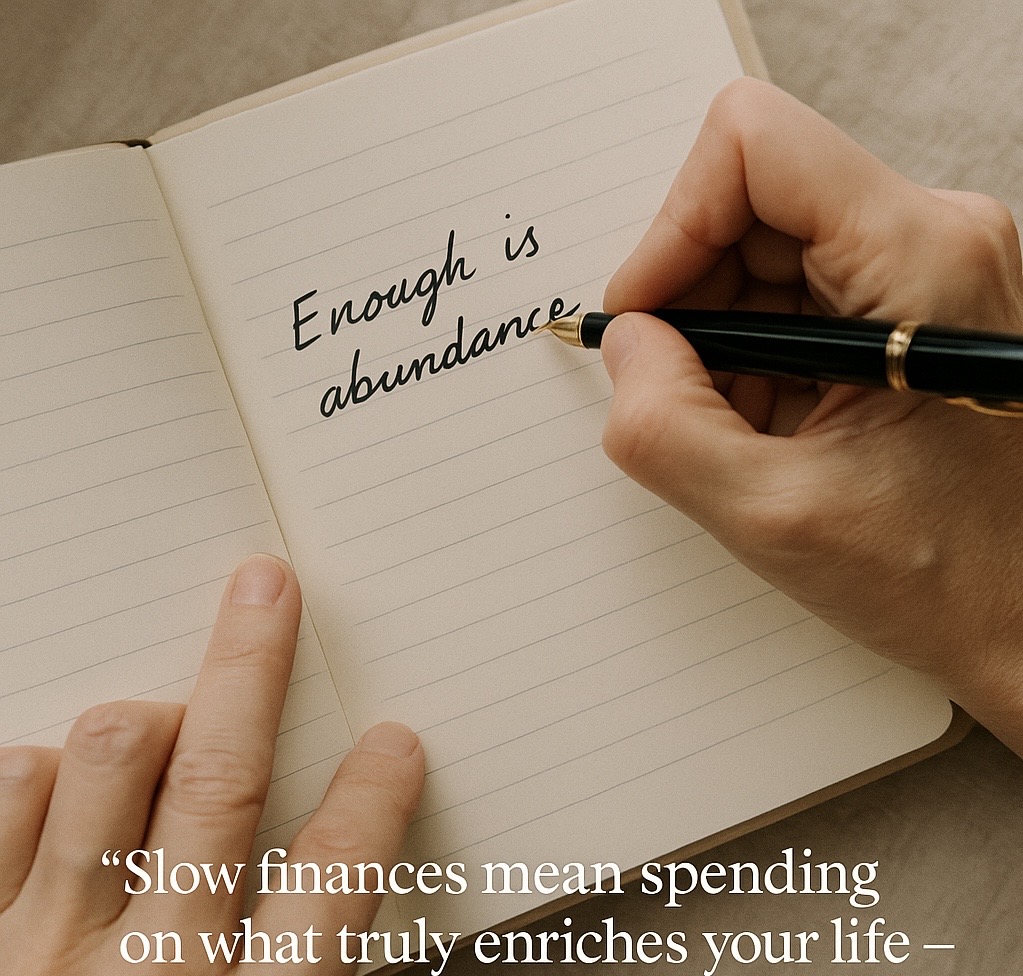

Slow Finances – Redefining Wealth in Later Life

The New Retirement Economics

Sarah Coles, personal finance analyst at Hargreaves Lansdown, notes: “The traditional retirement model is broken. People are living longer but often worrying more about money. Slow finances offer a sustainable alternative.”

Principles of Slow Finance:

‘Enough Mindset’

Distinguish between needs and wants

Practice conscious consumption

Sustainable Withdrawal Strategies

The 3.5% rule (safer than traditional 4%)

Bucket strategy for market downturns

Experimental Spending

Prioritise meaningful experiences

The “20-year test” (“Will this matter in 20 years?”)

Case Study: Geoff’s Investment Transformation Geoff, 68, shifted from active trading to slow investing:

Moved to dividend-paying stocks

Implemented a three-bucket system:

Immediate cash needs

3-5 year bonds

Long-term growth funds “I sleep better and my portfolio grows steadily,” he reports.

Your 7-Day Slow Living Challenge

Day 1: Digital Detox

No screens before breakfast/after dinner

Try analog alternatives (physical books, handwritten letters)

Day 2: Mindful Eating

Prepare one meal from scratch

Eat without distractions

Day 3: Nature Immersion

30+ minutes outdoors

Practice “forest bathing”

Day 4: Financial Review

Cancel one unused subscription

Set up a “slow spending” tracker

Day 5: Social Slowdown

One quality conversation (no multitasking)

Write a heartfelt letter

Day 6: Home Sanctuary

Declutter one space

Create a slow living corner

Day 7: Reflection

Journal about your experience

Plan ongoing slow living practices

Conclusion: Your Slow Living Blueprint

The Slower You Go The More You’ll Notice!

Slow living isn’t about withdrawing from life – it’s about engaging with it more deeply. As Dr. Brewer concludes: “The slower you go, the more you’ll discover that true richness comes not from accumulation, but from appreciation.”

Your Next Steps:

Start small – Pick one element from this guide to implement

Build gradually – Add new practices as habits form

Share the journey – Inspire others in your community

Remember, as Carl Honoré reminds us: “Slowing down isn’t about giving up – it’s about gearing up for what truly matters.” Your most fulfilling years may well be ahead of you, waiting to be discovered at the perfect pace – yours.

Riding Out the Storm: A Gen X Guide to Thriving in Retirement

April 2025. Halifax, England. The headlines scream of economic turmoil. Inflation, a beast many thought tamed, is stirring again. Wars rage in distant lands, disrupting supply chains and fueling uncertainty. Tariffs, those blunt instruments of trade, threaten to choke off growth. Here in the UK, the legacy of COVID-era money printing by central banks is colliding head-on with these global shocks, creating a perfect storm.

Consider this: A recent survey reveals that 75% of UK adults over 55 are now “very concerned” about the impact of the current economic climate on their retirement savings. That’s a chilling statistic, isn’t it? For Generation X, those born between the mid-1960s and early 1980s, many of whom are now in their late 40s and 50s, this unfolding crisis presents a unique challenge. The comfortable retirement they envisioned, built on decades of hard work and careful saving, suddenly feels precarious.

Why is the UK economy facing such headwinds, and why does it disproportionately hurt the over-55s and those already in retirement? Let’s break it down.

The UK’s Economic Tightrope Walk

Several interconnected factors are contributing to the current economic struggles in the United Kingdom:

The Lingering Shadow of COVID-19: The pandemic triggered unprecedented levels of government spending and quantitative easing (printing money) to support businesses and individuals. While necessary at the time the amount printed was excessive and prolonged, this has contributed to inflationary pressures as the economy reopened and demand surged. All that extra money sloshing around? It devalued your existing retirement savings.

Global Geopolitical Instability: The ongoing conflicts and rising international tensions are disrupting energy markets, increasing commodity prices, and creating uncertainty for businesses. Think about the price of petrol at the pump or the rising cost of your energy bills – these are direct consequences of global instability.

Supply Chain Disruptions: The pandemic exposed vulnerabilities in global supply chains. Now, geopolitical issues and trade barriers are exacerbating these problems, leading to shortages of goods and higher prices for consumers. Remember when you couldn’t find certain items on supermarket shelves? That’s a supply chain issue biting.

Inflationary Pressures: A confluence of factors – the money supply increase, rising energy costs, and supply chain bottlenecks – has driven inflation to levels not seen in decades. This erodes the purchasing power of savings and makes everyday living more expensive. Your pension income simply doesn’t stretch as far.

Stagnant Wage Growth: While inflation has soared, wage growth for many has not kept pace, meaning real incomes are falling. This is particularly tough for those on fixed incomes, like many retirees. Imagine trying to pay for groceries when your pension has stayed the same but the prices have jumped!

The Impact of Tariffs and Trade Barriers: Evolving global trade relationships have introduced new complexities and costs for businesses, potentially impacting economic growth and contributing to higher prices. Businesses facing higher import costs often pass those costs onto consumers.

A Perfect Storm for the Over-55s and Retirees

This economic maelstrom is particularly damaging for those over 55 and already in retirement for several crucial reasons:

Erosion of Savings: Inflation directly diminishes the real value of their accumulated savings and pensions. A fixed pension income buys less and less each month.

Reduced Investment Returns: Economic uncertainty often leads to lower returns on investments, making it harder for pension pots to grow or even maintain their value. The stock market can be a bumpy ride during turbulent times.

Increased Cost of Living: Rising energy bills, food prices, and care costs disproportionately affect those on fixed incomes. These are essential expenses that can’t easily be cut back.

Longer Life Expectancy: People are living longer, meaning their retirement savings need to last for a more extended period. Economic downturns that deplete savings early in retirement can have devastating long-term consequences.

Limited Earning Potential: For those approaching or in retirement, the ability to significantly increase their income through employment is often limited. Finding a new job in your late 50s or 60s isn’t always straightforward.

Psychological Impact: The anxiety and stress of seeing their hard-earned savings dwindle can take a significant toll on the mental well-being of this age group. The fear of running out of money in retirement is a heavy burden.

But hold on! Before you throw your hands up in despair, remember this: Generation X is nothing if not resilient! We’ve navigated economic ups and downs before. We’ve adapted to technological shifts and cultural changes. And we can ride out this storm too. It requires a proactive and strategic approach.

Here are nine powerful ways that the over-55s in the UK can protect themselves from current and medium-term economic problems and ensure their retirement finances can still deliver the lifestyle they desire:

1. Take a Hard Look at Your Budget and Cut Unnecessary Spending

This might seem obvious, but it’s the bedrock of financial resilience. Now is the time for a forensic examination of your outgoings.

Track Your Spending: Use budgeting apps, spreadsheets, or even a notebook to meticulously record where your money is going for at least a month. You might be surprised by those small, regular expenses that add up. That daily takeaway coffee? Those impulse online purchases? They can take a significant bite out of your finances.

Categorise Expenses: Divide your spending into essential (housing, food, utilities, healthcare) and non-essential (entertainment, dining out, subscriptions).

Identify Areas for Reduction: Be honest with yourself. Which non-essential expenses can you reduce or eliminate? Could you downsize your TV package? Bring lunch from home more often? Review those multiple streaming subscriptions – do you really need them all?

Negotiate Bills: Don’t be afraid to haggle with your utility providers, internet company, and insurance providers. You might be able to secure a better deal just by asking! Comparison websites are your friend here. For example, you could call your broadband provider and say you’ve seen a cheaper deal elsewhere – they might just match it.

Consider Energy Efficiency: Invest in energy-saving measures for your home, such as switching to energy-efficient light bulbs, improving insulation, or getting a smart thermostat. While there’s an initial cost, the long-term savings on your energy bills can be substantial. Think about draught-proofing windows and doors – it’s a relatively cheap way to save energy.

2. Re-evaluate Your Investment Portfolio with a Focus on Risk and Income

If you have investments, particularly within your pension, now is the time to review your asset allocation with a qualified financial adviser.

Assess Your Risk Tolerance: As you approach and enter retirement, your ability to withstand significant investment losses typically decreases. Your portfolio might need to become more conservative. This doesn’t mean abandoning growth altogether, but it might involve shifting a larger portion of your assets into lower-risk investments like bonds or diversified funds with a track record of stability.

Consider Income-Generating Assets: Explore investments that provide a regular income stream, such as dividend-paying stocks or high-quality bonds. These can help supplement your pension income and reduce the need to draw down heavily on your capital. Remember, dividends aren’t guaranteed and can fluctuate.

Diversification is Key: Don’t put all your eggs in one basket! Ensure your portfolio is well-diversified across different asset classes, sectors, and geographies to mitigate risk. If one sector underperforms, others might hold steady.

Long-Term Perspective: Try to avoid making rash decisions based on short-term market fluctuations. Remember that investing is a long-term game. Panic selling during a downturn can lock in losses.

Seek Professional Advice: A qualified financial adviser can help you assess your individual circumstances, understand your risk tolerance, and develop a suitable investment strategy for the current economic climate. They can also help you navigate the complexities of pension drawdown.

3. Delay Retirement (If Feasible) and Consider Part-Time Work

For those approaching retirement, even a short delay can significantly boost your financial security.

Continue Building Your Pension Pot: Working for an extra few years means more contributions to your pension, allowing it more time to grow and benefit from potential market recovery.

Reduce Drawdown Pressure: Delaying retirement means you won’t need to start drawing on your pension savings as soon, giving them more time to accumulate.

Maintain Income and Benefits: Continuing to work provides a regular income stream and access to potential employment benefits like health insurance.

Explore Flexible Work Options: If full-time work isn’t appealing, consider part-time employment, consultancy roles, or freelance work. This can provide a valuable income supplement and keep you mentally and socially engaged. Think about your skills and how they could be applied in a flexible way. For example, a retired teacher could offer tutoring services.

Release Equity: Selling a larger property and buying a smaller one can free up a substantial lump sum that can be used to boost your retirement savings or provide additional income. Imagine the financial freedom of having a significant cash injection!

Reduce Maintenance and Running Costs: Smaller homes typically have lower utility bills, council tax, and maintenance costs. This can free up a significant portion of your monthly budget. Think about less gardening, less cleaning, and lower energy bills.

Consider Location: Downsizing might allow you to move to a more convenient location, closer to family, friends, or amenities, potentially reducing transportation costs.

Explore Retirement Communities: These communities often offer age-appropriate housing, social activities, and sometimes even care services, providing a supportive environment for later life. However, be sure to carefully consider the costs and fees involved.

Weigh the Emotional Aspects: Downsizing can be emotionally challenging, especially if you’ve lived in your home for many years. Carefully consider the emotional impact and discuss it with your family.

5. Strategize Your Pension Drawdown Carefully

If you’re already in retirement and drawing from your pension, it’s crucial to have a sustainable drawdown strategy.

Sustainable Withdrawal Rates: Avoid withdrawing too much too quickly. Aim for a sustainable withdrawal rate (typically around 3-4% per year) to ensure your pension pot lasts throughout your retirement. Withdrawing too much early on can significantly deplete your funds, especially during a downturn.

Phased Retirement: If you’re transitioning into retirement, consider a phased approach where you gradually reduce your working hours while drawing a smaller amount from your pension.

Regular Reviews: Review your drawdown strategy regularly with a financial adviser, especially in light of changing economic conditions and your personal circumstances.

Consider Annuities (with Caution): Annuities can provide a guaranteed income stream for life, offering security against longevity risk. However, consider the current interest rate environment and potential loss of flexibility before committing a significant portion of your pension to an annuity. Shop around for the best rates and understand the different types of annuities available.

Tax-Efficient Withdrawals: Work with a financial adviser to understand the most tax-efficient way to draw down your pension savings.

6. Explore Opportunities for Generating Additional Income in Retirement

Retirement doesn’t necessarily mean a complete cessation of income-generating activities.

Part-Time Work or Consulting: Utilise your skills and experience for part-time work or consulting in your field. This can provide a valuable income supplement and keep you mentally active.

Consider Rental Income: If you have a spare room, consider taking in a lodger (if your health and circumstances allow).

Explore Online Opportunities: The internet offers various ways to earn income, from online tutoring to freelance writing to selling crafts on platforms like Etsy.

Be Aware of Benefit Implications: If you are receiving state benefits, be sure to understand how additional income might affect your eligibility.

7. Understand and Claim Available Government Benefits

Make sure you are receiving all the state benefits you are entitled to.

Pension Credit: This provides extra money to help with living costs if you’re over State Pension age and on a low income. Many eligible people don’t claim it!

Attendance Allowance: If you have a disability and need help with personal care, you may be eligible for this non-means-tested benefit.

Winter Fuel Payment and Cold Weather Payment: These provide financial assistance with heating costs during the winter months.

Council Tax Reduction: You may be eligible for a reduction in your council tax bill depending on your circumstances.

Check the GOV.UK website and consult with organisations like Age UK or Citizens Advice to ensure you are claiming everything you are entitled to. They can provide invaluable assistance in navigating the benefits system.

8. Build and Maintain an Emergency Fund

An emergency fund can provide a crucial safety net to cover unexpected expenses without derailing your retirement finances.

Aim for 3-6 Months of Essential Living Expenses: This will help you weather unexpected costs like home repairs, medical bills, or a temporary loss of income.

Keep it Easily Accessible: Store your emergency fund in a readily accessible savings account, not tied up in long-term investments.

Top it Up Regularly: Make it a habit to contribute to your emergency fund whenever possible. Even small amounts can add up over time.

9. Stay Informed and Seek Professional Advice

The economic landscape is constantly evolving. Staying informed and seeking professional guidance is crucial.

Don’t Be Afraid to Ask for Help: Consult with qualified financial advisers, pension specialists, and benefits advisers. They can provide personalised guidance based on your specific situation. Remember, seeking advice is a sign of strength, not weakness.

Generation X: Forging a Resilient Retirement

The current economic climate presents significant challenges, but it doesn’t have to derail your retirement dreams. By taking proactive steps, carefully managing your finances, and seeking professional guidance, Generation X in the UK can build a resilient retirement that allows them to live the life they want. It requires vigilance, adaptability, and a willingness to make informed decisions. But remember, you’ve navigated challenges before, and with the right strategies, you can ride out this storm too and enjoy the retirement you’ve worked so hard for!